Concept explainers

Videos

Accounting for Accounts and Notes Receivable Transactions

Web Wizard, Inc., has provided information technology services for several years. The company uses the percentage of credit sales method to estimate

- a. During January, the company provided services for $40,000 on credit.

- b. On January 31, the company estimated bad debts using 1 percent of credit sales.

- c. On February 4, the company collected $20,000 of accounts receivable.

- d. On February 15, the company wrote off a $100 account receivable.

- e. During February, the company provided services for $30,000 on credit.

- f. On February 28, the company estimated bad debts using 1 percent of credit sales.

- g. On March 1, the company loaned $2,400 to an employee who signed a 6% note, due in 6 months.

- h. On March 15, the company collected $100 on the account written off one month earlier.

- i. On March 31, the company accrued interest earned on the note.

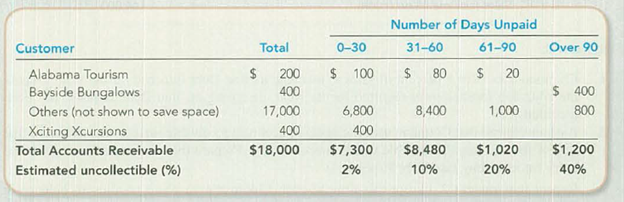

- j. On March 31, the company adjusted for uncollectible accounts, based on an aging analysis (below). Allowance for Doubtful Accounts has an unadjusted credit balance of $1,200.

Required:

- 1. For items (a)–(j), analyze the amount and direction (+ or −) of effects on specific financial statement accounts and the overall

accounting equation. - 2. Prepare

journal entries for items (a)–(j). - 3. Show how Accounts Receivable. Notes Receivable, and their related accounts would be reported in the current assets section of a classified balance sheet.

- 4. Sales Revenue and Service Revenue are two income statement accounts that relate to Accounts Receivable. Name two other accounts related to Accounts Receivable and Notes Receivable that would be reported on the income statement and indicate whether each would appear before, or after, Income from Operations.

1.

To indicate: The amount and direction of effects of each transaction from (a)-(j) on the financial statement accounts and on the overall accounting equation.

Explanation of Solution

Bad debt expense:

Bad debt expense is an expense account. The amounts of loss incurred from extending credit to the customers are recorded as bad debt expense. In other words, the estimated uncollectible accounts receivable are known as bad debt expense.

Allowance method:

It is a method for accounting bad debt expense, where amount of uncollectible accounts receivables are estimated and recorded at the end of particular period. Under this method, bad debts expenses are estimated and recorded prior to the occurrence of actual bad debt, in compliance with matching principle by using the allowance for doubtful account.

Write-off:

Write-off refers to the deduction of a certain amount from accounts receivable, when it is decided that the amount would be uncollectible forever.

Accounting equation: Accounting equation is an accounting tool expressed in the form of equation, by creating a relationship between the resources or assets of a company, and claims on the resources by the creditors and the owners. Accounting equation is expressed as shown below:

Indicate the amount and direction of effects each transactions on the financial statement accounts and on the overall accounting equation.

a.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Accounts receivable | +$40,000 | Service revenue (+R) | +$40,000 |

Table (1)

b.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Allowance for doubtful accounts (+xA) | –$400 | Bad debt expense (+E) | –$400 |

Table (2)

Working note:

Determine the amount of bad debt expense for the year.

c.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Cash | +$20,000 | |||||

| Accounts receivable | –$20,000 |

Table (3)

d.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Accounts receivable | –$100 | |||||

| Allowance for doubtful accounts (–xA) | +$100 |

Table (4)

e.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Accounts receivable | +$30,000 | Service revenue (+R) | +30,000 |

Table (5)

f.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Allowance for doubtful accounts (+xA) | –$300 | Bad debt expense (+E) | –$300 |

Table (6)

g.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Cash | –$2,400 | |||||

| Note receivable | +$2,400 |

Table (7)

h.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Accounts receivable | +$100 | |||||

| Allowance for doubtful accounts (+xA) | –$100 | |||||

| Cash | +$100 | |||||

| Accounts receivable | –$100 |

Table (8)

i.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Interest receivable | +$12 | Interest revenue (+R) | +$12 |

Table (9)

Working note:

Calculate the amount of interest revenue earned on note, as on March 31.

j.

| Assets | Amount | = | Liabilities | + | Stockholders’ equity | Amount |

| Allowance for doubtful accounts (+xA) | –$478 | Bad debt expense (+E) | –$478 |

Table (10)

Working note:

Estimate the amount of uncollectible under on the basis of aging analysis method.

| Number of days unpaid | |||||

| Total | 0–30 | 31–60 | 61–90 | Over 90 | |

| Total Accounts Receivable | $ 18,000 | $7,300 | $8,480 | $1,020 | $1,200 |

| Estimated Uncollectible (%) | |||||

| Estimated Uncollectible ($) | $ 1,678 | $146 | $848 | $204 | $480 |

Table (11)

Aging of receivables method:

A method of determining the estimated uncollectible receivables based on the age of individual accounts receivable is known as aging of receivables method. Amount of accounts receivables of different age and its respective uncollectible percentage are multiplied, to determine the estimated uncollectible receivables for each age group of receivable.

