PRIN.OF CORPORATE FINANCE

13th Edition

ISBN: 9781260013900

Author: BREALEY

Publisher: RENT MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 7, Problem 18PS

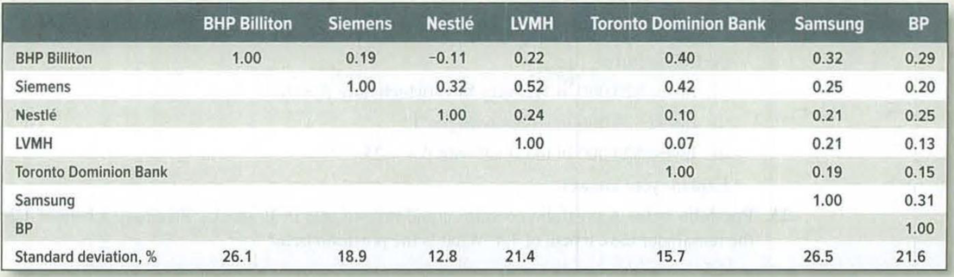

Portfolio risk Table 7.8 shows standard deviations and correlation coefficients for seven

stocks from different countries. Calculate the variance of a portfolio with equal investments

in each stock.

TABLE 7.8 Standard deviations of returns and correlation coefficients for a sample of seven stocks

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Do not answer wit incorrect values i will unhelpful!

What are the implications of missing a credit card payment in finance?

Omni Advisors, an international pension fund manager, uses the concepts of purchasing power parity (PPP) and the International Fisher Effect (IFE) to forecast spot exchange rates. Omni gathers the financial information as follows: Base price level 100 Current U.S. price level 105 Current South African price level 111 Base rand spot exchange rate $ 0.188 Current rand spot exchange rate $ 0.171 Expected annual U.S. inflation 7% Expected annual South African inflation 5% Expected U.S. one-year interest rate 10% Expected South African one-year interest rate 8% Required:

a. The current ZAR spot rate in USD that would have been forecast by PPP.Note: Do not round intermediate calculations. Round your answer to 4 decimal places.

b. Using the IFE, the expected ZAR spot rate in USD one year from now.Note: Do not round intermediate calculations. Round your answer to 4 decimal places.

c. Using PPP, the expected ZAR spot rate in USD four years from now.Note: Do not round intermediate calculations.…

Chapter 7 Solutions

PRIN.OF CORPORATE FINANCE

Ch. 7 - Rate of return The level of the Syldavia market...Ch. 7 - Real versus nominal returns The Costaguana stock...Ch. 7 - Arithmetic average and compound returns Integrated...Ch. 7 - Risk premiums Here are inflation rates and U.S....Ch. 7 - Risk Premium Suppose that in year 2030, investors...Ch. 7 - Stocks vs. bonds Each of the following statements...Ch. 7 - Expected return and standard deviation A game of...Ch. 7 - Standard deviation of returns The following table...Ch. 7 - Average returns and standard deviation During the...Ch. 7 - Prob. 10PS

Ch. 7 - Prob. 11PSCh. 7 - Diversification Here are the percentage returns on...Ch. 7 - Risk and diversification In which of the following...Ch. 7 - Prob. 14PSCh. 7 - Portfolio risk To calculate the variance of a...Ch. 7 - Portfolio risk a) How many variance terms and how...Ch. 7 - Portfolio risk Table 7.8 shows standard deviations...Ch. 7 - Portfolio risk Hyacinth Macaw invests 60% of her...Ch. 7 - Stock betas What is the beta of each of the stocks...Ch. 7 - Stock betas There are few, if any, real companies...Ch. 7 - Portfolio betas A portfolio contains equal...Ch. 7 - Portfolio betas Suppose the standard deviation of...Ch. 7 - Portfolio risk Here are some historical data on...Ch. 7 - Portfolio risk Suppose that Treasury bills offer a...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Delta Company, a U.S. MNC, is contemplating making a foreign capital expenditure in South Africa. The initial cost of the project is ZAR11,000. The annual cash flows over the five-year economic life of the project in ZAR are estimated to be 3,300, 4,300, 5,290, 6,280, and 7,250. The parent firm's cost of capital in dollars is 9,5 percent. Long-run inflation is forecasted to be 3 percent per annum in the United States and 7 percent in South Africa. The current spot foreign exchange rate is ZAR per USD = 3.75. Required:. Calculating the NPV in ZAR using the ZAR equivalent cost of capital according to the Fisher effect and then converting to USD at the current spot rate. - NPV in USD using fisher effect Converting all cash flows from ZAR to USD at purchasing power parity forecasted exchange rates and then calculating the NPV at the dollar cost of capital. - NPV in USD using PPP rates Are the two USD NPs different or the same? What is the NPV in dollars if the actual pattern of ZAR per…arrow_forwardWhat is the 50/30/20 budgeting rule in finance?arrow_forwardHow do student loans impact long-term financial health?arrow_forward

- With regard to foreign currency translation methods used by foreign MNCs, Multiple Choice a. foreign currency translation methods are generally only used by U.S. based MNCs since foreign firms have a built-in hedge by being foreign. b. are generally the same methods used by U.S.-based firms. c. are exactly the same methods used by U.S.-based firms since GAAP is GAAP. d. none of the options.arrow_forwardCray Research sold a supercomputer to the Max Planck Institute in Germany on credit and invoiced €11.60 million payable in six months. Currently, the six-month forward exchange rate is $1.18 per euro and the foreign exchange adviser for Cray Research predicts that the spot rate is likely to be $113 per euro in six months.Required: a. What is the expected gain/loss from a forward hedge?Note: A Negative value should be indicated with a minus sign. Do not round intermediate calculations. Round your final answer in whole dollars not in millions.arrow_forwardWhat is the time value of money and how is it calculated? need answer!arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:9781337514835

Author:MOYER

Publisher:CENGAGE LEARNING - CONSIGNMENT

Portfolio return, variance, standard deviation; Author: MyFinanceTeacher;https://www.youtube.com/watch?v=RWT0kx36vZE;License: Standard YouTube License, CC-BY