Concept explainers

Videos

Activity-based and department rate product costing and product cost distortions

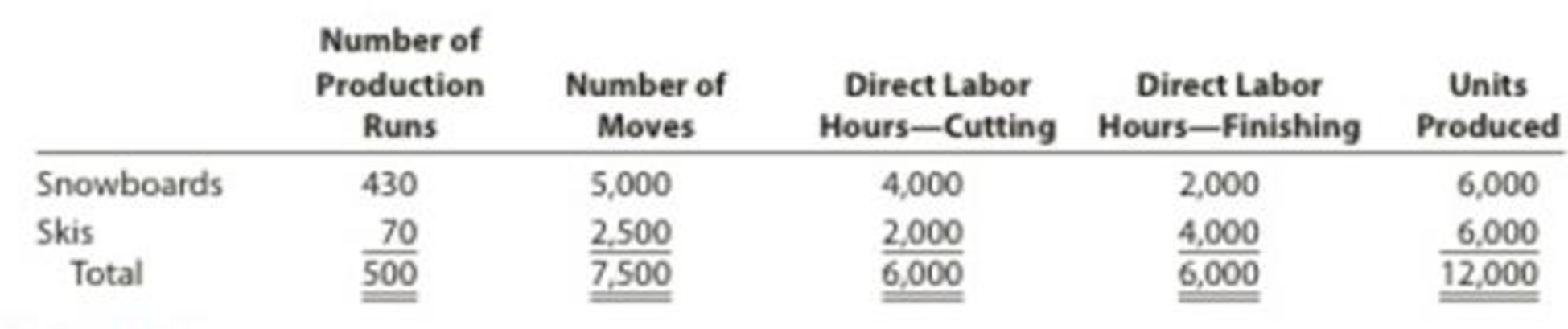

Black and Blue Sports Inc. manufactures two products: snowboards and skis. The factory

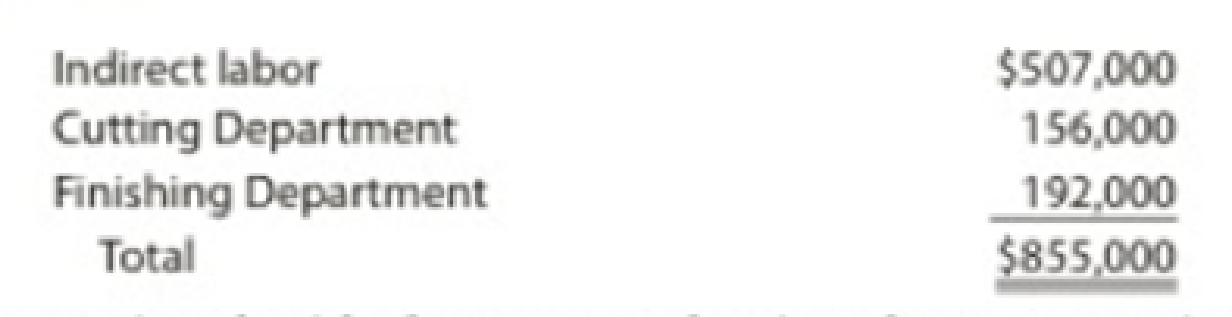

The activity base associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows:

Instructions

Determine the factory overhead rates under the multiple production department rate method. Assume that indirect labor is associated with the production departments, so that the total factory overhead is $315,000 and $540,000 for the Cutting and Finishing departments, respectively.

Determine the total and per-unit

Determine the activity rates, assuming that the indirect labor is associated with activities rather than with the production departments.

Determine the total and per-unit cost assigned to each product under activity-based costing.

Explain the difference in the per-unit overhead allocated to each product under the multiple production department factory overhead rate and activity-based costing methods.

1.

Compute the multiple production department overhead rates for both departments.

Explanation of Solution

Multiple production department factory overhead rates: This allocation method identifies different departments in the process of production. The factory overheads are allocated to products based on the overhead rate for each of the production departments.

Formula to compute multiple production department overhead rates:

Activity-based costing (ABC) method: The costing method which allocates overheads to the products based on factory overhead rate for each activity or cost object, according to the cost pooled for the cost drivers (allocation base).

Formula to compute activity-based overhead rate:

Compute multiple production department overhead rate for cutting department.

Compute multiple production department overhead rate for finishing department.

2.

Compute the factory overhead allocated to total and per unit of each product.

Explanation of Solution

Compute total factory overhead and per unit overhead allocated for snowboards.

| Production Department | Multiple Production Department Overhead Rate | × | Total Number of Budgeted DLH | = | Factory Overhead |

| Cutting | $52.50 per DLH | × | 4,000 DLH | = | $210,000 |

| Finishing | $90 per DLH | × | 2,000 DLH | = | 180,000 |

| Total factory overhead costs allocated for snowboards | $390,000 | ||||

| Number of units of snowboards | ÷ 6,000 units | ||||

| Factory overhead cost per unit of snowboard | $65.00 | ||||

Table (1)

Note: Refer to part (A) for value and computation of multiple production department overhead rate.

Compute total factory overhead and per unit overhead allocated for skis.

| Production Department | Multiple Production Department Overhead Rate | × | Total Number of Budgeted DLH | = | Factory Overhead |

| Cutting | $52.50 per DLH | × | 2,000 DLH | = | $105,000 |

| Finishing | $90 per DLH | × | 4,000 DLH | = | 360,000 |

| Total factory overhead costs allocated for skis | $465,000 | ||||

| Number of units of skis | ÷ 6,000 units | ||||

| Factory overhead cost per unit of ski | $77.50 | ||||

Table (2)

Note: Refer to part (A) for value and computation of multiple production department overhead rate.

3.

Calculate the activity-based overhead rate for each of the given activities

Explanation of Solution

Compute activity-based overhead rates.

| Computation of Activity-Based Overhead Rates | |||||

| Activity | Activity Cost | ÷ | Total Activity-Base Usage | = | Activity-Based Overhead Rates |

| Production control | $237,000 | ÷ | 500 production runs | = | $474 per run |

| Materials handling | 270,000 | ÷ | 7,500 moves | = | $36 per move |

| Cutting | 156,000 | ÷ | 6,000 DLH | = | $26 per DLH |

| Finishing | 192,000 | ÷ | 6,000 DLH | = | $32 per DLH |

Table (3)

4.

Calculate the activity-cost per unit of the products

Explanation of Solution

Compute activity cost allocated per unit of snowboards.

| Activity | Activity-Based Overhead Rates | × | Actual Use of Activity-Base (Cost Driver) | = | Activity Cost Allocated |

| Production control | $474 per run | × | 430 runs | = | $203,820 |

| Materials handling | 36 per move | × | 5,000 moves | = | 180,000 |

| Cutting | 26 per DLH | × | 4,000 DLH | = | 104,000 |

| Finishing | 32 per DLH | × | 2,000 DLH | = | 64,000 |

| Total activity costs allocated to snowboards | $551,820 | ||||

| Number of units of snowboard | ÷ 6,000 units | ||||

| Activity-based overhead cost per unit of snowboards | $91.97 | ||||

Table (4)

Note: Refer to Table (3) for the value and computation of activity allocation rates.

Compute activity cost allocated per unit of snowboards.

| Activity | Activity-Based Overhead Rates | × | Actual Use of Activity-Base (Cost Driver) | = | Activity Cost Allocated |

| Production control | $474 per run | × | 70 runs | = | $33,180 |

| Materials handling | 36 per move | × | 2,500 moves | = | 90,000 |

| Cutting | 26 per DLH | × | 2,000 DLH | = | 52,000 |

| Finishing | 32 per DLH | × | 4,000 DLH | = | 128,000 |

| Total activity costs allocated to skis | $303,180 | ||||

| Number of units of skis | ÷ 6,000 units | ||||

| Activity-based overhead cost per unit of ski | $50.53 | ||||

Table (5)

Note: Refer to Table (3) for the value and computation of activity allocation rates.

5.

Discuss the product cost distortion due to multiple production department overhead rate

Explanation of Solution

The product cost under multiple production department overhead rate approach and ABC approach are different. The product cost is distorted in multiple production department overhead rate approach. Although the time spent for cutting and finishing for snowboards and skis is in the same ratio, but the production control department and materials handling department are not accounted for in multiple department overhead rate method.

Want to see more full solutions like this?

Chapter 4 Solutions

Managerial Accounting, Loose-leaf Version

- Expand upon it pleasearrow_forwardKrypton Supplies experienced the following financial changes during a certain period: Total liabilities increased by $27,800, Stockholders' equity increased by $10,700 By how much and in what direction must total assets have changed during the same period?arrow_forwardAnthropic Industries' variable costs are 40% of sales. The company is contemplating an advertising campaign that will cost $36,000. If sales are expected to increase by $90,000, by how much will the company's net income increase? a. $18,000 b. $24,000 c. $36,000 d. $54,000arrow_forward

- Please provide the solution to this general accounting question using proper accounting principles.arrow_forwardPlease provide the solution to this general accounting question using proper accounting principles.arrow_forwardPlease show me the valid approach to solving this financial accounting problem with correct methods.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning