a.1.

To explain: The reason for Treasury bill’s return is independent of the state of the economy and whether treasury bills give a completely risk-free return.

Risk and Return:

The risk and return are two closely related terms. The risk is the uncertainty attached to an event. In case of any investment, there is some amount of risk attached to it as there can be either gain or loss. While return in the financial term is that percentage which represents the profit in an investment. Higher risk is related to higher return and lower risk has aprobability of lower return. The investor has to face a tradeoff between risk and return in terms of an investment.

Treasury bills:

The treasury bills are those short-term bonds or securities which have maturity period of less than one year. These are issued by the government for a shorter period and when thegovernment needs to raise funds immediately.

a.1.

Answer to Problem 23IC

- The 3% Treasury bill does not rely on the economic conditions because the treasury must and will redeem the bills at par apart from the state of the economy.

- The Treasury bills are risk-free return completely as the 3% return will be realized in all the possible economic states.

- The treasury bills cannot give a completely risk-free return as a security cannot be totally risk-free.

- Only the tax-exempt bonds or the inflation-indexed bonds would be riskless.

Explanation of Solution

- The treasury bills are the return, which is composed of real risk-free rate, in which 3% is risk-free rate.

- There is uncertainty about inflation, so it is not possible that the expected realized

rate of return would be 3%. - If the average of the inflation is 3.5% over the year, then the realized rate of return will be 2%,not the expected 3%.

- In terms of the

purchasing power , the Treasury-bills are riskless. - When the rates decline after an investment in a portfolio of treasury bills, the nominal income would also fall.

- The treasury bills are exposed to reinvestment rate risk.

Thus, the Treasury-bills will not depend on the economic condition as the treasury bills must and will redeem at par. All securities are exposed to some type of risk, so treasury bills cannot give a completely risk-free return.

2.

To explain: The reason for H’s returns expected to move with the economy and C’s returns expected to move counter to the economy.

2.

Answer to Problem 23IC

- The H’s returns are positively correlated with the economy, as the sales of the firm and its profits will experience the same kind of fluctuations as will the economy.

- The C Company is considered by most of the investors as a hedge against both bad times and high inflation, so in case the stock crashes the investors will do relatively well.

Explanation of Solution

- There are two kinds of correlation one is positive correlation and other is anegative correlation.

- When return is correlated positively, they will move with the economy and when they are correlated negatively, they move counter the economy.

Thus, as H’s return is positively correlated, it will move with the economy and as C’s returns are negatively correlated, it will move counter the economy.

b.

To determine: The expected rate of return for each alternative.

The Expected Return on theStock:

The expected return on stock refers to the weighted average of expected

b.

Explanation of Solution

Theformula to calculate the expected rate of return is,

Where,

-

-

-

- N is the number of states.

Calculate the expected rate of return for H.

Substitute 0.1, 0.2, 0.4, 0.2 and 0.1 for the probability and (29.5%), (9.5%), 12.5%, 27.5% and 42.5% for rates in the above given formula.

The expected rate of return is 9.9%.

Calculate the expected rate of return for T-bills.

Substitute 0.1, 0.2, 0.4, 0.2 and 0.1 for the probability and 3% for all rates in the above given formula.

The expected rate of return is 3%.

The value filled in the table is as:

| State of economy | Probability | T-bills | H | C | U | MP | 2-stock P |

| Recession | 0.1 | 3.0% | (29.5%) | 24.5% | 3.5% | (19.5%) | (2.5%) |

| Below average | 0.2 | 3.0% | (9.5%) | 10.5% | (16.5%) | (5.5%) | |

| Average | 0.4 | 3.0% | 12.5% | (1.0)% | 0.5% | 7.5% | 5.8% |

| Above average | 0.2 | 3.0% | 27.5% | (5.0%) | 38.5% | 22.5% | |

| Boom | 0.1 | 3.0% | 42.5% | (20.0%) | 23.5% | 35.5% | 11.3% |

|

| 3.0% | 9.9% | 1.2% | 7.3% | 8.0% | ||

|

| 0.0 | 11.2 | 18.8 | 15.2 | 4.6 | ||

| CV | 9.8 | 2.6 | 1.9 | 0.8 | |||

| b | -0.50 | 0.88 |

Table (1)

Thus, the expected rate of return for H and T-bills is 9.9% and 3%.

c.1.

