Concept explainers

Videos

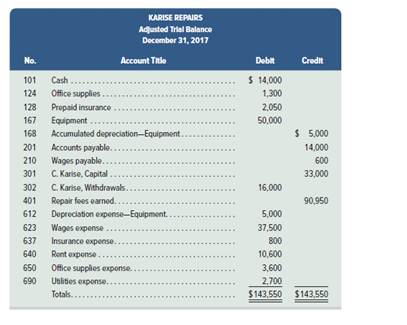

Problem 4-5A

Preparing trial balances, closing entries, and financial statements

C3 P2 P3

The adjusted

Required

a. Prepare an income statement and a statement of owner’s equity for the year 2017, and a classified

There are no owner investments in 2017.

b. Enter the adjusted trial balance in the first two columns of a six-column table. Use columns three and four for closing entry information and

the last two columns for a post-closing trial balance. Insert an Income Summary account as the last item in the trial balance.

C. Enter closing entry information in the six- column table and prepare

Check (1) Ending capital balance. $47.750 Net income. $30.750

(2) P-C trial balance totals. $67.350

Analysis Component

4. Assume for this part only that

a. None of the $8oo insurance expense had expired during the year. Instead, assume it is a prepayment of the next period’s insurance protection.

b. There are no earned and unpaid wages at the end of the year. (Hint: Reverse the $600 wages payable accrual.)

Describe the financial statement changes that would result from these two assumptions.

Want to see the full answer?

Check out a sample textbook solution

Chapter 4 Solutions

Connect Access Card for Fundamental Accounting Principles

- I am trying to find the accurate solution to this general accounting problem with the correct explanation.arrow_forwardTitan Manufacturing applies overhead cost to jobs on the basis of 85% of direct labor cost. If Job 427 shows $93,500 of manufacturing overhead applied, the direct labor cost on the job was: a. $79,475 b. $110,000 c. $120,000arrow_forwardI need help with this general accounting question using the proper accounting approach.arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning