Concept explainers

Videos

On October 1, 2019, Jay Pryor established an interior decorating business, Pioneer Designs. During the month, Jay completed the following transactions related to the business:

Oct. 1. Jay transferred cash from a personal bank account to an account to be used for the business, $18,000.

4. Paid rent for period of October 4 to end of month, $3,000.

10. Purchased a used truck for $23,750, paying $3,750 cash and giving a note payable for the remainder.

13. Purchased equipment on account, $10,500.

14. Purchased supplies for cash, $2,100.

15. Paid annual premiums on property and casualty insurance, $3,600.

15. Received cash for job completed, $8,950.

Enter the following transactions on Page 2 of the two-column journal:

21. Paid creditor a portion of the amount owed for equipment purchased on October 13, $2,000.

24. Recorded jobs completed on account and sent invoices to customers, $14,150.

26. Received an invoice for truck expenses, to be paid in November, $700.

27. Paid utilities expense, $2,240.

27. Paid miscellaneous expenses, $1,100.

Oct. 29. Received cash from customers on account, $7,600.

30. Paid wages of employees, $4,800.

31. Withdrew cash for personal use, $3,500.

Instructions

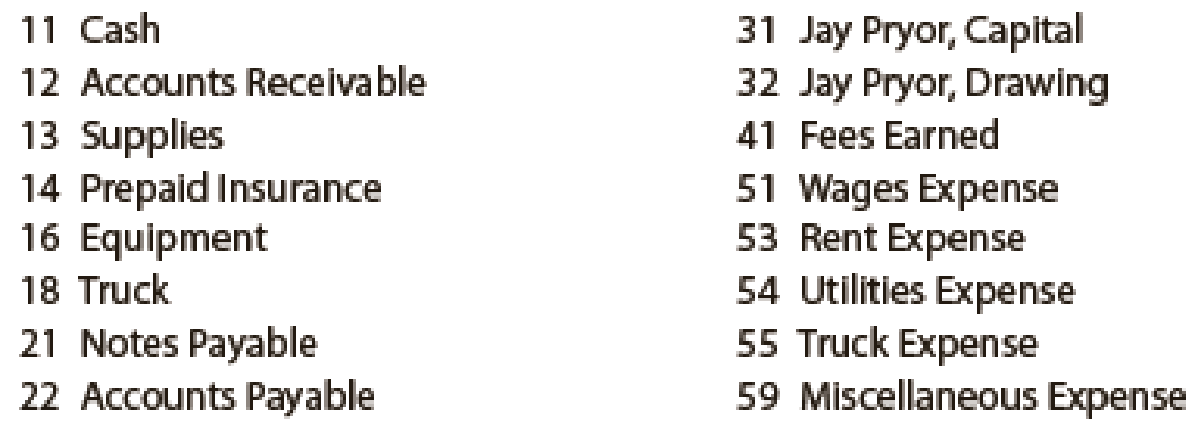

- 1. Journalize each transaction in a two-column journal beginning on Page 1, referring to the following chart of accounts in selecting the accounts to be debited and credited. (Do not insert the account numbers in the journal at this time.)

Journal entry explanations may be omitted.

- 2. Post the journal to a ledger of four-column accounts, inserting appropriate posting references as each item is posted. Extend the balances to the appropriate balance columns after each transaction is posted.

- 3. Prepare an unadjusted

trial balance for Pioneer Designs as of October 31, 2019. - 4. Determine the excess of revenues over expenses for October.

- 5.

Can you think of any reason why the amount determined in (4) might not be the net income for October?

Can you think of any reason why the amount determined in (4) might not be the net income for October?

1.

Journalize the transactions in a two column journal beginning on Page 1.

Explanation of Solution

Journal:

Journal is the book of original entry. Journal consists of the day today financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

Rules of debit and credit:

“An increase in an asset account, an increase in an expense account, a decrease in liability account, and a decrease in a revenue account should be debited.

Similarly, an increase in liability account, an increase in a revenue account and a decrease in an asset account, a decrease in an expenses account should be credited”.

Journalize each transaction in a two column journal beginning on Page 1.

| Journal Page 1 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2019 | Cash | 11 | 18,000 | ||

| October | 1 | Person JP, Capital | 31 | 18,000 | |

| (To record the transfer of cash from personal bank account to business account) | |||||

| 4 | Rent expense | 53 | 3,000 | ||

| Cash | 11 | 3,000 | |||

| (To record the payment of rent for the month of June) | |||||

| 10 | Truck | 18 | 23,750 | ||

| Cash | 11 | 3,750 | |||

| Notes payable | 21 | 20,000 | |||

| (To record the purchase of truck by cash and on account) | |||||

| 13 | Equipment | 16 | 10,500 | ||

| Accounts payable | 22 | 10,500 | |||

| (To record the purchase of equipment on account) | |||||

| 14 | Supplies | 13 | 2,100 | ||

| Cash | 11 | 2,100 | |||

| (To record the purchase of supplies) | |||||

| 15 | Prepaid insurance | 14 | 3,600 | ||

| Cash | 11 | 3,600 | |||

| (To record the payment made for insurance premiums) | |||||

| 15 | Cash | 11 | 8,950 | ||

| Fees earned | 41 | 8,950 | |||

| (To record the receipt of cash for the completed job) | |||||

Table (1)

| Journal Page 2 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2019 | 21 | Accounts payable | 22 | 2,000 | |

| October | Cash | 11 | 2,000 | ||

| (To record the payment made to creditor on account) | |||||

| 24 | Accounts receivable | 12 | 14,150 | ||

| Fees earned | 41 | 14,150 | |||

| (To record the invoices sent to customers for the jobs completed) | |||||

| 26 | Truck expense | 55 | 700 | ||

| Accounts payable | 22 | 700 | |||

| (To record the receipt of invoices for truck expenses) | |||||

| 27 | Utilities expense | 54 | 2,240 | ||

| Cash | 11 | 2,240 | |||

| (To record the payment of utilities expense) | |||||

| 27 | Miscellaneous expense | 59 | 1,100 | ||

| Cash | 11 | 1,100 | |||

| (To record the payment of miscellaneous expense) | |||||

| 29 | Cash | 11 | 7,600 | ||

| Accounts receivable | 12 | 7,600 | |||

| (To record the receipt of cash from customers on account) | |||||

| 30 | Wages expense | 51 | 4,800 | ||

| Cash | 11 | 4,800 | |||

| (To record the payment of wages expense) | |||||

| 31 | Person JP, Drawing | 32 | 3,500 | ||

| Cash | 11 | 3,500 | |||

| (To record the withdrawal of cash for personal use) | |||||

Table (2)

2.

Post the journal to a ledger of four-column accounts with appropriate post references, and the balances after each transaction is posted.

Explanation of Solution

T-account:

An account is referred to as a T-account, because the alignment of the components of the account resembles the capital letter ‘T’. An account consists of the three main components which are as follows:

- The title of the account.

- The left or debit side.

- The right or credit side.

General Ledger

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 1 | 1 | 18,000 | 18,000 | |||

| 4 | 1 | 3,000 | 15,000 | ||||

| 10 | 1 | 3,750 | 11,250 | ||||

| 14 | 1 | 2,100 | 9,150 | ||||

| 15 | 1 | 3,600 | 5,550 | ||||

| 15 | 1 | 8,950 | 14,500 | ||||

| 21 | 2 | 2,000 | 12,500 | ||||

| 27 | 2 | 2,240 | 10,260 | ||||

| 27 | 2 | 1,100 | 9,160 | ||||

| 29 | 2 | 7,600 | 16,760 | ||||

| 30 | 2 | 4,800 | 11,960 | ||||

| 31 | 2 | 3,500 | 8,460 | ||||

Table (3)

| Account: Accounts Receivable Account no. 12 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 24 | 2 | 11,900 | 14,150 | |||

| 29 | 2 | 7,600 | 6,550 | ||||

Table (4)

| Account: Supplies Account no. 13 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 14 | 1 | 2,100 | 2,100 | |||

Table (5)

| Account: Prepaid Insurance Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 15 | 1 | 3,600 | 3,600 | |||

Table (6)

| Account: Equipment Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 13 | 1 | 10,500 | 10,500 | |||

Table (7)

| Account: Truck Account no. 18 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 10 | 1 | 23,750 | 23,750 | |||

Table (8)

| Account: Notes Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 10 | 1 | 20,000 | 20,000 | |||