To determine: The standard deviation of returns.

Standard Deviation:

The standard deviation refers to the stand-alone risk associated with the securities. It measures how much a data is dispersed with its standard value. The Greek letter sigma represents the standard deviation.

c.1.

Explanation of Solution

The formula to calculate the standard deviation is,

Where,

-

-

-

-

- N is the number of states.

Calculation of standard deviation for H,

The standard deviation for H is 20.03%.

The value of

| State of economy | Probability | T-bills | H | C | U | MP | 2-stock P |

| Recession | 0.1 | 3.0% | (29.5%) | 24.5% | 3.5% | (19.5%) | (2.5%) |

| Below average | 0.2 | 3.0% | (9.5%) | 10.5% | (16.5%) | (5.5%) | |

| Average | 0.4 | 3.0% | 12.5% | (1.0)% | 0.5% | 7.5% | 5.8% |

| Above average | 0.2 | 3.0% | 27.5% | (5.0%) | 38.5% | 22.5% | |

| Boom | 0.1 | 3.0% | 42.5% | (20.0%) | 23.5% | 35.5% | 11.3% |

|

| 3.0% | 9.9% | 1.2% | 7.3% | 8.0% | ||

|

| 0.0 | 20.03 | 11.2 | 18.8 | 15.2 | 4.6 | |

| CV | 9.8 | 2.6 | 1.9 | 0.8 | |||

| b | -0.50 | 0.88 |

Table (2)

The standard deviation for H is20.03%.

2.

To explain: The type of risk measured by the standard deviation.

2.

Answer to Problem 23IC

The stand-alone risk of a portfolio is measured by the standard deviation.

Explanation of Solution

- The standard deviation is a measure of the risk of a security.

- The greater is the standard deviation, the higher is the chance that actual returns will be below the expected return.

- It also shows that there will be losses rather than profits.

Thus, the stand-alone risk is measured by the standard deviation.

3.

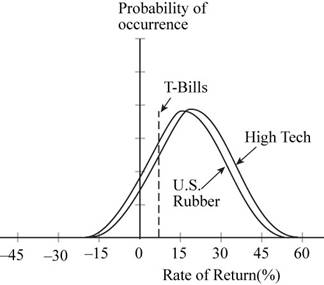

To prepare: A graph showing the probability distribution for H, U, and T.

3.

Answer to Problem 23IC

The graph showing the probability distribution is:

Fig 1

Explanation of Solution

- The graph shows the probability distribution for the given companies.

- The X-axis shows the rate of return in percentage.

- The Y-axis shows the occurrence.

- On the basis of the graph, the H is the riskiest investment.

- The T has the less risky investment.

Thus, the graph for aprobability distribution is as mentioned above and according to the graph, H is the riskiest investment andT is the least risky investment.

d.

To determine: The missing values of coefficient of variation and comparison of risk rankings of the coefficient of variation with the standard deviation.

The Coefficient of Variation:

The coefficient of variation is a tool to determine the risk. It determines the risk per unit of return. It is used for measurement when the expected returns are same for two data.

d.

Explanation of Solution

Given,

For T-bills,

The standard deviation is 0.0%.

The expected rate of return is 3%.

For H,

The standard deviation is 20.03%.

The expected rate of return is 9.9%.

The formula to calculate the coefficient of variation is,

Calculatethe coefficient of variation for T-bills.

Substitute 0.0% for the standard deviation and 3% for the expected rate of return in the above formula.

The coefficient of variation for T-bills is 0.0.

Calculate coefficient of variation for H.

Substitute 20.03% for the standard deviation and 9.9% for the expected rate of return in the above formula.

The coefficient of variation for H is 2.02.

The table with the missing values is as:

| State of economy | Probability | T-bills | H | C | U | MP | 2-stock P |

| Recession | 0.1 | 3.0% | (29.5%) | 24.5% | 3.5% | (19.5%) | (2.5%) |

| Below average | 0.2 | 3.0% | (9.5%) | 10.5% | (16.5%) | (5.5%) | |

| Average | 0.4 | 3.0% | 12.5% | (1.0)% | 0.5% | 7.5% | 5.8% |

| Above average | 0.2 | 3.0% | 27.5% | (5.0%) | 38.5% | 22.5% | |

| Boom | 0.1 | 3.0% | 42.5% | (20.0%) | 23.5% | 35.5% | 11.3% |

|

| 3.0% | 9.9% | 1.2% | 7.3% | 8.0% | ||

|

| 0.0 | 20.03 | 11.2 | 18.8 | 15.2 | 4.6 | |

| CV | 0.0 | 2.02 | 9.8 | 2.6 | 1.9 | 0.8 | |

| b | -0.50 | 0.88 |

Table (3)

The coefficient of variation for T-bills is 0.0 and for H is 2.02.

e.1.

The Expected Return on theStock:

The expected return on stock refers to the weighted average of expected returns on those assets which are held in the portfolio.

Standard Deviation:

The standard deviation refers to the stand-alone risk associated with the securities. It measures how much a data is dispersed with its standard value. The Greek letter sigma represents the standard deviation.

The Coefficient of Variation:

The coefficient of variation is a tool to determine the risk. It determines the risk per unit of return. It is used for measurement when the expected returns are same for two data.

e.1.

Explanation of Solution

Given,

A 2-stock portfolio is created.

The investment in H is $50,000.

The investment in C is $50,000.

The formula to calculate the expected rate of return is,

Where,

Calculate the expected rate of return for recession.

Substitute 0.5 for the weight and 9.9% and 1.2% for the rates in the above formula.

The expected rate of return is 5.55%.

Calculate the standard deviation for the2-stock portfolio.

The formula to calculate the standard deviation is,

Where,

Substitute 0.1, 0.2, 0.4, 0.2 and 0.1 for the different

The standard deviation is 4.63%.

Calculate the coefficient of variation for the 2-stock portfolio.

Calculated,

The expected rate of return is 5.55%.

The standard deviation is 4.63%.

The formula to calculate the coefficient of variation is,

Substitute 5.55% for the standard deviation and 4.63% for the expected rate of return in the above formula.

The coefficient of variation is 1.198.

The table showing the missing values is:

| State of economy | Probability | T-bills | H | C | U | MP | 2-stock P |

| Recession | 0.1 | 3.0% | (29.5%) | 24.5% | 3.5% | (19.5%) | (2.5%) |

| Below average | 0.2 | 3.0% | (9.5%) | 10.5% | (16.5%) | (5.5%) | 0.5% |

| Average | 0.4 | 3.0% | 12.5% | (1.0)% | 0.5% | 7.5% | 5.8% |

| Above average | 0.2 | 3.0% | 27.5% | (5.0%) | 38.5% | 22.5% | 11.25% |

| Boom | 0.1 | 3.0% | 42.5% | (20.0%) | 23.5% | 35.5% | 11.3% |

|

| 3.0% | 9.9% | 1.2% | 7.3% | 8.0% | 5.55% | |

|

| 0.0 | 20.03 | 11.2 | 18.8 | 15.2 | 4.6 | |

| CV | 0.0 | 2.02 | 9.8 | 2.6 | 1.9 | 0.8 | |

| b | -0.50 | 0.88 |

Table (4)

Working note:

Calculate the portfolio returns for each state of the economy.

The formula to calculate the portfolio return is,

Calculate the portfolio return for below average.

Substitute 0.5 for weights and (-9.5%) for therate of H and 10.5% for C in the above formula.

The portfolio return is 0.5%.

Calculate the portfolio return for above average.

Substitute 0.5 for weights and 27.5% for therate of H and (-5%) for therate of C in the above formula.

The portfolio return is 11.25%.

The table of the economy states and their portfolio return is:

| State | Portfolio |

| Recession | (2.5%) |

| Below average | 0.5% |

| Average | 5.8% |

| Above average | 11.25% |

| Boom | 11.3% |

Table (5)

The expected rate of return, standard deviation, and coefficient of variation for the2-stock portfolio is 5.55%, 4.63% and 1.198 respectively.

2.

To explain: The comparison of the riskiness of the 2-stock portfolios with the riskiness of the individual stock.

2.

Answer to Problem 23IC

The comparison of the riskiness of the 2-stock portfolio with the riskiness of the individual stock is explained below:

- The stand-alone risk of the portfolio is significantly less than the stand-alone risk of the individual stocks.

- The stocks are negatively correlated.

- If the stocks were held in isolation, the combination of the two stocks diversifies the inherent risks.

Explanation of Solution

- The stand-alone risk is measured by the standard deviation and coefficient of variation.

- The negative correlation of the stocks means that when one company is doing bad the other is doing well and vice-versa.

- The isolation of the stocks means that there is a one-stock portfolio.

Thus, if held in isolation, the 2-stock portfolio is less risky compared to the individual stocks.

f. 1.

To explain: The effect on riskiness and to the expected return of the portfolio.

f. 1.

Answer to Problem 23IC

Given,

The investor begins with a portfolio that has one randomly selected stock.

- There is a positive correlation of stocks with one another if the economy does well, and so is the effect on general stocks and vice-versa.

- When the additional stocks are added to the portfolio, the portfolio’s standard deviation declines because the added stocks are not perfectly and positively correlated.

- As more and more stocks are added, each new stock has a less of a risk-reducing impact, and eventually, theaddition of the stocks has virtually no effect on the portfolio’s risk which is measured by the standard deviation.

Explanation of Solution

- The correlation coefficient between the stocks generally ranges in +0.35. A single stock selected at random would have a standard deviation of about 35%.

- The addition of additional shares to the portfolio decreases the standard deviation of the portfolio.

- When the combination of the stocks is made into well-diversified portfolios, the standard deviation stabilizes.

- The standard deviation stabilizes at about 20% when 40 or more randomly selected stocks are added.

Thus, the risk will reduce when the stocks are randomly added.

2.

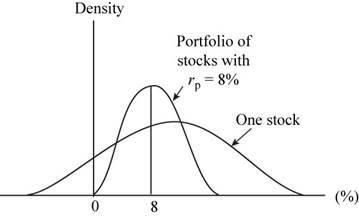

To explain: The implication for investors and the graph of the two portfolios.

2.

Answer to Problem 23IC

The graph showing the two portfolios is:

Fig 2

The implication on the investors is that the investors must hold well-diversified portfolios of stocks rather than the individual stocks.

Explanation of Solution

- The graph represents the portfolio of one stock and the portfolio of the added stocks.

- The X-axis represents the percentage of the portfolio.

- The Y-axis represents the density of the portfolio.

- The standard deviation gets smaller as more stocks are combined in the portfolio when the return on the portfolio remains constant.

- The return on theportfolio is 8% and the value is constant.

- When stocks are added to the portfolio, the risk gets reduced.

Thus, the graph of the two portfolios is shown above and the implication for investors is that the investors should hold well-diversified portfolios rather than holding the individual stocks.

g. 1.

To explain: The impact of the portfolio on the thinking of the investors.

g. 1.

Answer to Problem 23IC

- The diversification of the portfolio affects the investor’s view towards risk.

- The standard deviation and coefficient of variation may be significant to the undiversified investor but is not appropriate to a well-diversified investor.

- A rational, risk-averse investor is more interested in the effect that the stock has on the riskiness of the portfolio than the stand-alone risk of the stock.

Explanation of Solution

- The diversification of a portfolio has lot of effects on the investor’s view of risk.

- The stand-alone risk is measured by the standard deviation and the coefficient of variation.

- The stand-alone risk is composed of diversifiable risk, which can be removed by holding a stock in a well-diversified portfolio.

Thus, the risk called as market risk is present when the entire market portfolio is held.

2.

To explain: The possibilities of earning a risk premium and the compensation of the risk.

2.

Answer to Problem 23IC

- When a person holds a one-stock portfolio, the person or the investor is exposed to a higher degree of risk and that risk will not be compensated.

- If the returns are high enough for the compensation of higher risk, the bargain would be more rational for the diversified investors.

