Concept explainers

Compute the missing amount of “schedule of changes in the County’s Net pension liability and related ratios”.

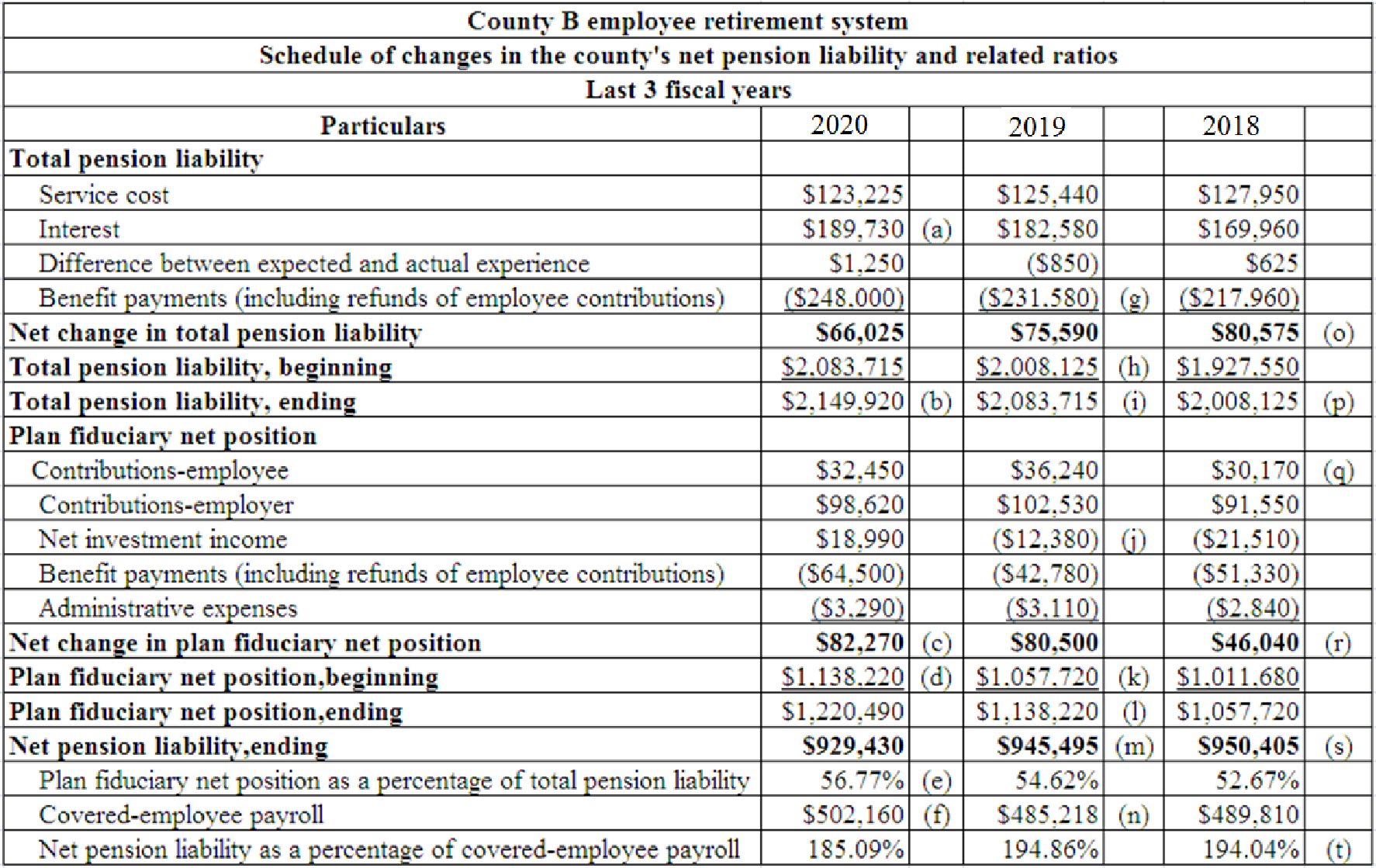

Explanation of Solution

Fiduciary activities: Fiduciary activities are those activities done by persons or organizations to another parties with utmost good faith and trust. A fiduciary activity may involve managing funds, assets and other valuables of a person or a group of people.

The person or organization involved in fiduciary activities need to act ethically in the best interest of others. Government also involve in fiduciary activities by holding the assets of individuals or organization to benefit them.

Prepare the financial statement of County B:

Table (1)

Working note (a): Calculate interest during the year 2020:

Interest amount is calculated by deducting all other pension liabilities from net change in total pension liability. Total pension liabilities except interest includes service costs, difference between expected and experience, and benefit payments. The amount of service cost is $123,225, difference between expected and experience is $1,250, and benefit payment is -$248,000. The net change in total pension liability is $66,205.

Calculation of interest is as follows:

Hence, the interest amount is $189,730.

Working note (b): Calculate net change in plan fiduciary net position:

Net change in plan fiduciary net position is the difference between plan fiduciary net position at the end of the year and plan fiduciary net position at the beginning of the year. Plan fiduciary net position at the ending is $1,057,720. Plan fiduciary net position at the beginning is $1,011,680.

Calculation of net change in plan fiduciary net position is as follows:

Hence, the net change in plan fiduciary net position is $46,040.

Working note (c): Calculate net change in plan fiduciary net position:

Net change in plan fiduciary net position is the difference between plan fiduciary net position incomes and plan fiduciary net position expenses. Plan fiduciary net position income includes contribution from employee $32,450, contribution from employers $98,620, and net investment income $18,990. Plan fiduciary net position expenses include benefit payments of $64,500 and administrative expenses of $3,290.

Calculation of net change in plan fiduciary net position is as follows:

Hence, the net change in plan fiduciary net position is $82,270.

Working note (d): Calculate plan fiduciary net position at the beginning of the year 2020:

Plan fiduciary net position at the beginning is computed as the difference between plan fiduciary net position at the end of the year and net change in plan fiduciary net position. Plan fiduciary net position at the end of the year is $1,220,490.

Calculation of plan fiduciary net position at the beginning is as given below:

Hence, the plan fiduciary net position at the beginning of the year 2020 is $1,138,220.

Working note (e): Calculate plan fiduciary net position as the percentage of total pension liability:

Plan fiduciary net position as a percentage of total pension liability is calculated by dividing plan fiduciary net position at the end of the year by total pension liability at the end of the year. Plan fiduciary net position at the end of the year is given as $1,220,490 and total pension liability at the end of the year is calculated as $2,149,920.

Calculate plan fiduciary net position as the percentage of total pension liability:

Hence, the plan fiduciary net position as percentage of total pension liability is 56.77%.

Working note (f): Calculate covered-employee payroll:

The calculation of covered-employee payroll is by dividing net pension liability at the ending by net pension liability as a percentage of covered-employee payrolls. Net pension liability at the ending is given as $929,430 and net pension liability as a percentage of covered-employee payrolls is 185.09%.

Calculate covered-employee payroll:

Hence, the covered-employee payroll is $502,150.

Working note (g): Calculate benefit payment for the year 2019:

Benefit payment is calculated by deducting all other pension liabilities from net change in total pension liability. Total pension liabilities except benefit payment includes service costs, interest, and difference between expected and experience. The amount of service cost is $125,440, interest amount is $182,580, and difference between expected and experience is -$850, and benefit payment is -$248,000. The net change in total pension liability is $75,590.

Calculate benefit payment for the year 2019:

Hence, the benefit payment for the year 2019 is ($231,580).

Working note (h): Calculate total pension liability at the beginning of the year 2019:

Total pension liability at the beginning of the year is computed as the difference between total pension liability at the end of the year and net change in total pension liability. The total pension liability at the ending is $2,083,715. The calculation is as follows:

Calculate total pension liability at the beginning of the year 2019:

Hence, the total pension liability at the beginning of the year is $2,008,125.

Working note (i): Calculate total pension liability at the end of the year 2019:

The total pension liability at the end of the year 2019 will be the same as the total pension liability at the beginning of the year 2020. The total pension liability at the beginning of the year 2020 is $2,083,715. Hence, the total pension liability at the end of the year 2019 is also $2,083,175.

Working note (j): Calculate net investment income for 2019:

Net investment income is the difference between net change in plan fiduciary net position and the difference between plan fiduciary net position incomes and plan fiduciary net position expenses. Plan fiduciary net position income includes contribution from employee $36,240, contribution from employers $102,530. Plan fiduciary net position expenses include benefit payments of -$42,780 and administrative expenses of -$3,110. The net change in plan fiduciary net position is given as $80,500.

Calculate net investment income for 2019:

Hence, the net investment income for 2019 is ($12,380).

Working note (k): Calculate plan fiduciary net position at the beginning of 2019:

The plan fiduciary net position at the beginning of the year 2019 will be the same as the plan fiduciary net position at the end of the year 2018. The plan fiduciary net position at the end of the year 2018 is $1,057,720. Hence, the plan fiduciary net position at the beginning of the year 2019 is also $1,057,720.

Working note (l): Calculate plan fiduciary net position at the end of the year 2019:

Plan fiduciary net position at the ending is computed as the sum of plan fiduciary net position at the beginning of the year and net change in plan fiduciary net position. Plan fiduciary net position at the beginning of the year is $1,057,720.

Calculation of plan fiduciary net position at the beginning is as given below:

Hence, the plan fiduciary net position at the end of the year 2019 is $1,138,220.

