Videos

a.

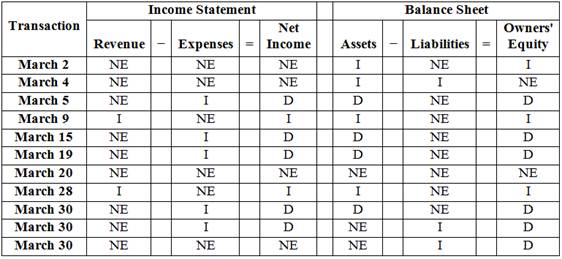

Analyze the effects that each of the given transactions will have on the following six components of the company’s financial statements for the month of March.

a.

Explanation of Solution

Income statement:

The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

This financial statement reports a company’s resources (assets) and claims of creditors (liabilities) and stockholders (stockholders’ equity) over those resources. The resources of the company are assets which include money contributed by stockholders and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and

Analyze the effects that each of the given transactions will have on the following six components of the company’s financial statements for the month of March as follows:

Figure (1)

b.

Prepare journal entries for each transaction.

b.

Explanation of Solution

Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Prepare journal entries for each transaction as follows:

| Date | Account title and Explanation | Post ref. |

Debit (in $) | Credit (in $) |

| March 2 | Cash | 80,000 | ||

| Capital stock | 80,000 | |||

| (To record the issue of the capital stock) | ||||

| March 4 | Truck | 45,000 | ||

| Cash | 15,000 | |||

| Notes Payable | 30,000 | |||

| (To record the purchase of truck) | ||||

| March 5 | Rent expense | 2,500 | ||

| Cash | 2,500 | |||

| (To record the payment made for March rent) | ||||

| March 9 | 11,300 | |||

| Service revenue | 11,300 | |||

| (To record the services provided on account) | ||||

| March 15 | Salaries expense | 7,100 | ||

| Cash | 7,100 | |||

| (To record the salary expense paid) | ||||

| March 19 | Maintenance expense | 900 | ||

| Cash | 900 | |||

| (To record the maintenance expense paid) | ||||

| March 20 | Cash | 3,800 | ||

| Accounts receivable | 3,800 | |||

| (To record the cash collected from accounts receivable) | ||||

| March 28 | Accounts receivable | 14,400 | ||

| Service revenue | 14,400 | |||

| (To record the services provided on account) | ||||

| March 30 | Salaries expense | 7,500 | ||

| Cash | 7,500 | |||

| (To record the salary expense paid) | ||||

| March 30 | Fuel expense | 830 | ||

| Accounts payable | 830 | |||

| (To record the bill received for fuel used during March) | ||||

| March 30 | Dividends | 1,200 | ||

| Dividends Payable | 1,200 | |||

| (To record the payment due for the cash dividend declared) |

Table (1)

c.

Post each transaction to the appropriate ledger accounts.

c.

Explanation of Solution

T-account:

The condensed form of a ledger is referred to as T-account. The left-hand side of this account is known as debit, and the right hand side is known as credit.

Post each transaction to the appropriate ledger accounts as follows:

| Cash | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 2 | 80,000 | 80,000 | ||

| 4 | 15,000 | 65,000 | |||

| 5 | 2,500 | 62,500 | |||

| 15 | 7,100 | 55,400 | |||

| 19 | 900 | 54,500 | |||

| 20 | 3,800 | 58,300 | |||

| 30 | 7,500 | 50,800 | |||

Table (2)

| Accounts Receivable | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 9 | 11,300 | 11,300 | ||

| 20 | 3,800 | 7,500 | |||

| 28 | 14,400 | 21,900 | |||

Table (3)

| Truck | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 4 | 45,000 | 45,000 | ||

Table (4)

| Notes Payable | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 4 | 30,000 | 30,000 | ||

Table (5)

| Accounts Payable | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 30 | 830 | 830 | ||

Table (6)

| Dividends Payable | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 30 | 1,200 | 1,200 | ||

Table (7)

| Capital Stock | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 2 | 80,000 | 80,000 | ||

Table (8)

| Dividends | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 30 | 1,200 | 1,200 | ||

Table (9)

| Service Revenue | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 9 | 11,300 | 11,300 | ||

| 28 | 14,400 | 25,700 | |||

Table (10)

| Maintenance Expense | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 19 | 900 | 900 | ||

Table (11)

| Fuel Expense | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 30 | 830 | 830 | ||

Table (12)

| Salaries Expense | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 15 | 7,100 | 7,100 | ||

| 30 | 7,500 | 14,600 | |||

Table (13)

| Rent Expense | |||||

| Date | Debit | Credit | Balance | ||

| Current Year | |||||

| March | 5 | 2,500 | 2,500 | ||

Table (14)

d.

Prepare a

d.

Explanation of Solution

Trial balance:

Trial balance is a summary of all the ledger accounts balances presented in a tabular form with two column, debit and credit. It checks the mathematical accuracy of the

Prepare a trial balance dated March 31, current year as follows:

| Deliveries T | ||

| Trial Balance | ||

| March 31, Current Year | ||

| Cash | $50,800 | |

| Accounts receivable | 21,900 | |

| Truck | 45,000 | |

| Notes payable | $30,000 | |

| Accounts payable | 830 | |

| Dividends payable | 1,200 | |

| Capital stock | 80,000 | |

| | 0 | |

| Dividends | 1,200 | |

| Service revenue | 25,700 | |

| Maintenance expense | 900 | |

| Fuel expense | 830 | |

| Salaries expense | 14,600 | |

| Rent expense | 2,500 | |

| $137,730 | $137,730 | |

Table (15)

e.

Compute total assets, total liabilities, and owners’ equity and explain whether these are the figures that the company will report in its March 31 balance sheet.

e.

Explanation of Solution

Assets:

These are the resources owned and controlled by business and used to produce benefits for the company. Assets are classified on the balance sheet as current assets, non-current assets, property, plant, and equipment, and intangible assets.

Liabilities:

The claims creditors have over assets or resources of a company are referred to as liabilities. These are the debt obligations owed by company to creditors. Liabilities are classified on the balance sheet as current liabilities and long-term liabilities.

Owners’ equity:

Owner’s equity refers to the right the owner possesses over the resources of the business. Revenues and the expenses are the components of the owner’s equity.

Net income:

The bottom line of income statement which is the result of excess of earnings from operations (revenues) over the costs incurred for earning revenues (expenses) is referred to as net income.

Compute total assets, total liabilities, and owners’ equity as follows:

| Total Assets: | ||

| Cash | $50,800 | |

| Accounts receivable | 21,900 | |

| Trucks | 45,000 | |

| Total assets | $117,700 | |

| Total Liabilities: | ||

| Notes payable | $30,000 | |

| Accounts payable | 830 | |

| Dividends payable | 1,200 | |

| Total liabilities | $32,030 | |

| Total Owners' Equity: | ||

| Total assets − Total liabilities | $85,670 |

Table (16)

Explain whether these are the figures that the company will report in its March 31 balance sheet as follows:

No, these are not the figures that the company will report in its March 31 balance sheet. Adjustments will be made to the trial balance figures at the end, before preparing the financial statements of the company. The figures, after the adjustments are made, will be the figures that the company will report in its March 31 balance sheet.

Want to see more full solutions like this?

Chapter 3 Solutions

Financial & Managerial Accounting

- Please don't use AI And give correct answer .arrow_forwardLouisa Pharmaceutical Company is a maker of drugs for high blood pressure and uses a process costing system. The following information pertains to the final department of Goodheart's blockbuster drug called Mintia. Beginning work-in-process (40% completed) 1,025 units Transferred-in 4,900 units Normal spoilage 445 units Abnormal spoilage 245 units Good units transferred out 4,500 units Ending work-in-process (1/3 completed) 735 units Conversion costs in beginning inventory $ 3,250 Current conversion costs $ 7,800 Louisa calculates separate costs of spoilage by computing both normal and abnormal spoiled units. Normal spoilage costs are reallocated to good units and abnormal spoilage costs are charged as a loss. The units of Mintia that are spoiled are the result of defects not discovered before inspection of finished units. Materials are added at the beginning of the process. Using the weighted-average method, answer the following question: What are the…arrow_forwardQuick answerarrow_forward

- Financial accounting questionarrow_forwardOn November 30, Sullivan Enterprises had Accounts Receivable of $145,600. During the month of December, the company received total payments of $175,000 from credit customers. The Accounts Receivable on December 31 was $98,200. What was the number of credit sales during December?arrow_forwardPaterson Manufacturing uses both standards and budgets. For the year, estimated production of Product Z is 620,000 units. The total estimated cost for materials and labor are $1,512,000 and $1,984,000, respectively. Compute the estimates for: (a) a standard cost per unit (b) a budgeted cost for total production (Round standard costs to 2 decimal places, e.g., $1.25.)arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education