Videos

Intercorporate Inventory and Debt Transfers (Effective Interest Method)

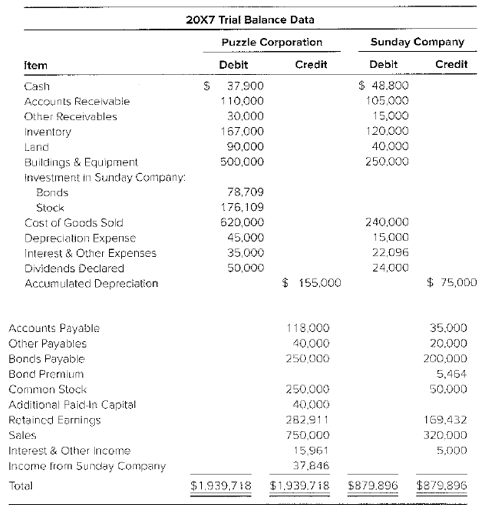

Puzzle Corporation purchased 75 percent of Sunday Company’s common stock at underlying book value on January 1, 20X3. At that date, the fair value of the noncontrolling interest was equal to 25 percent of Sunday’s book value.

During 20X7, Puzzle resold inventory purchased from Sunday in 20X6. It had cost Sunday $44,000 to produce the inventory, and Puzzle had purchased it for $59,000. In 20X7, Puzzle had purchased inventory for $40,000 and sold it to Sunday for $60,000. At December 31, 20X7. Sunday continued to hold $27,000 of the inventory.

Sunday had issued $200,000 of 8 percent, 10−year bonds on January 1, 20X4, at 104. Puzzle had purchased $80,000 of the bonds from one of the original owners for $78,400 on December 31, 20X5. Interest is paid annually on December 31. Assume Puzzle uses the fully adjusted equity method.

Required

a. What amount of cost of goods sold will be reported in the 20X7 consolidated income statement?

b. What inventory balance will be reported in the December 31, 20X7, consolidated

c. Prepare the

d. Prepare the journal entry to record interest income for Puzzle for 20X7.

e. What amount will be assigned to the noncontrolling interest in the consolidated balance sheet prepared at December 31, 20X7?

f. Prepare all consolidation entries needed at December 31, 20X7, to complete a three−part consolidation worksheet.

g. Prepare a consolidation worksheet for 20X7 in good form.

a

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

Amount of cost of goods sold to be reported in consolidated income statement.

Answer to Problem 8.25P

Cost of goods sold to be reported in consolidated income statement is $794,000

Explanation of Solution

| $ | $ | |

| Amount of cost of goods reported by P corporation | 620,000 | |

| Amount of cost of goods reported by S corporation | 240,000 | |

| Adjustment of unrealized profit on inventory purchased by P from S | (15,000) | |

| Adjustment of inventory purchased from subsidiary and resold 20X7 | ||

| CGS intercompany sales recorded by P | 40,000 | |

| CGS intercompany sales recorded by S | 33,000 | |

| Total | 73,000 | |

| CGS based on P’s cost 40,000 x (33,000 /60,000) | (22,000) | |

| Required adjustment | (51,000) | |

| Cost of goods sold | 794,000 |

b.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

Inventory balance to be reported in consolidated balance sheet December 31 20X7

Answer to Problem 8.25P

Consolidated inventory balance to be reported in consolidated balance sheet is $278,000

Explanation of Solution

| $ | |

| Amount of inventory reported by P | 167,000 |

| Amount of inventory reported by S | 120,000 |

| Total | 287,000 |

| Less: Unrealized profit in ending inventory held by S | (9,000) |

| Consolidated inventory balance | 278,000 |

c.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

Journal entry to record interest expenses by S

Explanation of Solution

| Particulars | Debit $ | Credit $ |

| Interest expense | 15,200 | |

| Bond premium | 800 | |

| Cash | 16,000 | |

| (Paid cash on account of interest expense) |

Computation of interest expenses

| Par value of bond issued | $200,000 |

| Annual Interest | $16,000 |

| Annual amortization of premium ($4,800 /6 years) | (800) |

| Interest expenses | $15,200 |

d.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

Journal entry to record interest income for S

Explanation of Solution

| Particulars | Debit $ | Credit $ |

| Cash | $6,400 | |

| Investment in A company bond | 200 | |

| Interest income | 6,600 | |

| (Received cash on account of interest income and premium on bond amortized) |

Computation of interest income

| Annual payment received | $6,400 |

| Amortization of discount | 200 |

| Interest income | $6,600 |

e.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

The income assigned to non-controlling interest in consolidated balance sheet

Answer to Problem 8.25P

Amount of income assigned to non-controlling interest $15,620

Explanation of Solution

| $ | |

| Net income reported by S | 48,000 |

| Adjustment for realization of profit on inventory sold to P | 15,000 |

| Adjustment of gain on bond retirement | (520) |

| Realized net income | 62,480 |

| Income assigned to non-controlling interest | 15,620 |

Computation of gain on bond retirement

| $ | $ | |

| Par value of bond | 200,000 | |

| Amortization per year | 800 | |

| Premium maturity value Dec 31 20X5 | 6,400 | |

| Book value of bond | 206,400 | |

| Book value of bond purchase | 82,560 | |

| Purchase price | (78,400) | |

| Gain | 4,160 |

f.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

Preparation of consolidation entries needed at December 31 20X7 to complete consolidation worksheet.

Explanation of Solution

| Particulars | Debit $ | Credit $ |

| To eliminate income from subsidiary | ||

| Income from subsidiary | 36,000 | |

| Dividends declared | 18,000 | |

| Investment in S company stock | 18,000 | |

| (Income from subsidiary eliminated by reversal) | ||

| Assign income to non-controlling interest. | ||

| Income to non-controlling interest | 15,620 | |

| Dividends declared | 6,000 | |

| Non-controlling interest | 9,620 | |

| (Income assigned to non-controlling interest) | ||

| Eliminate beginning investment balance | ||

| Common stock S company | 50,000 | |

| Retained earnings January 1 | 170,000 | |

| Investment in A’s stock | 165,000 | |

| Non-controlling interest | 55,000 | |

| (Beginning investment in S stock eliminated by reversal) | ||

| Eliminating beginning inventory profit | ||

| Retained earnings, January 1 | 11,250 | |

| Non-controlling interest | 3,750 | |

| Cost of goods sold | 15,000 | |

| (Unrealized profit on beginning inventory eliminated) | ||

| Eliminating intercompany sale of inventory by P | ||

| Sales | 60,000 | |

| Cost of goods sold | 51,000 | |

| Inventory | 9,000 | |

| (Intercompany profit on sale of inventory eliminated) | ||

| Eliminating intercompany bond holdings | ||

| Bond payable | 80,000 | |

| Bond premium | 1,920 | |

| Interest income | 6,600 | |

| Investment on S company’s bonds | 78,800 | |

| Interest expenses | 6,080 | |

| Retained earnings, January 1 | 2,730 | |

| Non-controlling interest | 910 | |

| (Intercompany bond holdings eliminated by reversal) |

- Income from subsidiary is eliminated by debiting to income from subsidiary account.

- Assignment of income to non-controlling interest

Realized net income by S company

| Net income reported by S | $48,000 |

| Realization of profit on inventory sold to P(59,000 − 44,000) | $15,000 |

| Adjustment of gain on bond retirement ($4,160 / 8 years) | (520) |

| Realized net income | 62,480 |

- Common stock and retained earnings in the beginning of the year was $170,000 and 50,000 which is $220,000 eliminating by crediting to investment in S account and non- controlling interest account in the ratio of parental and subsidiary holdings.

- Beginning inventory profit of $15,000 is eliminated as required by debiting retained earnings at 75% and non-controlling interest by 25%.

- Intercompany sale of inventory is eliminated by posting reversal entry.

- Eliminating corporate bond holding

Bond premium:

| Bond premium given | $4,800 |

| P bond discount 80,000 − 78,400 | (1,600) |

| Net premium on bond | $3,200 |

Calculation of bond investment value:

| Bonds purchase consideration | $78,400 |

| Amortization of discount (1,600 / 8 years) | 200 |

| Bond investment value | $78,800 |

Calculation of interest expenses:

| $6,400 | |

| Less amortization of premium ($3,200 / 10 years) | (320) |

| Interest expenses | $6,080 |

g.

Introduction: When one business organization holds majority shareholdings in another company, the management can transfer resources between these two businesses. One way of resource transfer is debt transfer from one affiliate to another without third party involvement. Debt transfer may also include setoff of trade receivable, payables arising from the intercompany sale of inventory on credit and the issue of notes payable to each other in exchange for operating funds.

The preparation of consolidation worksheet for 20X7

Answer to Problem 8.25P

The following are the balances reported in consolidation work sheet for 20X7:

- Retained earnings $337,040

- Total Assets $1,274,700

Explanation of Solution

P Corporation and S Corporation

Consolidation worksheet

December 31, 20X7

| Elimination | |||||

| P $ | S $ | Debit $ | Credit $ | Consolidation $ | |

| Sales | 750,000 | 320,000 | 60,000 | 1,010,000 | |

| Interest and other income | 16,000 | 5,000 | 6,600 | 14,400 | |

| Income from subsidiary | 36,000 | 36,000 | |||

| 802,000 | 325,000 | 1,024,400 | |||

| Less: Cost of goods sold | (620,000) | (240,000) | 15,000 | ||

| 51,000 | (794,000) | ||||

| Depreciation expenses | (45,000) | (15,000) | (60,000) | ||

| Interest and other expenses | (35,000) | (22,000) | 6,080 | (50,920) | |

| Consolidated net income | $119,480 | ||||

| Income to NCI | 15,620 | (15,620) | |||

| Net income | 102,000 | 48,000 | 118,220 | 72,080 | 103,860 |

| Retained earnings Jan 1 | 291,700 | 170,000 | 170,000 | 2,730 | |

| 11,250 | 283,180 | ||||

| 393,700 | 218,000 | 387,040 | |||

| Dividends declared | (50,000) | (24,000) | 18,000 | ||

| 6,000 | (50,000) | ||||

| Retained earnings Dec 31 | 343,700 | 194,000 | 299,470 | 98,810 | 337,040 |

| Balance sheet: | |||||

| Cash | 37,900 | 48,800 | 86,700 | ||

| Accounts receivable | 110,000 | 105,000 | 215,000 | ||

| Other receivable | 30,000 | 15,000 | 45,000 | ||

| Inventory | 167,000 | 120,000 | 9,000 | 278,000 | |

| Land | 90,000 | 40,000 | 130,000 | ||

| Investment in S’s bonds | 78,800 | 78,800 | |||

| Investment in S’s Stock | 183,000 | 18,000 | |||

| 165,000 | |||||

| Buildings and Equipment | 500,000 | 250,000 | 750,000 | ||

| Less Accumulated Depreciation | (155,000) | (75,000) | (230,000) | ||

| Total Assets | 1,041,700 | 175,000 | 1,274,700 | ||

| Accounts payable | 118,000 | 35,000 | 153,000 | ||

| Other payable | 40,000 | 20,000 | 60,000 | ||

| Bonds payable | 250,000 | 200,000 | 80,000 | 370,000 | |

| Bonds premium | 4,800 | 1,920 | 2,880 | ||

| Common Stock: | |||||

| P company | 250,000 | 250,000 | |||

| S company | 50,000 | 50,000 | |||

| Additional Paid in capital | 40,000 | 40,000 | |||

| Retained earnings Dec 31 | 343,700 | 194,000 | 299,470 | 98,810 | 337,040 |

| Non-controlling interest | 3,750 | 9,620 | |||

| 55,000 | |||||

| 910 | 61,780 | ||||

| Total Liability and Equity | 1,041,700 | 175,000 | 1,274,700 | ||

Want to see more full solutions like this?

Chapter 8 Solutions

ADVANCED FINANCIAL ACCT.(LL) >CUSTOM<

- In determining whether § 357(c) applies, assess whether the liabilities involved exceed the bases of all assets a shareholder transfers to the corporation./ Provide explanation please. a. True b. Falsearrow_forwardI will unhelpful if wrong.arrow_forwardplease don't solve using wrong values i will mark as unhelpful.arrow_forward

- Bansai, age 66, retires and receives a $1,450 per month annuity from his employer's qualified pension plan. Bansai made $87,600 of after-tax contributions to the plan before retirement. Under the simplified method, Bansai's number of anticipated payments is 240. What is the amount includible in income in the first year of withdrawals assuming 12 monthly payments? A. $10,560 B. $12,540 C. $17,400 D. $8,220arrow_forwardWhat is the cost of goods sold?arrow_forwardCan you help me find the accurate solution to this financial accounting problem using valid principles?arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education