- So, the possibility of earning a risk premium is not easy and the compensation will not be done for the higher risk.

Explanation of Solution

- If the returns are that high that the high risk can be compensated, that would be a bargain for a rational and more diversified investor.

- The investors would start purchasing the portfolio and this increase in orders would drive the price up and the return down.

Thus, it is difficult to find the stocks in the market with returns high enough to pay for the diversifiable risk of the stock.

h. 1.

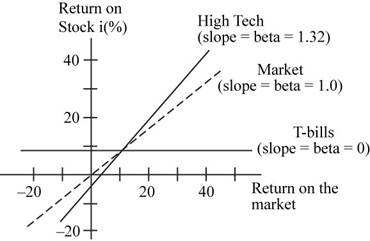

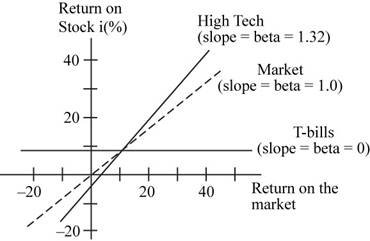

To determine: The beta coefficient and the use of beta for the risk analysis.

h. 1.

Answer to Problem 23IC

- The average beta of the stock is 1.0. Most stocks have a beta range of 0.5 to 1.5.

- The beta value can be theoretically negative but they are generally positive in the real world.

This is shown in the graph below:

Fig 3

Explanation of Solution

- The graph represents the calculation of the value of the beta.

- The X-axis represents the return on the market.

- The Y-axis represents the return on thestock.

- The average stock moves with the market.

- The value of the beta is calculated as the slope of the regression line which shows the relationship between the given stock and the general stock market.

- The slopes should be estimated and the slope should be used to calculate the value of beta.

Thus, the average beta of the stock would be 1.0.

2.

To explain: The relation of the expected return to each alternative market risk.

2.

Answer to Problem 23IC

- The expected returns are associated to each alternative’s market risk.

- This means that higher is the alternative’s rate of return, higher is the beta.

- The treasury bills have zero risks.

Explanation of Solution

- The expected returns are the return which is expected to be earned minimum on a portfolio.

- The market risk refers to that risk which the investor can experience when the overall market performance is influenced.

- The expected returns are related to the market risk as the factors affecting the market influence the minimum return rate to be earned.

Thus, the expected returns are associated to each alternative market risk.

3.

To explain: The graph showing the calculation of the beta coefficient and the measure of the betas and use of them in the risk analysis.

3.

Answer to Problem 23IC

The graph showing the calculation of the beta coefficient is:

Fig 4

- No, it is not possible to select among the alternatives on the basis of the information which is developed so far.

- The required rates of return are needed on these alternatives and then acomparison of them with their expected returns is needed.

Explanation of Solution

- The graph shows the calculation of the beta coefficient for the given data.

- The X-axis represents the return on the market.

- The Y-axis represents the return on the stock.

- The points are plotted on the graph for the market on a

- The points are then connected, and the slope is made.

- By the help of the slope, the value of beta is calculated as 1.0

Thus, the calculation of the beta coefficient is shown by the graph above and the required rate of return is needed to compare the alternatives with the expected return.

i. 1.

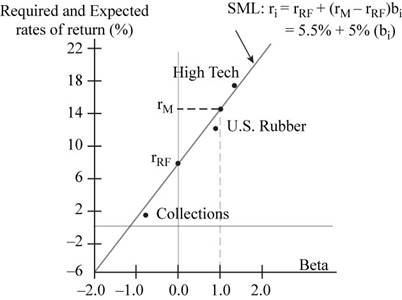

To determine: The security-market line equation, the calculation of the required rate of return on every alternative and the graph showing the relationship between the expected and required rates of return.

i. 1.

Explanation of Solution

Given,

The long-term Treasury bonds have a 3.0% yield.

The assumed risk-free rate is 3.0%.

The security market line equation is,

Where,

The risk-free rate is 3.0%.

The market return rate is 8.0%.

The market risk premium is 5%

Calculate the required rate of return for H.

Substitute 3% for

The required rate of return is 9.6%.

Calculate the required rate of return for M.

Substitute 3% for

The required rate of return is 8%.

Calculate the required rate of return for U.

Substitute 3% for

The required rate of return is 7.4%.

Calculate the required rate of return for T-bills.

Substitute 3% for

The required rate of return is 3%.

Calculate the required rate of return for C.

Substitute 3% for

The required rate of return is 0.5%.

The graph showing the relationship between expected return and required rate of return is:

Fig 5

- The graph shows the relationship between the required rate and expected return.

- The X-axis shows the value of beta.

- The Y-axis shows the required and expected rates of return.

- The slope shows the security market line equation.

- The X-axis is extended to the left of zero. This shows that there is a negative beta stock and the required return is less than the risk-free rate.

Thus, the security market line equation and the graph showing the relationship is described above and the required rate of return calculated for H, M, U, T-bills,and C is 9.6%, 8.0%, 7.4%, 3.0% and 0.5%.

2.

To determine: The comparison between the expected rates of return and the required rate of return.

2.

Explanation of Solution

The relationship between the expected rate of return and the required return is shown in the following table:

| Security |

Expected return

|

Required return

| Condition |

| H | 9.9% | 9.6% | Undervalued as

|

| M | 8.0% | 8.0% | Fairly valued as

|

| U | 7.3% | 7.4% | Overvalued as

|

| T-bills | 3.0% | 3.0% | Fairly valued as

|

| C | 1.2% | 0.5% | Overvalued as

|

Table (6)

Thus, the comparison is shown in the table above.

3.

To explain: The sense of the fact that C has an expected return less than T-bills.

3.

Answer to Problem 23IC

- The C has a negative beta value which indicates that there is anegative market risk.

- The inclusion of the stock of C in a normal portfolio will lower the risk of the portfolio.

- The C has an expected return less than T-bills have a sense that the stock C will affect the normal portfolio more than T-bills.

Explanation of Solution

- The C has a stock which is very interesting.

- This stock has a negative beta.

- This means that C is a valuable security to rational, well-diversified investors.

- The example is a fire insurance policy or life insurance policy.

- These policies have a negative expected return because of commissions and insurance company profits.

- A stock having negative beta is similar to an insurance policy.

Thus, the stock C having a less expected return than T-bills makes the effect different on the stock.

4.

To determine: The market risk and the required return of a 50-50 portfolio of H and C and of H and U.

4.

Explanation of Solution

Given,

The risk-free rate is 3%.

The market return is 8.0%.

Calculate the required return on the 50-50 portfolio of H and C.

The formula to calculate the required rate of return is,

Where,

Substitute 3% for

The required rate of return is 5.025%.

Calculate the required return on the 50-50 portfolio of H and U.

The formula to calculate the required rate of return is,

Where,

Substitute 3% for

The required rate of return is 8.475%.

Working note:

Calculation of beta for 50-50 portfolio of H and C,

The value of beta is 0.405.

Calculation of beta for 50-50 portfolio of H and U,

The value of beta is 1.095.

Thus, the required return for 50-50 portfolio of H and C and for H and U is 5.025% and 8.475% respectively.

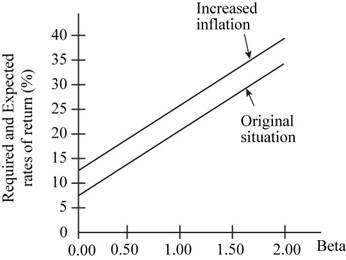

j.1.

To determine: The effect of the higher inflation on the security market line and on the returns required on high and low-risk securities.

j.1.

Answer to Problem 23IC

The graph shows the effect on the security market line:

Fig 6

Explanation of Solution

- The graph shows the effect of higher inflation on the security market line.

- The X-axis shows the value of the beta.

- The Y-axis shows the required and expected rates of return.

- The line of theoriginal situation is the ‘security market line’ in normal conditions.

- When the inflation is increased by 3% over current estimates, the ‘increased inflation line’ shows the slope of the security market line.

- The risk-free rate is 3% and the market return is 8%.

- With the increase, the risk-free rate becomes 6% and the market return becomes 11%.

- The market risk premium remains 5%.

Thus, the effect of the higher inflation is shown by the graph above and the required return will rise sharply on high-risk stocks but not much on low beta securities.

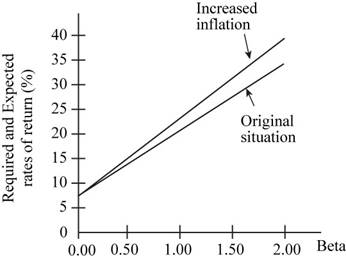

2.

To determine: The effect of the higher market risk premium on the security market line and on the returns required on high and low-risk securities.

2.

Answer to Problem 23IC

The graph shows the effect on the security market line:

Fig 7

Explanation of Solution

- The graph shows the effect of risk aversion on the security market line.

- The X-axis shows the value of the beta.

- The Y-axis shows the required and expected rates of return.

- The line of theoriginal situation is the ‘security market line’ in normal conditions.

- When the market risk premium is increased by 3% over current estimates, the ‘increased risk aversion’ line shows the slope of the security market line.

- The risk-free rate is 3% and the market return is 8%.

- With the increase, the security market line rotates upward about the Y-intercept.

- The risk-free remains constant at 3%.

- The market risk premium increases to 11%.

Thus, the effect of the increase in the market risk premium is shown in the graph above and the required return will rise sharply on high-risk stocks but not much on the low beta securities.

Want to see more full solutions like this?

Chapter 8 Solutions

Fundamentals of Financial Management, Concise Edition

- Assume that the following statements of financial position are stated and a book value. Alpha Corporation Current Assets $15,000 Current Liabilities $5,400 Net Fixed Assets 39,000 Long-Term Debt 10,100 Equity 38,500 $54,000 $54,000 Beta Corporation Current Assets $3,600 Current Liabilities $1,400 Net Fixed Assets 6,700 Long-Term Debt 2,100 Equity 6,800 $10,300 $10,300 Suppose the fair market value of Beta’s fixed assets is $9,500 rather than the $6,700 book value shown. Alpha pays $17,300 for Beta and raises the needed funds through an issue of long-term debt. Construct the post-merger statement of financial position now, assuming that the purchase method of accounting is used.arrow_forwardThe shareholders of Barley Corporation have voted in favor of a buyout offer from Wheat Corporation. Information about each firm is given here: Barley Wheat Price/earnings ratio 13.5 21 Shares outstanding 90,000 210,000 Earnings $180,000 $810,000 Barley shareholders will receive one share of Wheat stock for every three shares they hold of Barley. Required What will the EPS of Wheat be after the merger? What will be the P/E ratio if the NPV of the acquisition is 0? What must Wheat feel is the value of the synergy between these two firms? Explain how your answer can be reconciled with the decision to go ahead with the takeover?arrow_forwardBlack Oil Company is trying to decide whether to lease or buy a new computer-assisted drilling system for its extraction business. Management has already determined that acquisition of the system has a positive NPV. The system costs $9.4 million and qualifies for a 25% CCA rate. The equipment will have a $975,000 salvage value in five years. Black Oil’s tax rate is 36%, and the firm can borrow at 9%. Cape Town Company has offered to lease the drilling equipment to Black Oil for payments of $2.15 million per year. Cape Town’s policy is to require its lessees to make payments at the start of the year. Suppose it is estimated that the equipment will have no savage value at the end of the lease. What is the maximum lease payment acceptable to Black Oil now?arrow_forward

- Space Exploration Technology Corporation (Space X), is an aerospace manufacturer that sells stock engine components and tests equipment for commercial space transportation. A new customer has placed an order for eight high-bypass turbine engines, which increase fuel economy. The variable cost is $1.6 million per unit, and the credit price is $1.725 million each. Credit is extended for one period, and based on historical experience, payment for about one out of every 200 such orders is never collected. The required return is 1.8% per period. Required Assuming that this is a one-time order, should it be filled? The customer will not buy if credit is not extended. What is the break-even probability of default in part 1? Suppose that customers who don’t default become repeat customers and place the same order every period forever. Further assume that repeat customers never default. Should the order be filled? What is the break-even probability of default?arrow_forwardSouth African Airlines is contemplating leasing a high-tech tracker for its fleet of airplanes. Leasing is a very common practice with expensive, high-tech equipment. The scanner costs $6.3 million and it qualifies for a 30% CCA rate. Because of the rapid progression of technology, the high-tech tracker will be valued at $0 in 4 years. You can lease it for $1.875 million per year for four years. Assume that assets pool remains open and payments are made at the end of the year. Assuming a tax rate of 37%. You can borrow at 8% pre-tax. Should you lease or buy?arrow_forwardBlack Oil Company is trying to decide whether to lease or buy a new computer-assisted drilling system for its extraction business. Management has already determined that acquisition of the system has a positive NPV. The system costs $9.4 million and qualifies for a 25% CCA rate. The equipment will have a $975,000 salvage value in five years. Black Oil’s tax rate is 36%, and the firm can borrow at 9%. Cape Town Company has offered to lease the drilling equipment to Black Oil for payments of $2.15 million per year. Cape Town’s policy is to require its lessees to make payments at the start of the year. What is the NAL for Black Oil Company? What is the maximum lease payment that would be acceptable to the company?arrow_forward

- Iceberg Corporation currently has an all-equity capital structure. The company is considering a new structure that holds 30% debt. There are 6,500 shares outstanding and the price per share is $45 today. EBIT is expected to remain at $29,000 per year forever. The interest rate on new debt is 8%, and there are no taxes. Required Justin, a shareholder of the firm, owns 100 shares of stock. What is his cash flow under the current capital structure, assuming the company has a dividend payout rate of 100%? What will Justin’s cash flow be under the proposed capital structure of the firm? Assume he keeps all 100 of his shares. Suppose the company does convert, but Justin prefers the current all-equity capital structure. Show how he could unlever his shares of stock to recreate the original capital structure.arrow_forwardCovehead Lighthouse Corporation is considering a change in its cash-only policy. The new terms would be net one period. Based on the following information, determine if Covehead Lighthouse should proceed or not. The required rate of return is 2.5% per period. Current Policy New Policy Price per unit $73 $75 Cost per unit $38 $38 Unit sales per month 3,280 3,390arrow_forwardThe YYY and ZZZ Company are two firms whose business risk are the same but that have different dividend policies. YYY pays no dividend, whereas ZZZ has an expected dividend yield of 4%. Suppose the capital gains tax rate is zero, whereas the income tax rate is 35%. YYY has an expected earnings growth rate of 15% annually, and its stock price is expected to grow at this same rate. If the after-tax expected returns on the two stocks are equal, what is the pre-tax required return on ZZZ stock?arrow_forward

- Charlie Corporation is analyzing the possible acquisition of Delta Inc. Neither firm has debt. The forecasts of Charlie show that the purchase would increase its annual after-tax cash flow by $425,000 indefinitely. The current market value of Delta is $8.8 million. The current market value of Charlie is $22 million. The appropriate discount rate for the incremental cash flows is 8%. Charlie is trying to decide whether it should offer 35% of its stock or $12 million in cash to Delta. Required What is the synergy from the merger? What is the value of Delta to Charlie? What is the cost to Charlie of each alternative? What is the NPV of Charlie of each alternative?arrow_forwardParadox Corporation is evaluating an extra dividend verses a share repurchase. In either case, $14,500 would be spent. Current earnings are $1.65 per share, and the stock currently sells for $58 per share. There are 2,000 shares outstanding. Ignore taxes and other imperfections in answering the following questions: Required Evaluate the two alternatives in terms of the effect on the price per share of the stock and shareholder wealth. What will be the effect on Paradox Corporation’s EPS and P/E ratio under the two different scenarios? In the real world, which of these actions would you recommend? Why?arrow_forwardThe statement of financial position, from a market value, is shown below for AAA Corporation. AAA has declared a 25% stock dividend. The stock goes ex dividend tomorrow. There are currently 13,000 shares of stock outstanding. What will the ex-dividend price be? Market Value Statement of Financial Position Cash $83,000 Debt $121,000 Fixed Assets 575,000 Equity 537,000 Total $658,000 Total $658,000arrow_forward