Table (9)

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 13 | 1 | 10,500 | – | 10,500 | ||

| 21 | 2 | 2,000 | 8,500 | ||||

| 26 | 2 | 700 | 9,200 | ||||

Table (10)

| Account: Person JP, Capital Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 1 | 1 | 18,000 | 18,000 | |||

Table (11)

| Account: Person JP, Drawing Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 31 | 2 | 3,500 | 3,500 | |||

Table (12)

| Account: Fees earned Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 15 | 1 | 8,950 | 8,950 | |||

| 24 | 2 | 14,150 | 23,100 | ||||

Table (13)

| Account: Wages expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 30 | 2 | 4,800 | 4,800 | |||

Table (14)

| Account: Rent expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 4 | 1 | 3,000 | 3,000 | |||

Table (15)

| Account: Utilities expense Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 27 | 2 | 2,240 | 2,240 | |||

Table (16)

| Account: Truck expense Account no. 55 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 26 | 2 | 700 | 700 | |||

Table (17)

| Account: Miscellaneous expense Account no. 59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| October | 27 | 2 | 1,100 | 1,100 | |||

Table (18)

3.

Prepare an unadjusted trial balance of EC Designs as of June 30, 2019.

Explanation of Solution

Unadjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Prepare an unadjusted trial balance of P Designs as of October 31, 2019 as follows:

|

P Designs Unadjusted Trial Balance October 31, 2019 | |||

| Particulars |

Account No. | Debit $ | Credit $ |

| Cash | 11 | 8,460 | |

| Accounts receivable | 12 | 6,550 | |

| Supplies | 13 | 2,100 | |

| Prepaid insurance | 14 | 3,600 | |

| Equipment | 16 | 10,500 | |

| Van | 18 | 23,750 | |

| Notes payable | 21 | 20,000 | |

| Accounts payable | 22 | 9,200 | |

| Storey K, Capital | 31 | 18,000 | |

| Storey K, Drawings | 32 | 3,500 | |

| Fees earned | 41 | 23,100 | |

| Wages expense | 51 | 4,800 | |

| Rent expense | 53 | 3,000 | |

| Utilities expense | 54 | 2,240 | |

| Van expense | 55 | 700 | |

| Miscellaneous expense | 59 | 1,100 | |

| Total | 70,300 | 70,300 | |

Table (19)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $70,300.

4.

Calculate the excess of revenues over expenses for the month of October.

Explanation of Solution

The excess of revenues over expenses for the month of October is $11,260.

Working note:

Calculate the excess of revenues over expenses.

Hence, the excess of revenues over expenses for the month of October is $11,260.

5.

Discuss the reason behind the amount determined in (4) might not be the net income for June.

Explanation of Solution

The amount determined in (4) might not be the net income for October, because adjusting entries for supplies used, insurance expired, and depreciation should be passed at the end of the accounting period in order to bring the accounts up to date.

Want to see more full solutions like this?

Chapter 2 Solutions

FINANCIAL ACCOUNTING

- Joe transferred land worth $200,000, with a tax basis of $40,000, to JH Corporation, an existing entity, for 100 shares of its stock. JH Corporation has two other shareholders, Ethan and Young, each of whom holds 100 shares. With respect to the transfer:a. Joe has no recognized gain. b. JH Corporation has a basis of $160,000 in the land.c. Joe has a basis of $200,000 in his 100 shares in JH Corporation. d. Joe has a basis of $40,000 in his 100 shares in JH Corporation. e. None of the above.arrow_forwardI need help with this general accounting problem using proper accounting guidelines.arrow_forwardI am looking for the correct answer to this general accounting problem using valid accounting standards.arrow_forward

- accounting question?arrow_forwardThree individuals form JEY Corporation with the following contributions: Joe, cash of $50,000 for 50 shares; Ethan, land worth $20,000 (basis of $11,000) for 20 shares; and Young, cattle worth $9,000 (basis of $6,000) for 9 shares and services worth $21,000 for 21 shares. a. These transfers are fully taxable and not subject to § 351. b. Young’s basis in her stock is $27,000. c. Young’s basis in her stock is $6,000. d. Ethan’s basis in his stock is $20,000. e. None of the above.arrow_forwardNonearrow_forward

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT