(a)

The profit or loss earned by a representative firm when

(a)

Explanation of Solution

Given information:

The price is $25, the quantity produced is 600, and the

The total revenue can be calculated using Equation (1) as follows:

Substitute the respective values in Equation (1) to calculate the total revenue.

The total revenue is $15,000.

The total cost can be calculated using Equation (2) as follows:

Substitute the respective values in Equation (2) to calculate the total cost.

The total cost is $9,000.

The profit or loss earned by a firm is the difference between the total revenue and total cost. The profit or loss of a firm can be calculated using Equation (3) as follows:

Substitute the respective values in Equation (3) to calculate the profit.

The profit of the firm is $6,000.

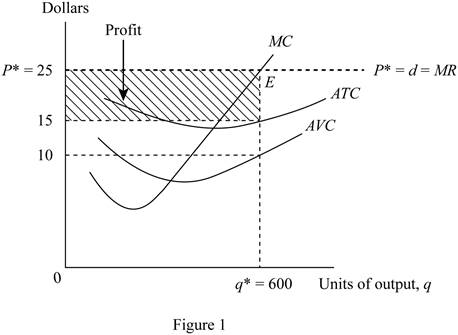

Figure 1 shows the profit earned by the representative firm.

The horizontal axis of Figure 1 measures the quantity of output, and the vertical axis measures the price. The average variable cost curve, average total cost curve, and the marginal cost curve are plotted using the given information. The marginal revenue curve is the same as the demand curve, and the price line as the firm is perfectly competitive. The profit maximizing output is produced at the point E, where the marginal revenue and marginal cost curves intersect. The shaded region in the graph represents the profit earned by the firm. The profit can also be calculated as the area of the shaded rectangular region.

Figure 1 reveals that the equilibrium price per unit is $25, equilibrium quantity is 600 units, and the cost per unit is $15. Thus, profit can be calculated as follows:

Thus, the profit of the firm is $6,000.

Total cost: Total cost is defined as the sum of fixed cost and variable cost.

Total revenue: Total revenue is defined as the total income earned from the sale of output produced.

Profit: Profit is defined as the excess revenue earned over the total cost of production.

(b)

The profit or loss earned by a representative firm when demand is D2.

(b)

Explanation of Solution

Given information:

The price is $15, the quantity produced is 400, and the average total cost is $18.

Substitute the respective values in Equation (1) to calculate the total revenue.

The total revenue is $6,000.

Substitute the respective values in Equation (2) to calculate the total cost.

The total cost is $7,200.

Substitute the respective values in Equation (3) to calculate the profit.

The loss of the firm is $1,200.

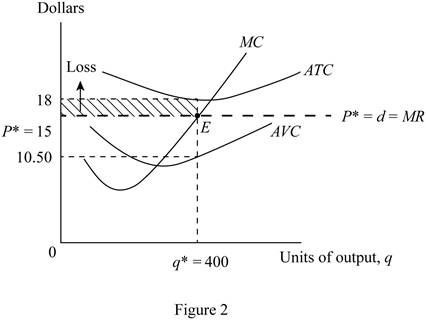

Figure 2 shows the loss incurred by the representative firm.

The horizontal axis of Figure 2 measures the quantity of output, and the vertical axis measures the price. The

Figure 2 reveals that the

Thus, the loss incurred is $1,200.

Total cost: Total cost is defined as the sum of fixed cost and variable cost.

Total revenue: Total revenue is defined as the total income earned from the sale of output produced.

Loss: Loss is defined as the excess cost incurred over the total revenue earned.

(c)

The profit or loss earned by a representative firm when demand is D3.

(c)

Explanation of Solution

Given information:

The price is $10, the quantity produced is 300, the average total cost is $21, and the average variable cost is $11..

Substitute the respective values in Equation (1) to calculate the total revenue.

The total revenue is $3,000.

Substitute the respective values in Equation (2) to calculate the total cost.

The total cost is $6,300.

Since the price is less than the average variable cost, the firm would better shutdown.

The loss of the firm is the total fixed cost of the firm. The total fixed cost can be calculated as follows:

The total fixed cost or the loss of the firm is $3,000.

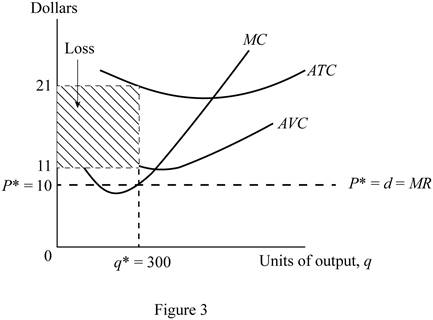

Figure 3 shows the loss incurred by the representative firm.

The horizontal axis of Figure 3 measures the quantity of output, and the vertical axis measures the price. The average variable cost curve, average total cost curve, and the marginal cost curve are plotted using the given information. The marginal revenue curve is the same as the demand curve, and the price line as the firm is perfectly competitive. It is evident that the marginal revenue curve is below the average variable cost curve. This loss if the fixed cost of the firm. The shaded region in the graph represents the loss incurred by the firm. The loss can also be calculated as the area of the shaded rectangular region.

Figure 3 reveals that equilibrium price is $11, equilibrium quantity is 300 units, and the cost per unit is $21. Thus, loss can be calculated as follows:

Thus, the loss incurred is $3,000.

Total cost: Total cost is defined as the sum of fixed cost and variable cost.

Fixed cost: Fixed cost is defined as the cost that is independent of the level of output or production of a firm.

Variable cost: Variable cost is defined as the cost that depends on the level of production or output of a firm.

Loss: Loss is defined as the excess cost incurred over the total revenue earned.

Want to see more full solutions like this?

Chapter 9 Solutions

EBK PRINCIPLES OF MICROECONOMICS

- Your marketing department has identified the following customer demographics in the following table. Construct a demand curve and determine the profit maximizing price as well as the expected profit if MC=$1. The number of customers in the target population is 10,000. Use the following demand data: Group Value Frequency Baby boomers $5 20% Generation X $4 10% Generation Y $3 10% `Tweeners $2 10% Seniors $2 10% Others $0 40%arrow_forwardYour marketing department has identified the following customer demographics in the following table. Construct a demand curve and determine the profit maximizing price as well as the expected profit if MC=$1. The number of customers in the target population is 10,000. Group Value Frequency Baby boomers $5 20% Generation X $4 10% Generation Y $3 10% `Tweeners $2 10% Seniors $2 10% Others $0 40% ur marketing department has identified the following customer demographics in the following table. Construct a demand curve and determine the profit maximizing price as well as the expected profit if MC=$1. The number of customers in the target population is 10,000.arrow_forwardTest Preparation QUESTION 2 [20] 2.1 Body Mass Index (BMI) is a summary measure of relative health. It is calculated by dividing an individual's weight (in kilograms) by the square of their height (in meters). A small sample was drawn from the population of UWC students to determine the effect of exercise on BMI score. Given the following table, find the constant and slope parameters of the sample regression function of BMI = f(Weekly exercise hours). Interpret the two estimated parameter values. X (Weekly exercise hours) Y (Body-Mass index) QUESTION 3 2 4 6 8 10 12 41 38 33 27 23 19 Derek investigates the relationship between the days (per year) absent from work (ABSENT) and the number of years taken for the worker to be promoted (PROMOTION). He interviewed a sample of 22 employees in Cape Town to obtain information on ABSENT (X) and PROMOTION (Y), and derived the following: ΣΧ ΣΥ 341 ΣΧΥ 176 ΣΧ 1187 1012 3.1 By using the OLS method, prove that the constant and slope parameters of the…arrow_forward

- QUESTION 2 2.1 [30] Mariana, a researcher at the World Health Organisation (WHO), collects information on weekly study hours (HOURS) and blood pressure level when writing a test (BLOOD) from a sample of university students across the country, before running the regression BLOOD = f(STUDY). She collects data from 5 students as listed below: X (STUDY) 2 Y (BLOOD) 4 6 8 10 141 138 133 127 123 2.1.1 By using the OLS method and the information above derive the values for parameters B1 and B2. 2.1.2 Derive the RSS (sum of squares for the residuals). 2.1.3 Hence, calculate ô 2.2 2.3 (6) (3) Further, she replicates her study and collects data from 122 students from a rival university. She derives the residuals followed by computing skewness (S) equals -1.25 and kurtosis (K) equals 8.25 for the rival university data. Conduct the Jacque-Bera test of normality at a = 0.05. (5) Upon tasked with deriving estimates of ẞ1, B2, 82 and the standard errors (SE) of ẞ1 and B₂ for the replicated data.…arrow_forwardIf you were put in charge of ensuring that the mining industry in canada becomes more sustainable over the course of the next decade (2025-2035), how would you approach this? Come up with (at least) one resolution for each of the 4 major types of conflict: social, environmental, economic, and politicalarrow_forwardHow is the mining industry related to other Canadian labour industries? Choose one other industry, (I chose Forestry)and describe how it is related to the mining industry. How do the two industries work together? Do they ever conflict, or do they work well together?arrow_forward

- What is the primary, secondary, tertiary, and quaternary levels of mining in Canada For each level, describe what types of careers are the most common, and describe what stage your industry’s main resource is in during that stagearrow_forwardHow does the mining industry in canada contribute to the Canadian economy? Describe why your industry is so important to the Canadian economy What would happen if your industry disappeared, or suffered significant layoffs?arrow_forwardWhat is already being done to make mining in canada more sustainable? What efforts are being made in order to make mining more sustainable?arrow_forward

- What are the environmental challenges the canadian mining industry face? Discuss current challenges that mining faces with regard to the environmentarrow_forwardWhat sustainability efforts have been put forth in the mining industry in canada Are your industry’s resources renewable or non-renewable? How do you know? Describe your industry’s reclamation processarrow_forwardHow does oligopolies practice non-price competition in South Africa?arrow_forward

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education