Principles of Accounting: Chapters 1-13

12th Edition

ISBN: 9781133593102

Author: Belverd E., Jr, Ph.d. Needles, Marian, Ph.D. Powers, Susan V. Crosson

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Videos

Question

Chapter 6S, Problem 1P

1 and 2.

To determine

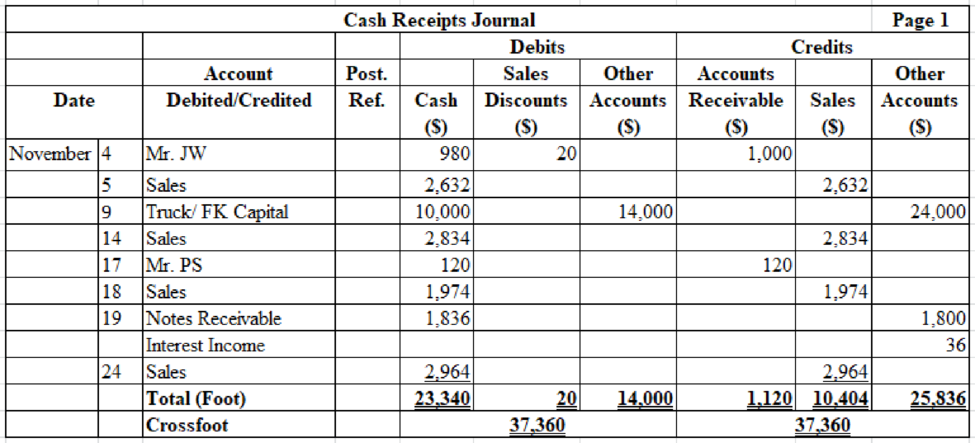

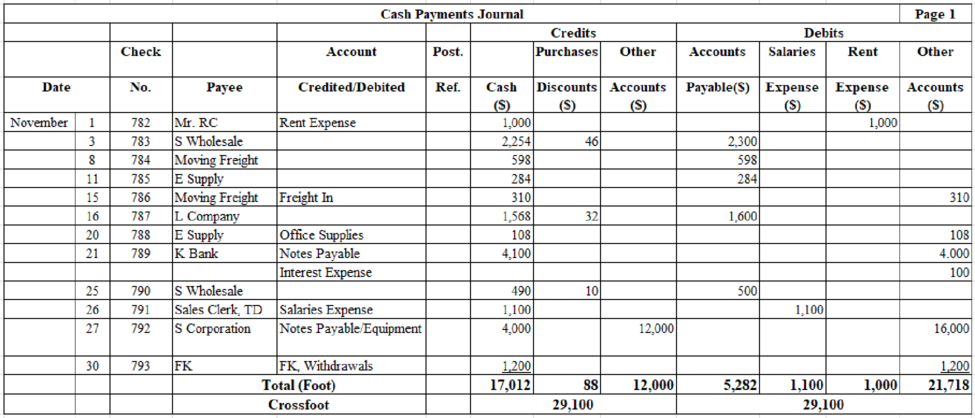

Record the given transactions in the cash receipts and cash payments journals and foot and crossfoot the journals.

1 and 2.

Expert Solution

Explanation of Solution

Record the given transactions in the cash receipts and cash payments journals.

3.

To determine

Indicate the journals from which the manager finds the total sales for the accounting period.

3.

Expert Solution

Explanation of Solution

The transaction related to Sales should be recorded in sales journal, cash receipts journal, and sales general ledger. The manager can find the total sales by adding the total sales column of sales journal and total sales column of cash receipt journal. Manager can also find the total sales by referring the sales account in the general ledger.

Want to see more full solutions like this?

Subscribe now to access step-by-step solutions to millions of textbook problems written by subject matter experts!

Students have asked these similar questions

Step by step.....?

Please help!!!! I need it bad

A company sells a product for $25 per unit. The variable cost per unit is $15, and the total fixed costs are $50,000.

a) How many units must the company sell to break even?

b) If the company wants a profit of $10,000, how many units must it sell?

Chapter 6S Solutions

Principles of Accounting: Chapters 1-13

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Don't use ai. A company has the following data: Cash: $50,000Accounts Receivable: $30,000Inventory: $60,000Current Liabilities: $70,000a) What is the company’s acid-test ratio?b) Is the company in a strong liquidity position based on this ratio?arrow_forwardQuestion 5:A company has the following data: Cash: $50,000Accounts Receivable: $30,000Inventory: $60,000Current Liabilities: $70,000a) What is the company’s acid-test ratio?b) Is the company in a strong liquidity position based on this ratio?arrow_forwardQuestion 5: Acid-Test RatioA company has the following data: Cash: $50,000Accounts Receivable: $30,000Inventory: $60,000Current Liabilities: $70,000a) What is the company’s acid-test ratio?b) Is the company in a strong liquidity position based on this ratio?arrow_forward

- Question 4: Depreciation (Straight-Line Method)A company purchases machinery for $50,000. The estimated salvage value is $5,000, and the useful life is 10 years. a) Calculate the annual depreciation expense.b) What will the book value of the machinery be after 4 years?arrow_forwardInventory Valuation (FIFO Method)A company had the following inventory transactions during the month: Beginning inventory: 100 units @ $10 eachPurchase: 200 units @ $12 eachPurchase: 150 units @ $13 eachAt the end of the month, 250 units remain in inventory. Calculate the value of the ending inventory using the FIFO method. explainarrow_forwardNeed assistance without use of ai.arrow_forward

- Depreciation (Straight-Line Method)A company purchases machinery for $50,000. The estimated salvage value is $5,000, and the useful life is 10 years. a) Calculate the annual depreciation expense.b) What will the book value of the machinery be after 4 years?arrow_forwardA company has the following data: Cash: $50,000Accounts Receivable: $30,000Inventory: $60,000Current Liabilities: $70,000a) What is the company’s acid-test ratio?b) Is the company in a strong liquidity position based on this ratio?arrow_forwardDon't want AI answerarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial Accounting

Accounting

ISBN:9781337272124

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

College Accounting (Book Only): A Career Approach

Accounting

ISBN:9781305084087

Author:Cathy J. Scott

Publisher:Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:9781947172685

Author:OpenStax

Publisher:OpenStax College

College Accounting (Book Only): A Career Approach

Accounting

ISBN:9781337280570

Author:Scott, Cathy J.

Publisher:South-Western College Pub

Excel Applications for Accounting Principles

Accounting

ISBN:9781111581565

Author:Gaylord N. Smith

Publisher:Cengage Learning

Financial Accounting

Accounting

ISBN:9781305088436

Author:Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:Cengage Learning

IAS 29 Financial Reporting in Hyperinflationary Economies: Summary 2021; Author: Silvia of CPDbox;https://www.youtube.com/watch?v=55luVuTYLY8;License: Standard Youtube License