(a)

Consumption and saving.

(a)

Explanation of Solution

According to the life-cycle model of consumption, the consumption of an individual depends on the income earned in the entire life time of an individual.

The total life time income of the individuals can be calculated as the sum of income they earn in different periods using Equation (1) as follows:

Given that A enjoys $100,000 in three periods and F enjoys $40,000 in period1, $100,000 in period2, and $160,000 in period3, both individuals consume for 5 periods in life.

The life-time income of A can be calculated by substituting the respective values in Equation (1) as follows:

Thus, the life-time income of A is $300,000.

The life-time income of F can be calculated by substituting the respective values in Equation (1) as follows:

Thus, the life-time income of F is $300,000.

The life-time consumption of individuals can be calculated using Equation (2) as follows:

The life-time consumption of A can be calculated by substituting the respective values in Equation (2) as follows:

The life-time consumption of A is $60,000.

The life-time consumption of F can be calculated by substituting the respective values in Equation (2) as follows:

The life-time consumption of F is $60,000.

The savings can be calculated as the part of income, which is not consumed. The savings can be calculated using Equation (3) as follows:

The saving in period 1 for A can be calculated by substituting the respective value in Equation (3) as follows:

Thus, A’ savings for period 1 is $40,000.

Table 1 shows the values of savings for A and F in different periods calculated using Equations 1, 2, and 3.

Table 1

| A | F | |

| S1 | 40,000 | -20,000 |

| S2 | 40,000 | 40,000 |

| S3 | 40,000 | 100,000 |

| S4 | -60,000 | -60,000 |

| S5 | -60,000 | -60,000 |

Life-cycle theory: Life-cycle theory developed by Franco Modigliani and Richard Brumberg relates the spending and saving habits of an individual to the course of their life time.

Savings: Savings is defined as that part of income that is not consumed in the current period and is to be used for future consumption.

(b)

The wealth of individuals.

(b)

Explanation of Solution

The wealth of an individual is calculated as the accumulated saving in each period.

The wealth can be calculated using Equation (4) as follows:

The wealth of individual A in the beginning of period 2 is calculated by substituting the respective values in Equation (4) as follows:

Thus, the wealth of A in the beginning of period 2 is $40,000.

Table 2 shows the values of wealth for A and F in different periods, which are calculated using Equation 4.

Table 1

| A | F | |

| W1 | 0 | 0 |

| W2 | 40,000 | -20,000 |

| W3 | 80,000 | 20,000 |

| W4 | 120,000 | 120,000 |

| W5 | 60,000 | 60,000 |

| W6 | 0 | 0 |

It is evident from the table values that there is no wealth in period1 and period 6.

(c)

The graphical representation of consumption, income, and wealth of the individuals.

(c)

Explanation of Solution

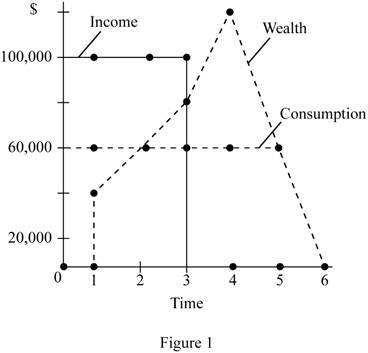

Figure 1 given below shows the consumption, income, and wealth of A.

The horizontal axis of Figure 1 measures the time period, and the vertical axis measures the consumption, income, and wealth. A enjoys a fixed income over the first 3 periods, and hence he also has a constant pattern of consumption as clearly depicted in Figure 1. A saves a part of his income and thus gradually increases his wealth during his earning years and gradually dissaves when he leads his retirement life. His pattern of consumption, income, and wealth is according to the prediction of the life-cycle model.

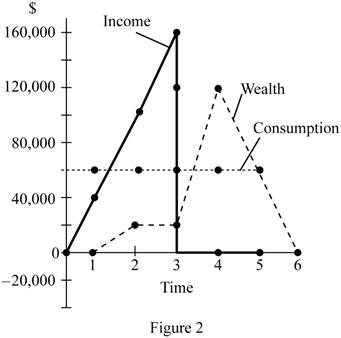

Figure 2 given below shows the consumption, income, and wealth of F.

The horizontal axis of Figure 1 measures the time period, and the vertical axis measures the consumption, income, and wealth. F increases his income gradually, and this would force him to borrow initially to enjoy a smooth consumption. When his income increases, he would accumulate wealth and then use it for his consumption in the retirement life.

Savings: Savings is defined as that part of income that is not consumed in the current period and is to be used for future consumption.

Dissaving: The act of spending more than earned in the current period or spending the past savings is known as dissaving.

(d)

The impact of borrowing.

(d)

Explanation of Solution

A has fixed income from the initial years of earning, and hence there is no need for him to borrow. Thus, A’s consumption or income will not be affected when there is a borrowing constraint. However, F depends on borrowing for his initial period. When there is a borrowing constraint, F has to spend his entire income of $40,000 in the initial period. For the later periods, he smooths his consumption by dividing the lifetime income across the remaining periods.

The life-time income of F can be calculated by substituting the respective values in Equation (1) as follows:

Thus, the life-time income of F is $260,000.

The life-time consumption of F can be calculated by substituting the respective values in Equation (2) as follows:

The life-time consumption of F is $65,000.

The saving in period 2 for F can be calculated by substituting the respective values in Equation (3) as follows:

Thus, F’s savings for period 2 is $35,000.

The wealth of individual F in the beginning of period 2 is calculated by substituting the respective values in Equation (4) as follows:

Thus, the wealth of A in the beginning of period 2 is $40,000.

Table 2 shows the values of savings and wealth F in different periods, which are calculated using Equations 3 and 4.

Table 1

| Period | F's Consumption | F's Savings | F's Wealth |

| 0 | 0 | 0 | 0 |

| 1 | 40,000 | 0 | 0 |

| 2 | 65,000 | 35,000 | 35,000 |

| 3 | 65,000 | 95,000 | 130,000 |

| 4 | 65,000 | -65,000 | 65,000 |

| 5 | 65,000 | -65,000 | 0 |

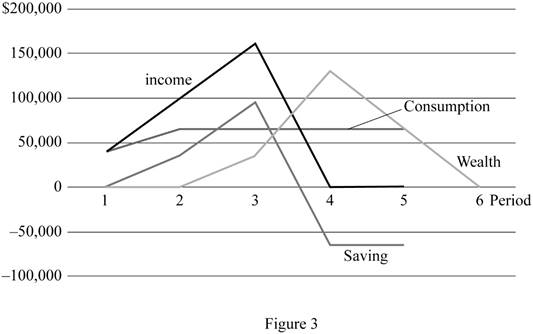

Figure 3 given below shows the consumption, income, and wealth of F.

The horizontal axis of Figure 1 measures the time period, and the vertical axis measures the consumption, income, and wealth. F increases his income gradually. However, he faces borrowing constraints, and hence he can only use his initial income for consumption. When his income increases, he would accumulate wealth, and then use it for his consumption in the retirement life.

Savings: Savings is defined as that part of income that is not consumed in the current period and is to be used for future consumption.

Dissaving: The act of spending more than earned in the current period or spending the past savings is known as dissaving.

Want to see more full solutions like this?

Chapter 19 Solutions

Macroeconomics (Cloth) (Instructor's)

- 1. We want to examine the comparative statics of the Black Scholes model. Complete the following table using the Excel model from class or another of your choice. Provide the call premium and the put premium for each scenario. Underlier Risk-free Scenario price rate Volatility Time to expiration Strike Call premium Put premium Baseline $50 5% 25% 1 year $55 Higher strike $50 5% 25% 1 year $60 Higher volatility $50 5% 40% 1 year $55 Higher risk free $50 8% 25% 1 year $55 More time $50 5% 25% 2 years $55 2. Look at the baseline scenario. a. What is the probability that the call is exercised in the baseline scenario? b. What is the probability that the put is exercised? c. Explain why the probabilities sum to 1.arrow_forwardSome people say that since inflation can be reduced in the long run without an increase in unemployment, we should reduce inflation to zero. Others believe that a steady rate of inflation at, say, 3 percent, should be our goal. What are the pros and cons of these two arguments? What, in your opinion, are good long-run goals for reducing inflation and unemployment?arrow_forwardExplain in words how investment multiplier and the interest sensitivity of aggregate demand affect the slope of the IS curve. Explain in words how and why the income and interest sensitivities of the demand for real balances affect the slope of the LM curve. According to the IS–LM model, what happens to the interest rate, income, consumption, and investment under the following circumstances?a. The central bank increases the money supply.b. The government increases government purchases.c. The government increases taxes.arrow_forward

- Suppose that a person’s wealth is $50,000 and that her yearlyincome is $60,000. Also suppose that her money demand functionis given by Md = $Y10.35 - i2Derive the demand for bonds. Suppose the interest rate increases by 10 percentage points. What is the effect on her demand for bonds?b. What are the effects of an increase in income on her demand for money and her demand for bonds? Explain in wordsarrow_forwardImagine you are a world leader and you just viewed this presentation as part of the United Nations Sustainable Development Goal Meeting. Summarize your findings https://www.youtube.com/watch?v=v7WUpgPZzpIarrow_forwardPlease draw a standard Commercial Bank Balance Sheet and briefly explain each of the main components.arrow_forward

- Please draw the Federal Reserve System’s Balance Sheet and briefly explain each of the main components.arrow_forward19. In a paragraph, no bullet, points please answer the question and follow the instructions. Give only the solution: Use the Feynman technique throughout. Assume that you’re explaining the answer to someone who doesn’t know the topic at all. How does the Federal Reserve currently get the federal funds rate where they want it to be?arrow_forward18. In a paragraph, no bullet, points please answer the question and follow the instructions. Give only the solution: Use the Feynman technique throughout. Assume that you’re explaining the answer to someone who doesn’t know the topic at all. Carefully compare and contrast fiscal policy and monetary policy.arrow_forward

- 15. In a paragraph, no bullet, points please answer the question and follow the instructions. Give only the solution: Use the Feynman technique throughout. Assume that you’re explaining the answer to someone who doesn’t know the topic at all. What are the common arguments for and against high levels of federal debt?arrow_forward17. In a paragraph, no bullet, points please answer the question and follow the instructions. Give only the solution: Use the Feynman technique throughout. Assume that you’re explaining the answer to someone who doesn’t know the topic at all. Explain the difference between present value and future value. Be sure to use and explain the mathematical formulas for both. How does one interpret these formulas?arrow_forward12. Give the solution: Use the Feynman technique throughout. Assume that you’re explaining the answer to someone who doesn’t know the topic at all. Show and carefully explain the Taylor rule and all of its components, used as a monetary policy guide.arrow_forward

Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning