Concept explainers

(a)

Introduction:

Journal entries of P related to its investment in S

(a)

Explanation of Solution

Journal entries

| S. no | Particulars | Debit | Credit |

| 1 | Investment in S | $ 203,000 | |

| Cash | $ 203,000 | ||

| (To record investment made in subsidiary company) | |||

| 2 | Cash | $ 20,000 | |

| Investment in S | $ 20,000 | ||

| (To record dividend declared by S) | |||

| 3 | Investment in S | $ 60,000 | |

| Income from S | $ 60,000 | ||

| (To record income generated from S) | |||

| 4 | Income from S | $ 3,000 | |

| Investment in S | $ 3,000 | ||

| (To record amortization expense) |

- Recording the initial investment in S

- Recording P’s share in S co.’s dividend

- Recording P’s share in S co.’s income

- Recording the amortization expense

| Particulars | Amount |

| Acquisition Price(a) | $ 203,000 |

| Net book value of acquisition(b) | $ 150,000 |

| $ 20,000 | |

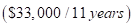

| Fair value adjustment in Building and equipments (a-b-c) | $ 33,000 |

| Amortization of excess assigned to building and equipment =$33,000/11 | $ 3,000 |

| Calculation of Income of S | ||

| Sales | $ 400,000 | |

| Less: | ||

| COGS | $ 250,000 | |

| $ 15,000 | ||

| Other expenses | $ 75,000 | $ 340,000 |

| $ 60,000 |

(b)

Introduction: Journal entries is a systematic method of recording transactions as and when they occur. It is a summary of transactions divided into the debit and credit items that are recorded chronologically. It is an act of keeping and recording all the transactions occurring in the business.

Consolidation entries to prepare consolidation financial statements

(b)

Explanation of Solution

Consolidation entries

| S.no | Particulars | Debit (in $) | Credit (in$) |

| 1 | Income from subsidiary | 57,000 | |

| Dividends declared | 20,000 | ||

| Investment in S | 37,000 | ||

| (Eliminating entry for rejecting the income from subsidiary) | |||

| 2 | Common stock- S | 50,000 | |

| 100,000 | |||

Differential  | 53,000 | ||

| Investment in S | 203,000 | ||

| (Eliminating entry for rejecting the investment balance) | |||

| 3 | Building and equipment | 33,000 | |

| Goodwill | 20,000 | ||

| Differential | 53,000 | ||

| (Eliminating entry for assigning the differential) | |||

| 4 | Depreciation expense  | 3,000 | |

| | 3,000 | ||

| (To record depreciation reclassification) | |||

| 5 | Accounts payable | 16,000 | |

| Accounts receivables | 16,000 | ||

| (To record elimination entry of inter-company transactions) |

- Recording the eliminating entry for rejecting the income from subsidiary

- Recording the eliminating entry for rejecting the investment balance

- Recording the eliminating entry for assigning the differential

- Recording the eliminating entry for amortizing the differential

- Recording the eliminating entry for inter corporate receivables and payables

(c)

Introduction: A consolidated worksheet is used to prepare the consolidated financial statements of the parent company and its subsidiary. It reflects the individual values of the parent and the subsidiary and then one consolidated figure for both the entities.

Three part consolidation worksheet for 20X5

(c)

Answer to Problem 4.36P

The consolidated net income is $157,000

The consolidated retained earnings as on December 31, 20X5 is $397,000

The total consolidated assets are $1,269,000

The total consolidated liabilities and equity are $1,269,000

Explanation of Solution

| Consolidated Work paper as on December 31, 20X5 | |||||

| Particulars | P | S | Eliminations | Consolidated | |

| Income statement | Debit | Credit | |||

| Sales | $ 700,000 | $ 400,000 | $ 1,100,000 | ||

| Less: | |||||

| Cost of goods sold | $(500,000) | $(250,000) | $ (750,000) | ||

| Depreciation expense | $ (25,000) | $ (15,000) | $ 3,000 | $ (43,000) | |

| Other expenses | $ (75,000) | $ (75,000) | $ (150,000) | ||

| Income from S' | $ 57,000 | $57,000 | |||

| Net income | $ 157,000 | $ 60,000 | $ 157,000 | ||

| Statement of Retained Earnings | |||||

| Beginning balance | $ 290,000 | $ 100,000 | $100,000 | $ 290,000 | |

| Income, from above | $ 157,000 | $ 60,000 | $ 60,000 | $ 157,000 | |

| Dividends declared | $ (50,000) | $ (20,000) | $(20,000) | $ (50,000) | |

| Ending balance | $ 397,000 | $ 140,000 | $160,000 | $(20,000) | $ 397,000 |

| Assets | |||||

| Cash | $ 82,000 | $ 25,000 | $ 107,000 | ||

| Accounts Receivables | $ 50,000 | $ 55,000 | $ 16,000 | $ 89,000 | |

| Inventory | $ 170,000 | $ 100,000 | $ 270,000 | ||

| Land | $ 80,000 | $ 20,000 | $ 100,000 | ||

| Buildings and equipment | $ 500,000 | $ 150,000 | $ 33,000 | $ 683,000 | |

| Investment in S's stock | $ 240,000 | $ 37,000 | |||

| $203,000 | |||||

| Differential | $ 53,000 | $ 53,000 | |||

| Goodwill | $ 20,000 | $ 20,000 | |||

| Total assets | $1,122,000 | $ 350,000 | $ 1,269,000 | ||

| Liabilities | |||||

| Accumulated Depreciation | $ 155,000 | $ 75,000 | $ 3,000 | $ 233,000 | |

| Accounts payable | $ 70,000 | $ 35,000 | $ 16,000 | $ 89,000 | |

| Mortgages payable | $ 200,000 | $ 50,000 | $ 250,000 | ||

| Common stock: | $ 300,000 | 50,000 | $ 50,000 | $ 300,000 | |

| Retained earnings from above | $ 397,000 | $ 140,000 | $140,000 | $ 397,000 | |

| Total liabilities and equity | $1,122,000 | $ 350,000 | $ 1,269,000 | ||

Want to see more full solutions like this?

Chapter 4 Solutions

ADVANCED FIN. ACCT.(LL)-W/CONNECT

- Need your help with Questionarrow_forwardTOSHIBA ended the year with an inventory of $842,000. During the year, the firm purchased $5,467,000 of new inventory and the cost of goods sold reported on the income statement was $5,215,000. What was TOSHIBA's inventory at the beginning of the year?arrow_forwardCan you demonstrate the proper approach for solving this financial accounting question with valid techniques?arrow_forward

- Can you explain the process for solving this financial accounting problem using valid standards?arrow_forwardThe balance in the printing supplies account on September 1 was $8,750, supplies purchased during September were $2,850, and the supplies on hand at September 30 were $2,200. The amount to be used for the appropriate adjusting entry is___. a. $6,700. b. $7,500. c. $9,400. d. $6,200. Helparrow_forwardGibson Manufacturing budgets sales of $3,750,000, fixed costs of $145,800, and variable costs of $975,000. What is the contribution margin ratio for Gibson Manufacturing? Helparrow_forward

- Duo Company has a deferred tax liability at the end of Year 1 of $120 as a result of a temporary future taxable amount of $500. If, in May, Year 2, Congress increases the income tax rate from 30% to 35%, then Duo will record the change as a: a. credit to Deferred Tax Liability of $175. b. debit to Income Tax Expense of $175. c. credit to Deferred Tax Liability of $120. d. debit to Income Tax Expense of $25.arrow_forwardSolve this problemarrow_forwardCan you explain the correct approach to solve this general accounting question?arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning