Videos

a.

Prepare the journal entries to record cost of goods sold under (1) specific identification method, (2) average-cost method, (3) FIFO method, and (4) LIFO method, and discuss the financial reporting differences that may arise from choosing the FIFO method over the LIFO method.

a.

Explanation of Solution

Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Rules of Debit and Credit:

Following rules are followed for debiting and crediting different accounts while they occur in business transactions:

- Debit, all increase in assets, expenses and dividends, all decrease in liabilities, revenues and stockholders’ equities.

- Credit, all increase in liabilities, revenues, and stockholders’ equities, all decrease in assets, and expenses.

Perpetual inventory system: The method or system of maintaining, recording, and adjusting the inventory perpetually throughout the year, is referred to as perpetual inventory system.

First-in-First-Out (FIFO): In this method, items purchased initially are sold first. So, the value of the ending inventory consist the recent cost for the remaining unsold items.

Last-in-First-Out (LIFO): In this method, items purchased recently are sold first. So, the value of the ending inventory consist the initial cost for the remaining unsold items.

Average Cost method: In this method, the inventories are priced at the average rate of goods available for sales.

Prepare the journal entries to record cost of goods sold under specific identification method as follows:

| Date | Account Title and Explanation | Post Ref. | Debit | Credit |

| Cost of goods sold (1) | $14,800 | |||

| Inventory | $14,800 | |||

| (To record the cost of goods sold incurred) |

Table (1)

- Cost of goods sold is an operating expense account and decreases the

stockholders’ equity account by $14,800. Therefore, debit cost of goods account with $14,800. - Inventory is an asset account, and it decreases the value of assets by $14,800. Therefore, credit inventory account with $14,800.

Working note:

Calculate the value of cost of goods sold under separate identification method

Table (2)

(1)

Prepare the journal entries to record cost of goods sold under average cost method as follows:

| Date | Account Title and Explanation | Post Ref. | Debit | Credit |

| Cost of goods sold (3) | $15,050 | |||

| Inventory | $15,050 | |||

| (To record the cost of goods sold incurred) |

Table (3)

- Cost of goods sold is an operating expense account and decreases the stockholders’ equity account by $15,050. Therefore, debit cost of goods account with $15,050.

- Inventory is an asset account, and it decreases the value of assets by $15,050. Therefore, credit inventory account with $15,050.

Working note:

Calculate average cost per unit

Calculate the value of cost of goods sold under average cost method

Table (4)

(3)

Prepare the journal entries to record cost of goods sold under FIFO method as follows:

| Date | Account Title and Explanation | Post Ref. | Debit | Credit |

| Cost of goods sold (4) | $14,600 | |||

| Inventory | $14,600 | |||

| (To record the cost of goods sold incurred) |

Table (5)

- Cost of goods sold is an operating expense account and decreases the stockholders’ equity account by $14,600. Therefore, debit cost of goods account with $14,600.

- Inventory is an asset account, and it decreases the value of assets by $14,600. Therefore, credit inventory account with $14,600.

Working note:

Calculate the value of cost of goods sold under FIFO assets

Table (6)

(4)

Prepare the journal entries to record cost of goods sold under LIFO method as follows:

| Date | Account Title and Explanation | Post Ref. | Debit | Credit |

| Cost of goods sold (5) | $15,400 | |||

| Inventory | $15,400 | |||

| (To record the cost of goods sold incurred) |

Table (7)

- Cost of goods sold is an operating expense account and decreases the stockholders’ equity account by $15,400. Therefore, debit cost of goods account with $15,400.

- Inventory is an asset account, and it decreases the value of assets by $15,400. Therefore, credit inventory account with $15,400.

Working note:

Calculate the value of cost of goods sold under LIFO assets

Table (8)

(5)

b.

Prepare the subsidiary ledger record for Company under the four inventory method valuation.

b.

Explanation of Solution

Subsidiary ledger:

Subsidiary ledger refers to the ledger that provides the detailed information of the account already recorded in the general ledger such as accounts receivable subsidiary ledger and accounts payable subsidiary ledger.

Prepare the subsidiary ledger record for Company under the four inventory method valuation as follows:

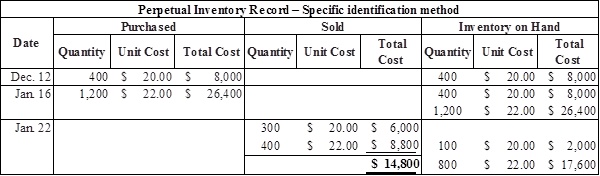

(1) Specific identification method:

| PURCHASED | SOLD | BALANCE | |||||||

| Date | Units | Unit Cost | Total | Units | Unit Cost | Cost of Goods Sold | Units | Unit Cost | Balance |

| Dec 12 | 400 | 20 | 8,000 | 400 | 20 | 8,000 | |||

| Jan 16 | 1,200 | 22 | 26,400 | 400 | 20 | ||||

| 1,200 | 22 | 34,400 | |||||||

| Jan 22 | 300 | 20 | 100 | 20 | |||||

| 400 | 22 | 14,800 | 800 | 22 | 19,600 | ||||

Table (9)

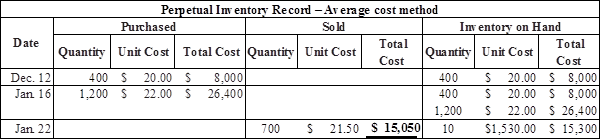

(2) Average-cost method:

| PURCHASED | SOLD | BALANCE | |||||||

| Date | Units | Cost | Total | Units | Cost | Cost of Goods Sold | Units | Cost | Balance |

| Dec 12 | 400 | 20 | 8,000 | 400 | 20.00 | 8,000 | |||

| Jan 16 | 1,200 | 22 | 26,400 | 1,600 | 21.50 | 34,400 | |||

| Jan 22 | 700 | $ 21.50 | $ 15,050 | 900 | 21.50 | 19,350 | |||

Table (10)

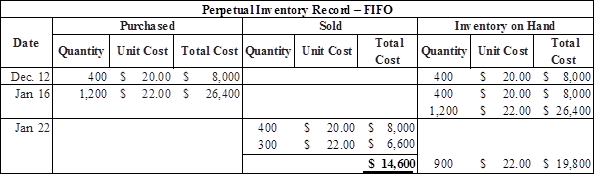

(3) First-in, first-out (FIFO) method:

| PURCHASED | SOLD | BALANCE | |||||||

| Date | Units | Unit Cost | Total | Units | Unit Cost | Cost of Goods Sold | Units | Unit Cost | Balance |

| Dec 12 | 400 | 20 | 8,000 | 400 | 20 | $ 8,000 | |||

| Jan 16 | 1,200 | 22 | 26,400 | 400 | 20 | ||||

| 1,200 | 22 | 34,400 | |||||||

| Jan 22 | 400 | 20 | |||||||

| 300 | 22 | 14,600 | 900 | 22 | 19,800 | ||||

Table (11)

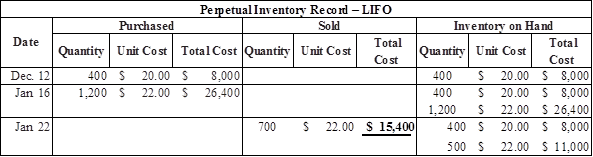

(4) Last-in, first-out (LIFO) method:

| PURCHASED | SOLD | BALANCE | |||||||

| Date | Units | Unit Cost | Total | Units | Unit Cost | Cost of Goods Sold | Units | Unit Cost | Balance |

| Dec 12 | 400 | 20 | 8,000 | 400 | 20 | 8,000 | |||

| Jan 16 | 1,200 | 22 | 26,400 | 400 | 20 | ||||

| 1,200 | 22 | 34,400 | |||||||

| Jan 22 | 700 | 22 | 15,400 | 400 | 20 | ||||

| 500 | 22 | 19,000 | |||||||

Table (12)

c.

Explain whether the

c.

Explanation of Solution

Explain whether the inventory valuation method gives lowest cost of goods sold or not, and the valuation method that gives highest cost of goods sold for the tax purposes as follows:

In this case, the cost of goods sold under FIFO and LIFO is $14,600, and $15,400 respectively. Hence, the LIFO method has highest cost of goods sold whereas the FIFO method has the lowest cost of goods sold.

The inventory method that would be preferable for financial statements is FIFO, because FIFO method would produce higher net income, lower cost of goods sold, and higher ending inventory (total assets). At the same time, the higher amount of net income produces the more income tax expense, so LIFO method is preferred for income tax reporting. When a company uses LIFO method it would produce lower amount of tax obligation and higher amount of

Want to see more full solutions like this?

Chapter 8 Solutions

Connect Online Access for Financial Accounting

- I am looking for the most effective method for solving this financial accounting problem.arrow_forwardPlease show me the valid approach to solving this financial accounting problem with correct methods.arrow_forwardI need guidance in solving this financial accounting problem using standard procedures.arrow_forward

- Can you help me find the accurate solution to this financial accounting problem using valid principles?arrow_forwardJazz Corporation owns 50 percent of the Vanderbilt Corporation stock. Vanderbilt distributed a $10,000 dividend to Jazz Corporation. Jazz Corporation's taxable income before the dividend was $100,000. What is the amount of Jazz's dividends received deduction on the dividend it received from Vanderbilt Corporation?arrow_forwardHow can I solve this financial accounting problem using the appropriate financial process?arrow_forward

- I am searching for the accurate solution to this general accounting problem with the right approach.arrow_forwardPlease provide the correct answer to this general accounting problem using valid calculations.arrow_forwardBillie Bob purchased a used camera (five-year property) for use in his sole proprietorship in the prior year. The basis of the camera was $2,400. Billie Bob used the camera in his business 60 percent of the time during the first year. During the second year, Billie Bob used the camera 40 percent for business use. Calculate Billie Bob’s depreciation deduction during the second year, assuming the sole proprietorship had a loss during the year. (Billie Bob did not place the asset in service in the last quarter.arrow_forward

- According to the income tax of Jamaica, a person is a resident if he (a) lives in the country, (b) resides in the country for not more than 183 days, (c) lives in a country 183 days or longer in any one year, or (d) lives in a country for 3 consecutive months in any one year.arrow_forwardHiarrow_forwardI need help with accountingarrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education