Videos

Binomial model* Over the coming year, Ragwort’s stock price will halve to $50 from its current level of $100 or it will rise to $200. The one-year interest rate is 10%.

- a. What is the delta of a one-year call option on Ragwort stock with an exercise price of $100?

- b. Use the replicating-portfolio method to value this call.

- c. In a risk-neutral world, what is the probability that Ragwort stock will rise in price?

- d. Use the risk-neutral method to check your valuation of the Ragwort option.

- e. If someone told you that in reality there is a 60% chance that Ragwort’s stock price will rise to $200, would you change your view about the value of the option? Explain.

a.

To compute: The delta of one year call option on R stock with a strike price of $100.

Explanation of Solution

The formula to calculate delta is:

The calculation of delta is as follows:

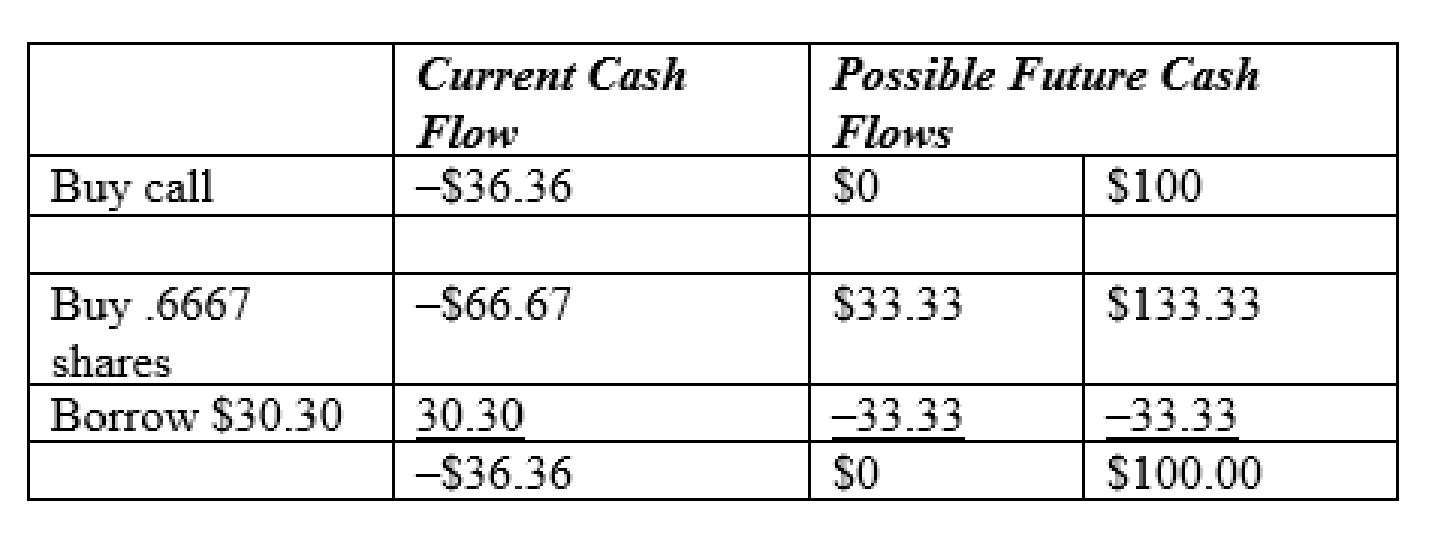

b.

To discuss: Apply the replicating portfolio technique to value this call.

Explanation of Solution

The replicating portfolio technique of valuing call is as follows.

c.

To discuss: The probability of increasing stock R price in a risk neutral world.

Explanation of Solution

The probability of increasing stock R calculated as follows:

The computation as follows:

Foot note: The probability is calculated on the basis of expected return.

d.

To compute: The value of stock R using the risk neutral method.

Explanation of Solution

The option value is calculated using the following formula:

Hence, the value of call is $36.36

e.

To discuss: Whether person X change his option regarding the value of option.

Explanation of Solution

Person X does not change his opinion regarding the value of option. The chance of price increase is most likely higher than the risk- neutral probability, but it does not aid to value the option.

Want to see more full solutions like this?

Chapter 21 Solutions

PRIN.OF CORPORATE FINANCE

Additional Business Textbook Solutions

Operations Management: Processes and Supply Chains (12th Edition) (What's New in Operations Management)

Marketing: An Introduction (13th Edition)

Intermediate Accounting (2nd Edition)

Horngren's Accounting (12th Edition)

Principles Of Taxation For Business And Investment Planning 2020 Edition

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

- What are the three interrelated areas of finance? (a) Financial markets, option and forwards (b) Banking, financial institutions and swap currency (c) Investment, Financial management and Financial market & Financial institution (d) All of abovearrow_forwardThe method that converts the amount of present cash into an amount of cash of equivalent value in future is: a.Budgeting b.Both a and b c.Discounting method d.Compounding methodarrow_forwardThe government finance which includes the principles and practices relating to the Procurement and management of funds for Central Government, and Local bodies is known as: a.Public Finance b.All of these c.Private Finance d.Business Financearrow_forward

- what is financial ratios?arrow_forwardWhich of the following is the activity which finance people are involved? (a) Investing decisions (b) Marketing decisions (c) Promotion decisions (d) Non of Abovearrow_forwardYou plan to invest $3,500 per year for 39 years into an IRA. What will the value of the IRA be after 39 years if the interest rate is 9% per year? Your answer may vary due to rounding.arrow_forward

- In finance, we refer to the market where new securities are bought and sold for the first time? (a) Money market (b) Capital market (c) Primary market (d) Secondary marketarrow_forward1: ________ is shown on a multiple-step but not on a single-step income statement. A. Credited to Inventory B. A customer utilizes a prompt payment incentive. C. Debited to the Inventory account D. Gross profitarrow_forwardwhat is corporate finance? explain it.arrow_forward

- A lorenz curve graphs the _________________ received by everyone up to a certain quintile. A. Unequal distribution over time B. Normative shares of income C. Cumulative shares of income D. Total share of incomearrow_forwardNeedhdjxjx ususs shsharrow_forwardCalculate dividends for this question i need help.arrow_forward

Pfin (with Mindtap, 1 Term Printed Access Card) (...FinanceISBN:9780357033609Author:Randall Billingsley, Lawrence J. Gitman, Michael D. JoehnkPublisher:Cengage Learning

Pfin (with Mindtap, 1 Term Printed Access Card) (...FinanceISBN:9780357033609Author:Randall Billingsley, Lawrence J. Gitman, Michael D. JoehnkPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals Of Financial Management, Concise Edi...FinanceISBN:9781337902571Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781285065137Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781305635937Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management, Concise Edi...FinanceISBN:9781305635937Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning