To calculate: The investment opportunity set of the two risky funds is to be tabulated along with the graph.

Introduction: The portfolio risk is defined as the combination of assets which carries its own risk with each investment.

The standard deviation is used to determine that in which manner the values from a data set vary from its mean value. This is calculated by the square root of the variance.

The expected return is defined as the return which is obtained on the risky asset that is expected in future.

Answer to Problem 5PS

Expected return for the portfolio = 13.39%

Standard deviation for the portfolio =

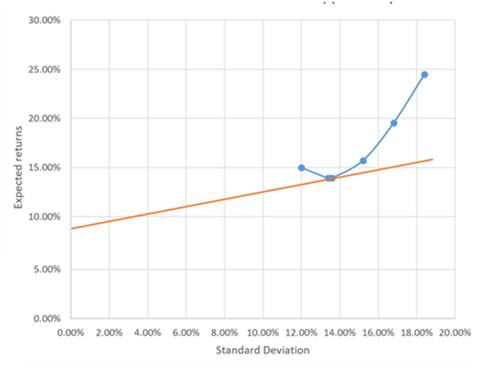

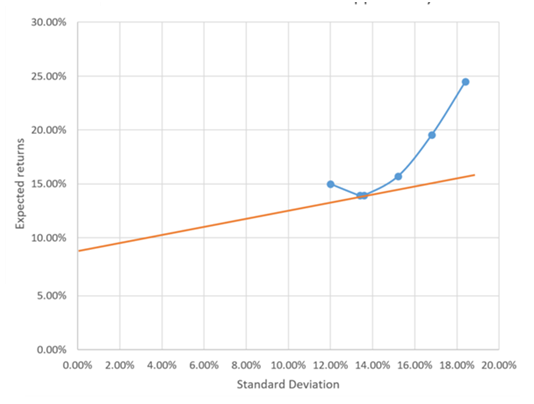

The graph is represented as −

Explanation of Solution

The following formula will be used to calculate the expected return of the portfolio for different proportions of stock and bond-

Where,

The following formula will be used to calculate the standard deviation of the portfolio for different proportions of stock and bond-

The three mutual funds are −

- Stock fund

- Long term government and corporate bond fund

- T-bill money market fund with yield 8%

The probability distribution of the risk fund is given as −

| Expected return | Standard deviation | |

| Stock fund (S) | 20% | 30% |

| Bond fund (B) | 12 | 15 |

The correlation between fund return = 0.10

The minimum variance portfolio is calculated as-

The weight of the stock fund in minimum variance portfolio is calculated as-

For bonds funds:

Put the calculated values in Equ (1) for expected return −

Put the calculated values in Equ (2) for the standard deviation-

The graph between expected return and standard deviation is called as investment opportunity set which is represented as −

Want to see more full solutions like this?

Chapter 7 Solutions

Investments

- Which of the following would hurt your credit score? Closing a long-held credit card account. Paying off student loan debt. Getting marriedarrow_forwardWhich of the following would be expected to hold its value best during a time of inflation? A certificate of deposit. A corporate bond. A house.arrow_forwardWhat is a budget? A spending plan showing sources and uses of income. A limit on spending that cannot be exceeded. The amount of money that a credit card will let youarrow_forward

- The Pan American Bottling Co. is considering the purchase of a new machine that would increase the speed of bottling and save money. The net cost of this machine is $60,000. The annual cash flows have the following projections: Year 1 ........... 2 ........... 3 ........... 4 ........... 5 ........... Cash Flow $23,000 26,000 29,000 15,000 8,000 a. If the cost of capital is 13 percent, what is the net present value of selecting a new machine? I need to see the work. I can't use Excel to solve the problem. Excel doesn't help me solve Part a.arrow_forwardPat and Chris have identical interest-bearing bank accounts that pay them $15 interest per year. Pat leaves the $15 in the account each year, while Chris takes the $15 home to a jar and never spends any of it. After five years, who has more money? Pat. Chris. They both have the same amount. Don’t knowarrow_forwardAssume a firm has earnings before depreciation and taxes of $200,000 and no depreciation. It is in a 25 percent tax bracket. a. Compute its cash flow using the following format: Earnings before depreciation and taxes _____Depreciation _____Earnings before taxes _____Taxes @ 25% _____Earnings after taxes _____Depreciation _____Cash Flow _____ b. Compute the cash flow for the company if depreciation is $200,000. Earnings before depreciation and taxes _____Depreciation _____Earnings before taxes _____Taxes @ 25% _____Earnings after taxes _____Depreciation _____Cash Flow _____ c. How large a cash flow benefit did the depreciation provide?arrow_forward

- Assume a $40,000 investment and the following cash flows for two alternatives. Year Investment X Investment Y 1 $6,000 $15,000 2 8,000 20,000 3 9,000 10,000 4 17,000 — 5 20,000 — Which of the alternatives would you select under the payback method?arrow_forwardThe Short-Line Railroad is considering a $140,000 investment in either of two companies. The cashflows are as follows:Year Electric Co. Water Works1.................. $85,000 $30,0002.................. 25,000 25,0003.................. 30,000 85,0004–10............ 10,000 10,000a. Using the payback method, what will the decision be?b. Using the Net Present Value method, which is the better project? The discount rate is 10%.arrow_forwardWhat is corporate finance explain its important?arrow_forward

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education