Working note (m): Calculate net pension liability at the end of the year 2019:

Net pension liability at the end of the year 2019 is calculated as the difference between total pension liability at the ending of 2019 and plan fiduciary net position at the ending. Total pension liability at the ending of 2019 is calculated as $2,083,715 and plan fiduciary net position at the ending of 2019 is $1,138,220.

Calculate net pension liability at the end of the year 2019:

Hence, the net pension liability at the end of the year 2019 is $945,495.

Working note (n): Calculate covered-employee payroll:

The calculation of covered-employee payroll is by dividing net pension liability at the ending by net pension liability as a percentage of covered-employee payrolls. Net pension liability at the ending is given as $945,495 and net pension liability as a percentage of covered-employee payrolls is 194.86%.

Calculate covered-employee payroll:

Hence, the covered-employee payroll is $485,218.

Working note (o): Calculate net change in total pension liability for the year 2018:

Net change in total pension liability is calculated by deducting benefit payment from all other pension liabilities. Total pension liabilities except benefit payment includes service costs, interest, and difference between expected and experience. The amount of service cost is $127,950, interest amount is $169,960, and difference between expected and experience is $625. The benefit payment is given as -$217,960.

Calculate net change in total pension liability for the year 2018:

Hence, the net change in total pension liability for the year 2018 is $80,575.

Working note (p): Calculate total pension liability at the end of the year 2018:

The total pension liability at the end of the year 2018 will be the same as the total pension liability at the beginning of the year 2019. The total pension liability at the beginning of the year 2019 is $2,008,125. Hence, the total pension liability at the end of the year 2018 is also $2,008,125.

Working note (q): Calculate contribution from employees for 2018:

Contribution from employees is calculated as the difference between net change in plan fiduciary net position and the difference between plan fiduciary net position incomes and plan fiduciary net position expenses. Plan fiduciary net position income includes contribution from employers $91,550 and net investment income is -$21,510. Plan fiduciary net position expenses include benefit payments of -$51,330 and administrative expenses of -$2,840. The net change in plan fiduciary net position is calculated as $46,040.

Calculate contribution from employees for 2018:

Hence, the contribution from employee for 2018 is $30,170.

Working note (r): Calculate net change in plan fiduciary net position:

Net change in plan fiduciary net position is the difference between plan fiduciary net position at the end of the year and plan fiduciary net position at the beginning of the year. Plan fiduciary net position at the ending is $1,057,720. Plan fiduciary net position at the beginning is $1,011,680.

Calculation of net change in plan fiduciary net position is as follows:

Hence, the net change in plan fiduciary net position is $46,040.

Working note (s): Calculate net pension liability at the end of the year 2018:

Net pension liability at the end of the year 2018 is calculated as the difference between total pension liability at the ending of 2018 and plan fiduciary net position at the ending. Total pension liability at the ending of 2018 is calculated as $2,008,125 and plan fiduciary net position at the ending of 2018 is $1,057,720.

Calculation of net pension liability at the end of the year 2018 is as given below:

Hence, the net pension liability at the end of the year 2018 is $950,405.

Working note (t): Calculate net pension liability as a percentage of covered-employee payrolls:

The calculation of net pension liability as a percentage of covered-employee payroll is by dividing net pension liability at the ending by covered-employee payroll. Net pension liability at the ending is given as $950,405 and covered-employee payroll is $489,810. The calculation of covered-employee payroll is as follows:

Hence, the net pension liability as a percentage of covered-employee payrolls is 194.04%.

Want to see more full solutions like this?

Chapter 8 Solutions

Accounting For Governmental & Nonprofit Entities

- Davis Company reported an increase of $350,000 in its accounts receivable during the year 2023. The company's statement of cash flows for 2023 reported $980,000 of cash received from customers. What amount of net sales must Davis have recorded in 2023?arrow_forwardRoosevelt Equipment Ltd. manufactures industrial cranes. The standard for a specific crane model calls for 30 direct labor hours at $22 per direct labor hour. During a recent period, 400 cranes were produced. The labor rate variance was zero, and the labor efficiency variance was $8,800 unfavorable. How many actual direct labor hours were worked?arrow_forwardNolan Industries assigns overhead costs to jobs on the basis of 140% of direct labor costs. The job cost sheet for Job 627 includes $31,200 in direct materials cost and $18,500 in direct labor cost. A total of 2,500 units were produced in Job 627. Required: a. What is the total manufacturing cost assigned to Job 627? b. What is the unit product cost for Job 627?arrow_forward

- Carlisle Services reported revenues of $78,000, expenses of $72,500, and dividends of $5,800 for the month ended February 28, 2024. Carlisle Services experienced a net income or net loss of what amount?arrow_forwardSolve this accounting issuearrow_forwardHi experts provide correct answer this accounting questionarrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education