Concept explainers

Videos

1.

Introduction:

Inventory is a record of finished goods of a company which they can sell to the customer, work in progress which can be transformed into finish goods and raw material which is a means of production. Inventory is also classified as a current asset in the

To calculate: Cost assigned to ending inventory and cost of goods sold using FIFO method.

1.

Answer to Problem 4PSB

Cost of goods available for is $249,300 and number of units available for sale is 680

Explanation of Solution

Cost of goods available for sale and number of units available for sale is as follows:

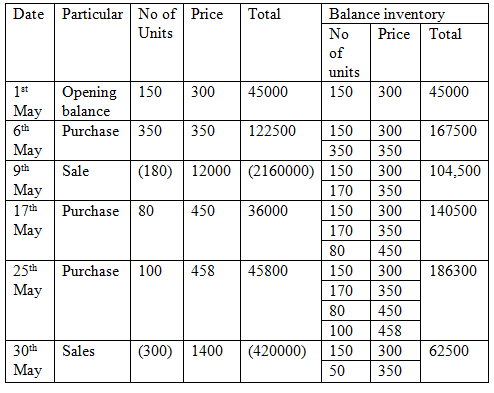

| Date | Particular | Units | Per unit cost | Total cost |

| 1st May | Opening inventory | 150 | 300 | 45000 |

| 6th May | Purchase | 350 | 350 | 122500 |

| 17th May | Purchase | 80 | 450 | 36000 |

| 25th May | purchase | 100 | 458 | 45800 |

| Total | 680 | 249,300 | ||

Thus, cost of goods available for is $249,300 and number of units available for sale is 680

Thus the cost assigned to ending inventory under FIFO method is $88800.

2.

Introduction:

Inventory is a record of finished goods of a company which they can sell to the customer, work in progress which can be transformed into finish goods and raw material which is a means of production. Inventory is also classified as a current asset in the balance sheet and it is valued by FIFO LIFO and weighted average method.

To calculate: Cost assigned to ending inventory and cost of goods sold using FIFO method.

2.

Answer to Problem 4PSB

The number of units in ending inventory is 200 units

Explanation of Solution

The number of units in closing inventory is as follows:

The number of units in ending inventory is 200 units

3.

Introduction:

Inventory is a record of finished goods of a company which they can sell to the customer, work in progress which can be transformed into finish goods and raw material which is a means of production. Inventory is also classified as a current asset in the balance sheet and it is valued by FIFO LIFO and weighted average method.

To compute: Cost assigned to ending inventory and cost of goods sold using LIFO method.

3.

Answer to Problem 4PSB

Cost assigned to ending inventory under FIFO method is $88800, under LIFO method is $62500, using weighted average method is $75600, using specific identification method is $$74,500

Explanation of Solution

- Cost assigned under FIFO method:

- LIFO method:

Thus the cost assigned to ending inventory under FIFO method is $88800.

Thus the cost assigned to ending inventory under LIFO method is $62500.

- Calculating the assigned amount of ending inventory according to weighted average method:

- Cost assigned to total inventory using specific identification method:

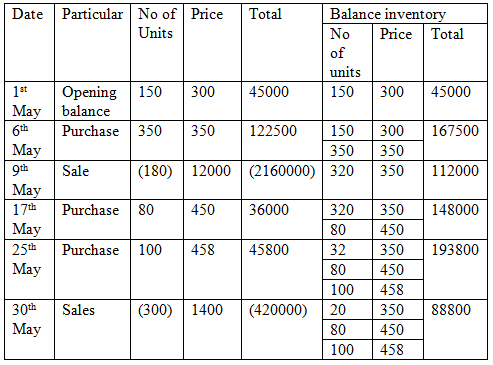

| Date | Particular | Unit | Cost per unit | Total | Balance inventory | ||

| Units | Cost per unit | Total cost | |||||

| 1st May | Opening balance | 150 | 300 | 45000 | 150 | 300 | 45000 |

| 6th may | Purchase | 350 | 350 | 122500 | 500 | 335 | 167500 |

| 9th may | Sales | 180 | 335 | 60300 | 320 | 335 | 107200 |

| 17th may | Purchase | 80 | 450 | 3600 | 400 | 358 | 143200 |

| 25th may | Purchase | 100 | 458 | 45800 | 500 | 378 | 189000 |

| 30th may | Sales | 300 | 378 | 113400 | 200 | 378 | 75600 |

Thus, cost assigned to ending inventory using weighted average method is $75600

Using specific identification method closing inventory will consist

| Particular | Units | Per unit ($) | Amount ($) |

| Opening Inventory | 70 | 300 | 21000 |

| 6th May | 50 | 350 | 17500 |

| 17th May | 80 | 450 | 36000 |

| Total | $74,500 |

Thus, cost assigned to ending inventory using specific identification method is $$74,500

4.

Introduction:

Inventory is a record of finished goods of a company which they can sell to the customer, work in progress which can be transformed into finish goods and raw material which is a means of production. Inventory is also classified as a current asset in the balance sheet and it is valued by FIFO LIFO and weighted average method.

To compute: The gross profit earn by the company is cost assigned to ending inventory for the company A using FIFO,LIFO and weighted average and specific identification.

4.

Answer to Problem 4PSB

Gross using FIFO methods is $636000 , using LIFO method is $449200, using weighted average method is $460024, and specific identification method is $461200.

Explanation of Solution

Gross profit earn by the company:

Cost of Goods sold:

For FIFO method

For LIFO methods

For weighted average method:

For specific identification:

| Particular | FIFO method | LIFO method | Weighted average method | Specific identification method |

| Total Sales | $636000 | $636000 | $636000 | $636000 |

| Cost of goods sold | $160500 | $186800 | $173700 | $174800 |

| Total | $475,500 | $449200 | $462300 | $461200 |

Thus, gross using FIFO methods is $636000 , using LIFO method is $449200, using the weighted average method is $460024, and specific identification method is $461200.

5.

Introduction:

Inventory is a record of finished goods of a company which they can sell to the customer, work in progress which can be transformed into finish goods and raw material which is a means of production. Inventory is also classified as a current asset in the balance sheet and it is valued by FIFO LIFO and weighted average method.

To compute: The gross profit earn by the company is cost assigned to ending inventory for the company A using FIFO,LIFO and weighted average and specific identification.

5.

Answer to Problem 4PSB

The manager will prefer FIFO method for costing inventory as gross profit is highest in FIFO method so using this method manager will earn more bonuses.

Explanation of Solution

FIFO method yield $475,500 gross profit which highest among other methods. So, the manager will prefer FIFO method for costing inventory as gross profit is highest in the FIFO method so using this method manager will earn more bonuses.

Want to see more full solutions like this?

Chapter 5 Solutions

Connect Access Card for Financial Accounting: Information and Decisions

- I need assistance with this financial accounting problem using valid financial procedures.arrow_forwardI need assistance with this financial accounting question using appropriate principles.arrow_forwardCan you solve this general accounting problem using appropriate accounting principles?arrow_forward

- Please give me true answer this financial accounting questionarrow_forwardAccurate Answerarrow_forwardDepartment B had 12,000 units in work in process that were 75% completed as to labor and overhead at the beginning of the period; 52,400 units of direct materials were added during the period; 48,000 units were completed during the period, and 9,500 units were 60% completed as to labor and overhead at the end of the period. All materials are added at the beginning of the process. The first-in, first-out method is used to cost inventories. The number of equivalent units of production for conversion costs for the period was ____ Units.arrow_forward

- Can you help me solve this general accounting problem with the correct methodology?arrow_forwardPlease explain the correct approach for solving this general accounting question.arrow_forwardI am looking for the correct answer to this financial accounting question with appropriate explanations.arrow_forward

- Want Answerarrow_forwardPlease help me solve this general accounting question using the right accounting principles.arrow_forwardAt the beginning of the year, Anna began a calendar-year business and placed in service the following assets during the year: Asset Date Acquired Cost Basis Computers 1/30 $ 28,000 Office desks 2/15 $ 32,000 Machinery 7/25 $ 75,000 Office building 8/13 $ 400,000 Assuming Anna does not elect §179 expensing and elects not to use bonus depreciation, answer the following questions: (Use MACRS Table 1, Table 2, Table 3, Table 4 and Table 5.) Note: Do not round intermediate calculations. b. What is Anna's year 2 cost recovery for each asset?arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub