The effects of tax on

Concept Introduction:

Tax:

Tax is a compulsory levy on the citizens by the government.

Demand:

Demand is a quantity of a commodity that a consumer is willing to purchase at a particular

Supply:

Supply is the quantity of a commodity that a producer is willing to sell at a particular price in a given period of time.

It is the amount of goods and services a particular amount of money can purchase. It is basically the purchasing power of money.

Explanation of Solution

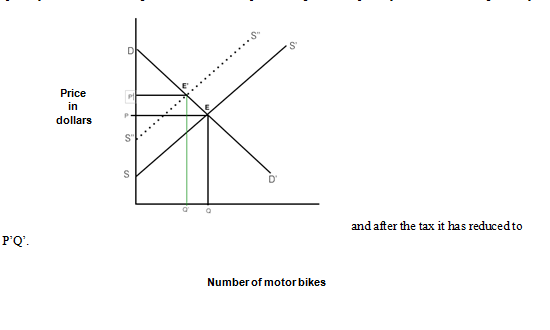

Let us take the example of a motor bike. Suppose, the cost of the motor bike is $100 and the government imposes 10% tax on the sale of it. Now, for the consumer earlier it was costing $100 but now it is costing $110, thus it has become relatively expensive. In other words, the real income of the consumer has reduced. With the reduction in the real income and substitution effect, the consumer will demand less quantity, that is, the consumer will move along the demand curve towards higher price and lesser quantity. Being conscious of this, the producer will also take an action. The supply curve will shift leftward implying less supply.

Thus, the taxes reduce both demand and supply.

As we can observe in the figure, where on vertical axis we have prices and on horizontal axis we have quantity, that before the imposition of tax, the

and after the tax it has reduced to P’Q’.

and after the tax it has reduced to P’Q’.

Want to see more full solutions like this?

Chapter 7 Solutions

MICROECONOMICS IN MODULES (LOOSELEAF)

- Use a game tree to illustrate why an aircraft manufacturer may price below the current marginal cost in the short run if it has a steep learning curve. (Hint: Show that learning by doing lowers its cost in the second period.) Part 2 Assume for simplicity the game tree is illustrated in the figure to the right. Pricing below marginal cost reduces profits but gives the incumbent a cost advantage over potential rivals. What is the subgame perfect Nash equilibrium?arrow_forwardAnswerarrow_forwardM” method Given the following model, solve by the method of “M”. (see image)arrow_forward

- As indicated in the attached image, U.S. earnings for high- and low-skill workers as measured by educational attainment began diverging in the 1980s. The remaining questions in this problem set use the model for the labor market developed in class to walk through potential explanations for this trend. 1. Assume that there are just two types of workers, low- and high-skill. As a result, there are two labor markets: supply and demand for low-skill workers and supply and demand for high-skill workers. Using two carefully drawn labor-market figures, show that an increase in the demand for high skill workers can explain an increase in the relative wage of high-skill workers. 2. Using the same assumptions as in the previous question, use two carefully drawn labor-market figures to show that an increase in the supply of low-skill workers can explain an increase in the relative wage of high-skill workers.arrow_forwardPublished in 1980, the book Free to Choose discusses how economists Milton Friedman and Rose Friedman proposed a one-sided view of the benefits of a voucher system. However, there are other economists who disagree about the potential effects of a voucher system.arrow_forwardThe following diagram illustrates the demand and marginal revenue curves facing a monopoly in an industry with no economies or diseconomies of scale. In the short and long run, MC = ATC. a. Calculate the values of profit, consumer surplus, and deadweight loss, and illustrate these on the graph. b. Repeat the calculations in part a, but now assume the monopoly is able to practice perfect price discrimination.arrow_forward

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education