It is given that the unadjusted balance of allowance for doubtful accounts is a credit balance of $1,200. It is calculated that the estimated uncollectible is $1,678. Under aging of receivables method, estimated uncollectible would be treated as desired ending balance of allowance for doubtful accounts. To bring the balance of allowance for doubtful accounts from a credit balance of $1,200 to a credit of $1,678, allowance for doubtful accounts must be adjusted (by debiting (increasing) bad debts expenses and by crediting (increasing) allowance for doubtful accounts). So, now calculate the amount needed to be adjusted for uncollectible accounts.

Calculate the amount needed to be adjusted for uncollectible accounts.

Thus, the amount needed to be adjusted for uncollectible accounts is $478.

Note:

xA denotes contra asset account

R denotes revenue account

E denotes expenses account

2.

To prepare: Journal entries for items from (a) to (j).

Explanation of Solution

Journal: Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Prepare journal entries for items from (a) to (j) as follows:

| Item | Date | Account Title and Explanation | Debit ($) | Credit ($) |

| a. | January | Accounts Receivable (+A) | 40,000 | |

| Service Revenue (+R) | 40,000 | |||

| (To record service rendered on credit) | ||||

| b. | January 31 | Bad debt expense (+E) | 400 | |

| Allowance for doubtful accounts (+xA) | 400 | |||

| (To record the estimated bad debt expense) | ||||

| c. | February 4 | Cash (+A) | 20,000 | |

| Accounts receivable (–A) | 20,000 | |||

| (To record the collection of cash on account) | ||||

| d. | February 15 | Allowance for doubtful accounts (–xA) | 100 | |

| Accounts receivable (–A) | 100 | |||

| (To record the write off of receivables) | ||||

| e. | February | Accounts Receivable (+A) | 30,000 | |

| Service Revenue (+R) | 30,000 | |||

| (To record service rendered on credit) | ||||

| f. | February 28 | Bad debt expense (+E) | 300 | |

| Allowance for doubtful accounts (+xA) | 300 | |||

| (To record the estimated bad debt expense) | ||||

| g. | March 1 | Note Receivable (+A) | 2,400 | |

| Cash (–A) | 2,400 | |||

| (To recordthe acceptance of note) | ||||

| h. | March 15 | Accounts Receivable (+A) | 100 | |

| Allowance for doubtful accounts (+xA) | 100 | |||

| (To reverse the written off receivables) | ||||

| March 15 | Cash (+A) | 100 | ||

| Accounts receivable (–A) | 100 | |||

| (To record the collection of cash on account) | ||||

| i. | March 31 | Interest Receivable (+A) | 12 | |

| Interest Revenue (+R) | 12 | |||

| (To record accrued interest earned on note) | ||||

| j. | March 31 | Bad debt expense (+E) | 478 | |

| Allowance for doubtful accounts (+xA) | 478 | |||

| (To record the estimated bad debt expense) | ||||

Table (12)

Note:

A denotes asset account, xA denotes contra-asset account, R denotes revenue account, and E denotes expenses account.

3.

To show: How accounts receivable, notes receivable, and their related accounts would be reported in the current asset section of the classified balance sheet at the end of quarter on March 31.

Explanation of Solution

Prepare partial classified balance sheet at the end of quarter on March 31 as follows:

| Incorporation W | ||

| Classified balance sheet (Partial) | ||

| At the end of quarter on March 31 | ||

| Assets: | Amount in $ | Amount in $ |

| Current assets: | ||

| Accounts receivable | 18,000 | |

| Less: Allowance for doubtful accounts | (1,678) | |

| Accounts receivable, net of allowance | 16,322 | |

| Notes receivable | 2,400 | |

| Interest receivable | 12 | |

Table (13)

4.

To identify: Two accounts (apart from sales revenue and service revenue) that are related to accounts receivable and notes receivable that would be reported on the income statement.

Explanation of Solution

Bad debt expense:

Bad debt expense is an expense account. The amounts of loss incurred from extending credit to the customers are recorded as bad debt expense. In other words, the estimated uncollectible accounts receivable are known as bad debt expense.

Bad debt expense account is an account which is related to accounts receivables, which would be reported as bad debt expense on the income statement before income from operations.

