Accounting, Chapters 14-26

27th Edition

ISBN: 9781337272117

Author: WARREN, Carl S.; Reeve, James M.; Duchac, Jonathan

Publisher: South-Western College Pub

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 4, Problem 4.33EX

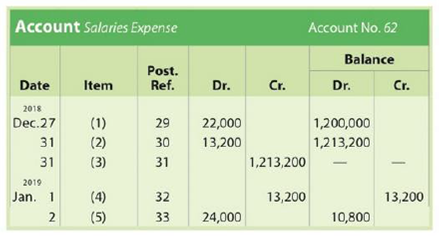

Entries posted to wages expense account

Portions of the salaries expense account of a business follow:

a. Indicate the nature of the entry (payment, adjusting, closing, reversing) from which each numbered posting was made.

b. Journalize the complete entry from which each numbered posting was made. Close revenues and expenses to J. McHenry, Capital.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

I Want Answer

What is the unit product cost under absorption costing ?

What is the estimated ending inventory?

Chapter 4 Solutions

Accounting, Chapters 14-26

Ch. 4 - Why do some accountants prepare an end-of-period...Ch. 4 - Describe the nature of the assets that compose the...Ch. 4 - Prob. 3DQCh. 4 - Prob. 4DQCh. 4 - Why are closing entries required at the end of an...Ch. 4 - What is the difference between adjusting entries...Ch. 4 - What is the purpose of the post-closing trial...Ch. 4 - Prob. 8DQCh. 4 - What is the natural business year?Ch. 4 - Prob. 10DQ

Ch. 4 - Flow of accounts into financial statements The...Ch. 4 - Flow of accounts into financial statements The...Ch. 4 - Statement of owner's equity Marcie Davies owns and...Ch. 4 - Statement of owner's equity Blake Knudson owns and...Ch. 4 - Classified balance sheet The following accounts...Ch. 4 - Classified balance sheet The following accounts...Ch. 4 - Closing entries After the accounts have been...Ch. 4 - Closing entries After the accounts have been...Ch. 4 - Accounting cycle From the following list of steps...Ch. 4 - Accounting cycle From the following list of steps...Ch. 4 - Working capital and current ratio Current assets...Ch. 4 - Working capital and current ratio Current assets...Ch. 4 - Flow of accounts into financial statements The...Ch. 4 - Classifying accounts Balances for each of the...Ch. 4 - Financial statements from the end-of-period...Ch. 4 - Financial statements from the end-of-period...Ch. 4 - Income statement The following account balances...Ch. 4 - Income statement; net loss The following revenue...Ch. 4 - Income statement FedEx Corporation had the...Ch. 4 - Statement of owners equity Apex Systems Co. offers...Ch. 4 - Statement of owners equity; net loss Selected...Ch. 4 - Classifying assets Identify each of the following...Ch. 4 - Balance sheet classification At the balance sheet...Ch. 4 - Balance sheet Optimum Weight Loss Co. offers...Ch. 4 - Balance sheet List the errors you find in the...Ch. 4 - Identifying accounts to be closed From the list...Ch. 4 - Closing entries Prior to closing, total revenues...Ch. 4 - Closing entries with net income Assume that the...Ch. 4 - Closing entries with net loss Stylist Services Co....Ch. 4 - Identifying permanent accounts Which of the...Ch. 4 - Post-closing trial balance An accountant prepared...Ch. 4 - Steps in the accounting cycle Rearrange the...Ch. 4 - Working capital and current ratio The following...Ch. 4 - Prob. 4.22EXCh. 4 - Completing an end-of-period spreadsheet List (a)...Ch. 4 - Adjustment data on an end-of-period spreadsheet...Ch. 4 - Completing an end-of-period spreadsheet Alert...Ch. 4 - Prob. 4.26EXCh. 4 - Adjusting entries from an end-of-period...Ch. 4 - Closing entries from an end-of-period spreadsheet...Ch. 4 - Reversing entry The following adjusting entry for...Ch. 4 - Adjusting and reversing entries On the basis of...Ch. 4 - Adjusting and reversing entries On the basis of...Ch. 4 - Entries posted to wages expense account Portions...Ch. 4 - Entries posted to wages expense account Portions...Ch. 4 - Financial statements and closing entries Beacon...Ch. 4 - Financial statements and closing entries Finders...Ch. 4 - T accounts, adjusting entries, financial...Ch. 4 - Ledger accounts, adjusting entries, financial...Ch. 4 - Complete accounting cycle For the past several...Ch. 4 - Financial statements and closing entries Last...Ch. 4 - Financial statements and closing entries The...Ch. 4 - T accounts, adjusting entries, financial...Ch. 4 - Ledger accounts, adjusting entries, financial...Ch. 4 - Complete accounting cycle For the past several...Ch. 4 - The unadjusted trial balance of PS Music as of...Ch. 4 - Kelly Pitney began her consulting business, Kelly...Ch. 4 - Prob. 4.1CPCh. 4 - Communication Your friend, Daniel Nat, recently...Ch. 4 - Financial statements The following is an excerpt...Ch. 4 - Financial statements Assume that you recently...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Please explain the correct approach for solving this general accounting question.arrow_forwardPlease explain the correct approach for solving this general accounting question.arrow_forwardKayla Enterprises has sales of 45.8 million, total assets of 37.2 million, and total debt of $12.7 million. If the profit margin is 9 percent, what is the net income?arrow_forward

- Please explain the solution to this general accounting problem with accurate principles.arrow_forwardI am looking for the correct answer to this general accounting question with appropriate explanations.arrow_forwardPlease provide the solution to this general accounting question with accurate financial calculations.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

Financial Accounting

Accounting

ISBN:9781337272124

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Financial Accounting

Accounting

ISBN:9781305088436

Author:Carl Warren, Jim Reeve, Jonathan Duchac

Publisher:Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:9781947172685

Author:OpenStax

Publisher:OpenStax College

College Accounting (Book Only): A Career Approach

Accounting

ISBN:9781305084087

Author:Cathy J. Scott

Publisher:Cengage Learning

College Accounting (Book Only): A Career Approach

Accounting

ISBN:9781337280570

Author:Scott, Cathy J.

Publisher:South-Western College Pub

The accounting cycle; Author: Alanis Business academy;https://www.youtube.com/watch?v=XTspj8CtzPk;License: Standard YouTube License, CC-BY