Concept explainers

Videos

Sales-related transactions using perpetual inventory system

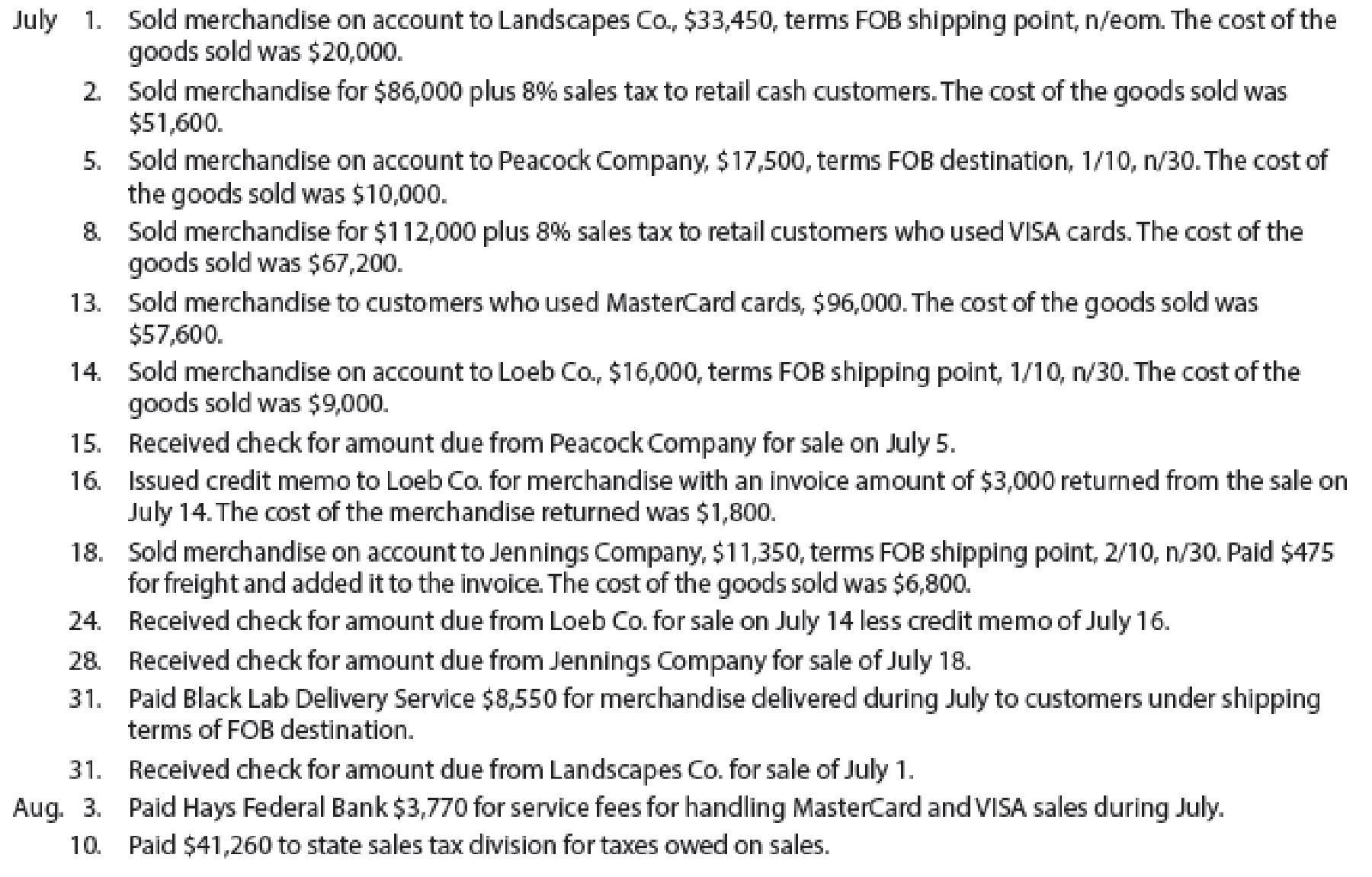

The following selected transactions were completed by Green Lawn Supplies Co., which sells irrigation supplies primarily to other businesses and occasionally to retail customers:

Instructions

Record the sale transactions of the company.