Interest revenue account is an account which is related to notes receivables, which would be reported as interest revenue on the income statement after income from operations.

Want to see more full solutions like this?

Chapter 8 Solutions

Fundamentals of Financial Accounting

- Reading and Interpreting Audit OpinionsRivian Automotive financial statements include the following audit report from KPMG LLP. -----------------------------------------------------------------------------------------------------------------------------------------------Report of Independent Registered Public Accounting FirmTo the Stockholders and Board of DirectorsRivian Automotive, Inc.:Opinion on the Consolidated Financial Statements We have audited the accompanying consolidated balance sheets of Rivian Automotive, Inc. and subsidiaries (the Company) as of December 31, 2022 and 2021, the related consolidated statements of operations, comprehensive loss, changes in contingently redeemable convertible preferred stock and stockholders' (deficit) equity, and cash flows for each of the years in the three-year period ended December 31, 2022, and the related notes (collectively, the consolidated financial statements). In our opinion, the consolidated financial statements present fairly, in…arrow_forwardIn a recent year, Adobe Inc. reports net income of $4,756 million. Its stockholders’ equity is $14,051 million and $14,797 million at the start and end of the fiscal year, respectively. a. Compute its return on equity (ROE) for the year. Round answers to the nearest whole dollar amount. Numerator Denominator Result Return on equity Answer 1 Answer 2 b. Adobe repurchased $6,550 million of its common stock during the year. Did this repurchase increase or decrease ROE? NOTE: Assume there was no change in net income related to the stock repurchase. c. If Adobe had not repurchased common stock during the year, what would ROE have been? Note: Enter answer as a percentage rounded to the nearest one decimal place (ex: 24.8%).arrow_forwardComputing Return on Assets and Applying the Accounting Equation Nordstrom Inc. reports net income of $564 million for a recent fiscal year. At the beginning of that fiscal year, Nordstrom had $8,115 million in total assets. By fiscal year end, total assets had decreased to $7,886 million. What is Nordstrom’s ROA? Note: Enter answer as a percentage rounded to the nearest 2 decimal places (ex: 24.58%). ROA Answerarrow_forward

- Computing and Interpreting Financial Statement RatiosFollowing are selected ratios of Norfolk Southern. Return on Assets (ROA) Component FY4 FY3 Profitability (Net income/Sales) 25.7% 27.0% Productivity (Sales/Average assets) 0.329 0.291 a. Was the company profitable in FY4? Answer 1b. In which year was the company more profitable? Answer 2c. Is the change in productivity a positive or negative development? Answer 3d. Compute the company’s ROA for both years. Note: Enter your answer as a percentage rounded to one decimal place (Ex: 29.4%).FY4 Answer 4%FY3 Answer 5%e. From the information, which of the following best explains the change in ROA during FY4?arrow_forwardExpand upon it and add to itarrow_forwardDefine these terms: A) Information Asymmetry. B) Material misstatement in the audited financial statements. C) The term "Professional Skepticism." D) Contribution margin ratio. E) Gross Margin, also known as Gross Profit Margin.arrow_forward

- No Ai Which of the following errors will cause the trial balance to not balance?A. Omission of a transactionB. Entry posted twiceC. Transposing digits in one sideD. Debiting one account and crediting anotherarrow_forwardDon't use ChatGPT!! Which of the following errors will cause the trial balance to not balance?A. Omission of a transactionB. Entry posted twiceC. Transposing digits in one sideD. Debiting one account and crediting anotherarrow_forwardWhich of the following is a temporary account?A. Retained EarningsB. Service RevenueC. Accounts PayableD. Inventoryarrow_forward

- Which of the following errors will cause the trial balance to not balance?A. Omission of a transactionB. Entry posted twiceC. Transposing digits in one sideD. Debiting one account and crediting anotherarrow_forwardMime Delivery Service is owned and operated by Pamela Kolp. The following selected transactionswere completed by Mime Delivery Service during October:1. Received cash from the owner as an additional investment, $7,500.2. Paid creditors on account, $815.3. Billed customers for delivery services on account, $3,250.4. Received cash from customers on account, $1,150.5. Paid cash to the owner for personal use, $500.Required:Indicate the effect of each transaction on the accounting equation elements (Assets, Liabilities,Owner’s Equity, Drawing, Revenue, and Expense) by listing the numbers identifying the transactions,(1) to (5). Also, indicate the specific item within the accounting equation element that is affected, i.e.(1) Asset (Cash) increases by $; Owner’s Equity (Pamela Kolp, Capital) increases by $.arrow_forwardWhen a company incurs an expense but does not yet pay it, what is the entry?A. Debit Expense, Credit CashB. Debit Liability, Credit ExpenseC. Debit Expense, Credit LiabilityD. No entry needed helparrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT