PRIN.OF CORP.FINANCE-CONNECT ACCESS

13th Edition

ISBN: 2810023360757

Author: BREALEY

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 3, Problem 1SQ

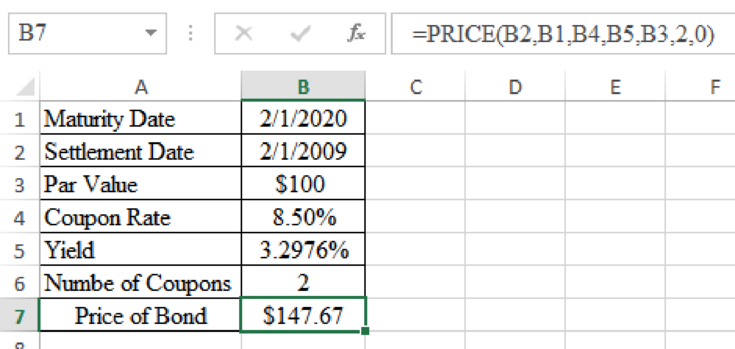

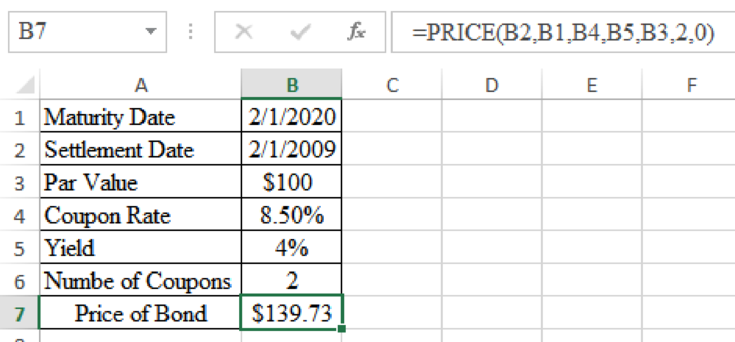

(PRICE) In February 2009, Treasury 8.5s of 2020 yielded 3.2976%. What was their price? If the yield rose to 4%, what would happen to the price?

Expert Solution

Summary Introduction

To determine: The price of bond at a yield of 3.2976%.

Answer to Problem 1SQ

The price of bond at a yield of 3.2976% is $147.67.

Explanation of Solution

Determine the price of bond at a yield of 3.2976%

Excel Spreadsheet:

Therefore the price of bond at a yield of 3.2976% is $147.67.

Expert Solution

Summary Introduction

To determine: The price of bond at a yield of 4%.

Answer to Problem 1SQ

The price of bond at a yield of 4% is $139.73.

Explanation of Solution

Determine the price of bond at a yield of 4%

Excel Spreadsheet:

Therefore the price of bond at a yield of 4% is $139.73.

Want to see more full solutions like this?

Subscribe now to access step-by-step solutions to millions of textbook problems written by subject matter experts!

Students have asked these similar questions

No ai will unhelpful

What is the future value of an ordinary annuity that pays $200 per year for 5 years at an interest rate of 5% compounded annually?

A) $1,000B) $1,052.63C) $1,105.13D) $1,215.51

step by step sopev

No Ai will give unhelp

What is the future value of an ordinary annuity that pays $200 per year for 5 years at an interest rate of 5% compounded annually?

A) $1,000B) $1,052.63C) $1,105.13D) $1,215.51

no ai ..,???10. *Calculating Expected Return*: A stock has a 50% chance of returning 15% and a 50% chance of returning 5%. What is the expected return on investment?

Chapter 3 Solutions

PRIN.OF CORP.FINANCE-CONNECT ACCESS

Ch. 3 - (PRICE) In February 2009, Treasury 8.5s of 2020...Ch. 3 - (YLD) On the same day, Treasury 3.5s of 2018 were...Ch. 3 - (DURATION) What was the duration of the Treasury...Ch. 3 - (MDURATION) What was the modified duration of the...Ch. 3 - Bond prices and yields A 10-year bond is issued...Ch. 3 - Bond prices and yields The following statements...Ch. 3 - Bond prices and yields Construct some simple...Ch. 3 - Bond prices and yields A 10-year German government...Ch. 3 - Bond prices and yields A 10-year German government...Ch. 3 - Bond prices and yields A 10-year U.S. Treasury...

Ch. 3 - Bond returns If a bonds yield to maturity does not...Ch. 3 - Bond returns a. An 8%, five-year bond yields 6%....Ch. 3 - Prob. 10PSCh. 3 - Duration True or false? Explain. a....Ch. 3 - Duration Here are the prices of three bonds with...Ch. 3 - Duration Calculate the durations and volatilities...Ch. 3 - Prob. 14PSCh. 3 - Duration Find the spreadsheet for Table 3.4 in...Ch. 3 - Prob. 16PSCh. 3 - Spot interest rates and yields Which comes first...Ch. 3 - Prob. 18PSCh. 3 - Spot interest rates and yields Look again at Table...Ch. 3 - Prob. 20PSCh. 3 - Spot interest rates and yields Assume annual...Ch. 3 - Spot interest rates and yields A 6% six-year bond...Ch. 3 - Spot interest rates and yields Is the yield on...Ch. 3 - Prob. 24PSCh. 3 - Measuring term structure The following table shows...Ch. 3 - Term-structure theories The one-year spot interest...Ch. 3 - Term-structure theories Look again at the spot...Ch. 3 - Real interest rates The two-year interest rate is...Ch. 3 - Prob. 30PSCh. 3 - Bond ratings A bonds credit rating provides a...Ch. 3 - Prob. 32PSCh. 3 - Price and spot interest rates Find the arbitrage...Ch. 3 - Prob. 34PSCh. 3 - Prices and spot interest rates What spot interest...Ch. 3 - Prices and spot interest rates Look one more time...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- What is the future value of an ordinary annuity that pays $200 per year for 5 years at an interest rate of 5% compounded annually? A) $1,000B) $1,052.63C) $1,105.13D) $1,215.51arrow_forwardA person wants to accumulate $10,000 in 4 years. How much should they invest annually if the interest rate is 6% compounded annually? A) $2,500B) $2,352.34C) $2,275.49D) $2,100arrow_forwardWhat is the present value of $2,000 to be received after 3 years, discounted at 10% per annum? A) $1,500.25B) $1,502.63C) $1,450D) $1,800 step by steparrow_forward

- No Ai ..??? 10. A company offers a 10% discount on all purchases over $100. If you buy something for $120, how much will you pay after the discount?arrow_forwardWhat is the present value of $2,000 to be received after 3 years, discounted at 10% per annum? A) $1,500.25B) $1,502.63C) $1,450D) $1,800explain.arrow_forwardNo ai..,, ?? No gpt you invest $5,000 in a mutual fund that charges a 1.5% management fee and a 0.5% administrative fee. If the fund returns 8% over a year, what is your net return?arrow_forward

- No ai..???You invest $2,000 in a certificate of deposit (CD) with a 4% annual interest rate for 2 years. How much interest will you earn?arrow_forwardA project requires an initial investment of $100,000 and generates annual cash flows of $20,000 for 5 years. If the discount rate is 10%, what is the project's net present value (NPV)? no ai help ..???arrow_forwarddear expert!!Please don't solve with incorrect values . i will give unhelpful.arrow_forward

- What is the present value of $2,000 to be received after 3 years, discounted at 10% per annum? A) $1,500.25B) $1,502.63C) $1,450D) $1,800arrow_forwardIf a business buys supplies on credit, which of the following accounts will be affected?a) Supplies and Accounts Payableb) Cash and Suppliesc) Accounts Receivable and Suppliesd) Supplies and Casharrow_forwardPlease don't solve with incorrect values . i will give unhelpful.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education

The U.S. Treasury Markets Explained | Office Hours with Gary Gensler; Author: U.S. Securities and Exchange Commission;https://www.youtube.com/watch?v=uKXZSzY2ZbA;License: Standard Youtube License