Explanation of Solution

Sales is an activity of selling the inventory of a business.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 1 | Accounts receivable | 33,450 | |

| Sales Revenue | 33,450 | ||

| (To record the sale of inventory on account) |

Table (1)

- • Accounts Receivable is an asset and it is increased by $33,450. Therefore, debit accounts receivable with $33,450.

- • Sales revenue is revenue and it increases the value of equity by $33,450. Therefore, credit sales revenue with $33,450.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 1 | Cost of Sold | 20,000 | |

| Inventory | 20,000 | ||

| (To record the cost of goods sold) |

Table (2)

- • Cost of sold is an expense account and it decreases the value of equity by $20,000. Therefore, debit cost of sold account with $20,000.

- • Inventory is an asset and it is decreased by $20,000. Therefore, credit inventory account with $20,000.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 2 | Cash | 92,880 (2) | |

| Sales Revenue | 86,000 | ||

| Sales Tax Payable | 6,880 (1) | ||

| (To record the sale of inventory for cash) |

Table (3)

Working Note (1):

Calculate the amount of sales tax payable.

Sales revenue = $86,000

Sales tax percentage = 8%

Working Note (2):

Calculate the amount of cash received.

Sales revenue = $86,000

Sales tax payable = $6,880 (1)

- • Cash is an asset and it is increased by $92,880. Therefore, debit cash account with $92,880.

- • Sales revenue is revenue and it increases the value of equity by $86,000. Therefore, credit sales revenue with $86,000.

- • Sales tax payable is a liability and it is increased by $6,880. Therefore, credit sales tax payable account with $6,880.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 2 | Cost of Sold | 51,600 | |

| Inventory | 51,600 | ||

| (To record the cost of goods sold) |

Table (4)

- • Cost of sold is an expense account and it decreases the value of equity by $51,600. Therefore, debit cost of sold account with $51,600.

- • Inventory is an asset and it is decreased by $51,600. Therefore, credit inventory account with $51,600.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 5 | Accounts receivable | 17,325 (3) | |

| Sales Revenue | 17,325 | ||

| (To record the sale of inventory on account) |

Table (5)

Working Note (3):

Calculate the amount of accounts receivable.

Sales = $17,500

Discount percentage = 1%

- • Accounts Receivable is an asset and it is increased by $17,325. Therefore, debit accounts receivable with $17,325.

- • Sales revenue is revenue and it increases the value of equity by $17,325. Therefore, credit sales revenue with $17,325.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 5 | Cost of Sold | 10,000 | |

| Inventory | 10,000 | ||

| (To record the cost of goods sold) |

Table (6)

- • Cost of sold is an expense account and it decreases the value of equity by $10,000. Therefore, debit cost of sold account with $10,000.

- • Inventory is an asset and it is decreased by $10,000. Therefore, credit inventory account with $10,000.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 8 | Cash | 120,960 (5) | |

| Sales Revenue | 112,000 | ||

| Sales Tax Payable | 8,960 (4) | ||

| (To record the sale of inventory for cash) |

Table (7)

Working Note (4):

Calculate the amount of sales tax payable.

Sales revenue = $112,000

Sales tax percentage = 8%

Working note (5):

Calculate the amount of cash received.

Sales revenue = $112,000

Sales tax payable = $8,960 (4)

- • Cash is an asset and it is increased by $120,960. Therefore, debit cash account with $120,960.

- • Sales revenue is revenue and it increases the value of equity by $112,000. Therefore, credit sales revenue with $112,000.

- • Sales tax payable is a liability and it is increased by $8,960. Therefore, credit sales tax payable account with $8,960.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 8 | Cost of Sold | 67,200 | |

| Inventory | 67,200 | ||

| (To record the cost of goods sold) |

Table (8)

- • Cost of sold is an expense account and it decreases the value of equity by $67,200. Therefore, debit cost of sold account with $67,200.

- • Inventory is an asset and it is decreased by $67,200. Therefore, credit inventory account with $67,200.

Record the journal entry for the sale of inventory for cash.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 13 | Cash | 96,000 | |

| Sales Revenue | 96,000 | ||

| (To record the sale of inventory for cash) |

Table (9)

- • Cash is an asset and it is increased by $96,000. Therefore, debit cash account with $96,000.

- • Sales revenue is revenue and it increases the value of equity by $96,000. Therefore, credit sales revenue with $96,000.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 13 | Cost of Sold | 57,600 | |

| Inventory | 57,600 | ||

| (To record the cost of goods sold) |

Table (10)

- • Cost of sold is an expense account and it decreases the value of equity by $57,600. Therefore, debit cost of sold account with $57,600.

- • Inventory is an asset and it is decreased by $57,600. Therefore, credit inventory account with $57,600.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 14 | Accounts receivable | 15,840 (6) | |

| Sales Revenue | 15,840 | ||

| (To record the sale of inventory on account) |

Table (11)

Working Note (6):

Calculate the amount of accounts receivable.

Sales = $16,000

Discount percentage = 1%

- • Accounts Receivable is an asset and it is increased by $15,840. Therefore, debit accounts receivable with $15,840.

- • Sales revenue is revenue and it increases the value of equity by $15,840. Therefore, credit sales revenue with $15,840.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 14 | Cost of Sold | 9,000 | |

| Inventory | 9,000 | ||

| (To record the cost of goods sold) |

Table (12)

- • Cost of sold is an expense account and it decreases the value of equity by $9,000. Therefore, debit cost of sold account with $9,000.

- • Inventory is an asset and it is decreased by $9,000. Therefore, credit inventory account with $9,000.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 15 | Cash | 17,325 | |

| Accounts Receivable | 17,325 | ||

| (To record the receipt of cash against accounts receivables) |

Table (13)

- • Cash is an asset and it is increased by $17,325. Therefore, debit cash account with $17,325.

- • Accounts Receivable is an asset and it is increased by $17,325. Therefore, debit accounts receivable with $17,325.

Record the journal entry for sales return.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 16 | Customer Refunds Payable | 2,970 (7) | ||

| Accounts Receivable | 2,970 | |||

| (To record sales returns) |

Table (14)

Working note (7):

Calculate the amount of refund owed to the customer.

Sales return = $3,000

Discount percentage = 1%

- • Customer refunds payable is a liability account and it is decreased by $2,970. Therefore, debit customer refunds payable account with $2,970.

- • Accounts Receivable is an asset and it is decreased by $2,970. Therefore, credit account receivable with $2,970.

Record the journal entry for the return of the .

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 16 | Inventory | 1,800 | |

| Estimated Returns Inventory | 1,800 | ||

| (To record the return of the ) |

Table (15)

- • Inventory is an asset and it is increased by $1,800. Therefore, debit inventory account with $1,800.

- • Estimated retunrs inventory is an expense account and it increases the value of equity by $1,800. Therefore, credit estimated returns inventory account with $1,800.

Record the journal entry for the sale of inventory on account.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 18 | Accounts receivable | 11,123 (8) | |

| Sales Revenue | 11,123 | ||

| (To record the sale of inventory on account) |

Table (16)

Working Note (8):

Calculate the amount of accounts receivable.

Sales = $11,350

Discount percentage = 2%

- • Accounts Receivable is an asset and it is increased by $11,123. Therefore, debit accounts receivable with $11,123.

- • Sales revenue is revenue and it increases the value of equity by $11,123. Therefore, credit sales revenue with $11,123.

Record the journal entry.

| Date | Account Title and Explanation |

Post Ref. |

Debit ($) |

Credit ($) |

| July 18 | Accounts Receivable | 475 | ||

| Cash | 475 | |||

| (To record freight charges paid) |

Table (17)

- • Accounts Receivable is an asset and it is increased by $475. Therefore, debit accounts receivable with $475.

- • Cash is an asset and it is decreased by $475. Therefore, credit cash account with $475.

Record the journal entry for cost of goods sold.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 18 | Cost of Sold | 6,800 | |

| Inventory | 6,800 | ||

| (To record the cost of goods sold) |

Table (18)

- • Cost of sold is an expense account and it decreases the value of equity by $6,800. Therefore, debit cost of sold account with $6,800.

- • Inventory is an asset and it is decreased by $6,800. Therefore, credit inventory account with $6,800.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 24 | Cash | 12,870 (9) | |

| Accounts Receivable | 12,870 | ||

| (To record the receipt of cash against accounts receivables) |

Table (19)

Working note (9):

Calculate the amount of cash received.

Net accounts receivable = $15,840

Customer refunds payable = $2,970

- • Cash is an asset and it is increased by $12,870. Therefore, debit cash account with $12,870.

- • Accounts Receivable is an asset and it is increased by $12,870. Therefore, debit accounts receivable with $12,870.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 28 | Cash | 11,598 (10) | |

| Accounts Receivable | 11,598 | ||

| (To record the receipt of cash against accounts receivables) |

Table (20)

Working note (10):

Calculate the amount of cash received.

Net accounts receivable = $11,123

Freight charges = $475

- • Cash is an asset and it is increased by $11,598. Therefore, debit cash account with $11,598.

- • Accounts Receivable is an asset and it is increased by $11,598. Therefore, debit accounts receivable with $11,598.

Record the journal entry for delivery expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| July 31 | Delivery expense | 8,550 | |

| Cash | 8,550 | ||

| (To record the payment of delivery expenses) |

Table (21)

- • Delivery expense is an expense account and it decreases the value of equity by $8,550. Therefore, debit delivery expense account with $8,550.

- • Cash is an asset and it is decreased by $8,550. Therefore, credit cash account with $8,550.

Record the journal entry for the cash receipt against accounts receivable.

| Date | Accounts and Explanation |

Debit ($) | Credit ($) |

| July 31 | Cash | 33,450 | |

| Accounts Receivable | 33,450 | ||

| (To record the receipt of cash against accounts receivables) |

Table (22)

- • Cash is an asset and it is increased by $33,450. Therefore, debit cash account with $33,450.

- • Accounts Receivable is an asset and it is increased by $33,450. Therefore, debit accounts receivable with $33,450.

Record the journal entry for credit card expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| August 3 | Credit card expense | 3,770 | |

| Cash | 3,770 | ||

| (To record the payment of credit card expenses) |

Table (23)

- • Credit card expense is an expense account and it decreases the value of equity by $3,770. Therefore, debit credit card expense account with $3,770.

- • Cash is an asset and it is decreased by $3,770. Therefore, credit cash account with $3,770.

Record the journal entry for credit card expense.

| Date | Accounts and Explanation | Debit ($) | Credit ($) |

| August 10 | Sales tax payable | 41,260 | |

| Cash | 41,260 | ||

| (To record the payment of credit card expenses) |

Table (24)

- • Sales tax payable is a liability account and it is decreased by $41,260. Therefore, debit customer refunds payable account with $41,260.

- • Cash is an asset and it is decreased by $41,260. Therefore, credit cash account with $41,260

Want to see more full solutions like this?

Chapter 5 Solutions

Financial and Managerial Accounting - CengageNow

- Please don't use AI And give correct answer .arrow_forwardLouisa Pharmaceutical Company is a maker of drugs for high blood pressure and uses a process costing system. The following information pertains to the final department of Goodheart's blockbuster drug called Mintia. Beginning work-in-process (40% completed) 1,025 units Transferred-in 4,900 units Normal spoilage 445 units Abnormal spoilage 245 units Good units transferred out 4,500 units Ending work-in-process (1/3 completed) 735 units Conversion costs in beginning inventory $ 3,250 Current conversion costs $ 7,800 Louisa calculates separate costs of spoilage by computing both normal and abnormal spoiled units. Normal spoilage costs are reallocated to good units and abnormal spoilage costs are charged as a loss. The units of Mintia that are spoiled are the result of defects not discovered before inspection of finished units. Materials are added at the beginning of the process. Using the weighted-average method, answer the following question: What are the…arrow_forwardQuick answerarrow_forward

- Financial accounting questionarrow_forwardOn November 30, Sullivan Enterprises had Accounts Receivable of $145,600. During the month of December, the company received total payments of $175,000 from credit customers. The Accounts Receivable on December 31 was $98,200. What was the number of credit sales during December?arrow_forwardPaterson Manufacturing uses both standards and budgets. For the year, estimated production of Product Z is 620,000 units. The total estimated cost for materials and labor are $1,512,000 and $1,984,000, respectively. Compute the estimates for: (a) a standard cost per unit (b) a budgeted cost for total production (Round standard costs to 2 decimal places, e.g., $1.25.)arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning