Concept explainers

a.

The

Introduction: Consumer surplus refers to the additional profit a consumer gets due to the difference between the price of a commodity in the market and the price a consumer is ready to give for a particular commodity at a given period of time.

Producer surplus on the other hand is the additional surplus of the producers due to the difference in the price of a good at which the producer wants to the supply with the prices the consumers are ready to pay for a commodity in the market at a particular period of time.

Total surplus is the total sum of the consumer as well as the producer surplus in an economy in a given period of time. Total surplus is also referred to as the economic surplus.

Price floor refers to the minimum prices decided by the government of a country so as to minimize the change in the price of commodities.

Explanation of Solution

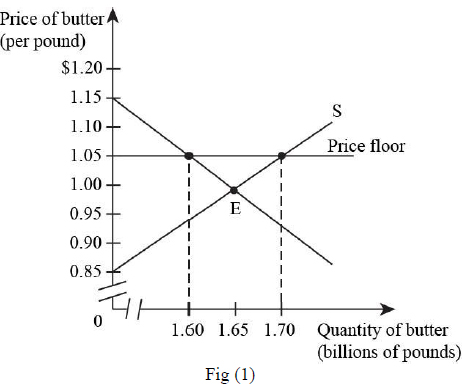

The diagram given below depicts the quantity demanded and quantity supplied of butter in billion pounds:

The consumer surplus in the absence of

Formula to calculate consumer surplus is as follows:

Substitute, $0.25 for the price above equilibrium, 0.15 for equilibrium price and $200 for the

Hence, consumer surplus is $10 billion.

Similarly, producer surplus can be calculated with the area above the supply curve but below the equilibrium prices.

Formula to calculate producer surplus is as follows:

Substitute 0.15 for the equilibrium price, 0.05 for the price below equilibrium price and $200 billion for equilibrium quantity demanded in the above formula,

Hence, producer surplus is $10 billion.

Thus, formula to calculate total surplus is as follows:

Substitute $10 billion for consumer surplus and $10 billion for producer surplus in the formula.

Hence, the total surplus is $20 billion.

b.

Consumer surplus if price floor is at $0.18 and consumer buy 140 billion pounds of milk.

Explanation of Solution

If price floor is set at $0.18 per pound, the consumer will purchase at the prices above the price floor but below the maximum price level that is $0.25 as shown in the figure 1.

The formula to calculate consumer surplus as per this explanation is as follows:

Substitute $0.25 for the maximum price, $0.18 for the floor price and 200 billion for the equilibrium quantity in the above formula,

Hence, the consumer surplus is $47 billion.

c.

The amount of producer surplus if price floor is at $0.18 per pound of milk and producers tend to sell 240 billion pounds of milk.

Explanation of Solution

With the price floor set, the producers tend to fix the sale of milk at 240 billion pounds. With this increased quantity more than the equilibrium quantity that was 1.65 billion.

Formula to calculate producer surplus is as follows:

Substitute 0.18 for floor price, 0.05 for lowest price and 240 billion for sales in the formula.

Hence, the producer surplus is $15.6 billion.

d.

The money spent by the USDA (U.S. Department of Agriculture) to buy surplus milk.

Explanation of Solution

The USDA has to buy 240 million pounds of milk.

Formula to calculate the money spends to buy 240billion pounds of milk is as follows:

Substitute, 0.18 for floor price and 240 billion for sales volume in the formula,

Hence, the amount of money spent is $43.2 billion.

e.

The total surplus in case of price floor and analyze the difference in the total surplus with price without a price floor.

Explanation of Solution

In case price floor is set by the government, the formula to calculate total surplus is as follows:

Substitute, 47 Billion for consumer surplus, $15.6 Billion for producer surplus and $43.2 Billion for the money spent in the formula,

Hence, the total surplus is $19.4 billion.

The total surplus in an economy when price floor is set by the government is less as compared to the total surplus before the advent of price floor. This is because of the reduction in both the producer as well as the consumer surplus in the economy.

Want to see more full solutions like this?

- As indicated in the attached image, U.S. earnings for high- and low-skill workers as measured by educational attainment began diverging in the 1980s. The remaining questions in this problem set use the model for the labor market developed in class to walk through potential explanations for this trend. 1. Assume that there are just two types of workers, low- and high-skill. As a result, there are two labor markets: supply and demand for low-skill workers and supply and demand for high-skill workers. Using two carefully drawn labor-market figures, show that an increase in the demand for high skill workers can explain an increase in the relative wage of high-skill workers. 2. Using the same assumptions as in the previous question, use two carefully drawn labor-market figures to show that an increase in the supply of low-skill workers can explain an increase in the relative wage of high-skill workers.arrow_forwardPublished in 1980, the book Free to Choose discusses how economists Milton Friedman and Rose Friedman proposed a one-sided view of the benefits of a voucher system. However, there are other economists who disagree about the potential effects of a voucher system.arrow_forwardThe following diagram illustrates the demand and marginal revenue curves facing a monopoly in an industry with no economies or diseconomies of scale. In the short and long run, MC = ATC. a. Calculate the values of profit, consumer surplus, and deadweight loss, and illustrate these on the graph. b. Repeat the calculations in part a, but now assume the monopoly is able to practice perfect price discrimination.arrow_forward

- how commond economies relate to principle Of Economics ?arrow_forwardCritically analyse the five (5) characteristics of Ubuntu and provide examples of how they apply to the National Health Insurance (NHI) in South Africa.arrow_forwardCritically analyse the five (5) characteristics of Ubuntu and provide examples of how they apply to the National Health Insurance (NHI) in South Africa.arrow_forward

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education