a.

To discuss: The reason why stockholders are indifferent to whether a firm decreases the volatility of its cash flows.

Introduction:

Stock is a type of security in a company that denotes ownership. The company can raise the capital by issuing stocks.

a.

Explanation of Solution

The reason why stockholders are indifferent to whether a firm decreases the cash flows ‘s volatility is as follows:

The stockholder can reduce the risk of volatile cash flows by way of diversifying their portfolio at the time when the volatility in cash flows are not caused by systematic risk. Even the firm will have to pass on the hedging cost to the investors when a firm decided to hedge the risk related to the cash flows ‘s volatility.

As a result, the sophisticated investors could hedge the risks by themselves. Therefore, these investors are indifferent from those who actually do the hedging process.

b.

To discuss: The reasons for risk management may raise the corporation value.

Introduction:

Risk management is a technique used in business to evaluate the financial risks associated by it. It helps to identify certain procedures to avoid or minimize their impact in the business.

b.

Explanation of Solution

The reasons of risk management can raise the corporation value are as follows:

- The risk management permits corporation to raise their use of debt.

- Reduces the costs related with the financial distress.

- Decrease the costs and risks of borrowing by using swap approaches.

- This management technique helps to maintain the company’s optimal capital budget.

- Risk management helps to decrease the higher taxes, which result from the fluctuating earnings.

- It even initiates compensation programs to rewards managers for attaining constant earnings.

- The risk management allows the corporate to use their

comparative advantages in hedging process relative to the hedging ability of individual investors.

c.

To discuss: The meaning of option and importance characteristic of an option.

Introduction:

A type of financial security whose value is derived from the value of a particular underlying asset is termed as Derivative. This form of financial security consists of two or more parties who enter into an agreement to purchase or sell an asset at a specific price on a particular period. They are four types of derivative securities that are as follows:

- Forward contract

- Future contract

- Swap

- Option

c.

Explanation of Solution

The meaning of option and importance characteristic of an option are as follows:

Option is a contract to purchase a financial asset from one party and sell it to another party on an agreed price for a future date. There are two types of options, which are as follows:

- An option that buys an asset called call option

- An option that sells an asset called put option

The most significant characteristic of option is that it will not obligate its owner to take any action. However, it gives the owner only the right to purchase or sell assets in the market.

d.1.

To discuss: The meaning of call option.

d.1.

Explanation of Solution

The meaning of call option is as follows:

An option to purchase a particular number of shares of a security within a specific period is termed as call option. It is a derivative contract between two parties.

d.2.

To discuss: The meaning of put option.

d.2.

Explanation of Solution

The meaning of put option is as follows:

An option to sell a particular number of shares of a security within a specific period is termed as put option. It is a derivative contract between two parties.

d.3.

To discuss: The meaning of exercise price.

d.3.

Explanation of Solution

The meaning of exercise price is as follows:

Exercise price is a price wherein a call or put options can be exercised in a derivative. It is also termed as Strike price.

d.4.

To discuss: The meaning of strike price.

d.4.

Explanation of Solution

The meaning of strike price is as follows:

A price which is specified in the option contract at which point the stocks can be sold or bough is termed as strike price.

d.5.

To discuss: The meaning of option price.

d.5.

Explanation of Solution

The meaning of option price is as follow:

An amount or price of shares where the option buyer pays to the seller is termed as option price. It is the market price of an option contract.

d.6.

To discuss: The meaning of expiration date.

d.6.

Explanation of Solution

The meaning of expiration date is as follows:

The last day or date, wherein the holder of a financial security has a right to exercise the particular option is termed as expiration date. In case of a Country AM’s option, the right of the holder is exercised until the exercise date whereas in Country E’s option, the option will be exercised only at the exercise date.

d.7.

To discuss: The meaning of exercise value.

d.7.

Explanation of Solution

The meaning of exercise value is as follows:

A value of call option when it is exercised at present is termed as exercise value. The mathematical equation of exercise value is as follows:

d.8.

To discuss: The meaning of covered option.

d.8.

Explanation of Solution

The meaning of covered option is as follows:

A call option is written against the stock held in a portfolio of the investor is termed as covered option. It is financial market transaction wherein the seller of call option owns the amount of underlying assets.

d.9.

To discuss: The meaning of naked option.

d.9.

Explanation of Solution

The meaning of naked option is as follows:

An option contract that cannot comprise on the ownership of the underlying assets or security by the way of buying or selling party is termed as naked option. It is just the reverse of a covered option.

d.10.

To discuss: The meaning of in-the-money call.

d.10.

Explanation of Solution

The meaning of in-the-money call is as follows:

A call option where the strike price is less as compared to the market price is termed as in-the-money call. In other words, it is where the strike price of a put option is more than the market price of particular underlying assets.

d.11.

To discuss: The meaning of out-the-money call.

d.11.

Explanation of Solution

The meaning of out-the-money call is as follows:

A call option where the exercise price is more than the present price of particular underlying assets is termed as out-the-money call.

d.12.

To discuss: The meaning of LEAPS.

d.12.

Explanation of Solution

The meaning of LEAP is as follows:

A publicly traded options contract with an expiration dates, which are more than one year is termed as LEAP. It is an abbreviation of Long-term equity anticipation securities. This is same as the conventional option, but they are long-term option with the maturity period of two and half years.

e.1.

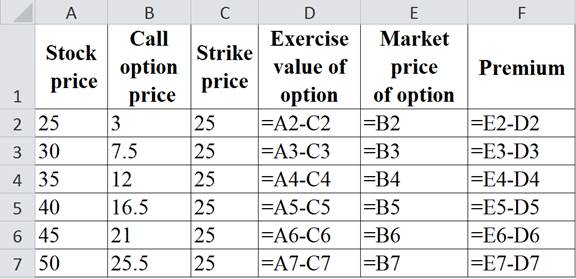

To determine: The strike price, stock price, exercise value, premium of option over the exercise value, and option price.

e.1.

Explanation of Solution

Given information:

TS Company has a call option with the strike price of $25. The call option prices at different stock price are as follows:

| Stock price |

Call option price |

| $25 | $3.00 |

| $30 | $7.50 |

| $35 | $12.00 |

| $40 | $16.50 |

| $45 | $21.00 |

| $50 | $25.50 |

The formula to compute the exercise value of option is as follows:

The formula to compute the premium of option over the exercise value is as follows:

Compute the strike price, stock price, exercise value, premium of option over the exercise value, and option price:

The table below shows the Excel formula to calculate the strike price, stock price, exercise value, premium of option over the exercise value, and option price:

The table below shows the calculated values of strike price, stock price, exercise value, premium of option over the exercise value, and option price:

e.2.

To discuss: The premium of option over exercise value when there is a raise in stock price and its reasons.

e.2.

Explanation of Solution

The premium of option over exercise value when there is a raise in stock price and its reasons are as follows:

From the above computation, it is clear that the premium of option price over the exercise value will fall tremendously when there is an increase in the price of the stock. It is because of the fall in the degree of leverage that is provided by the options when the underlying stock price rises.

f.1.

To discuss: The assumption of Black-Scholes option pricing model.

f.1.

Explanation of Solution

The assumptions of Black-Scholes option pricing model are as follows:

- The stock underlying call option does not provide any dividends at the lifetime of the option.

- Both the risk-free interest rate and short-term are stable at the lifetime of the option.

- Under this model, the call option can only be exercised on the date of expiration.

- In this model, there are no transactions costs involved at the time of sales or purchase of option or stock.

- A short-term selling is allowed without any penalty charges. Even the seller will receive immediately the whole cash proceeds at the current price of securities sold short.

f.2.

To discuss: The three equations that constitute Black-Scholes option pricing model.

f.2.

Explanation of Solution

The three equations that constitute Black-Scholes option pricing model are as follows:

- The first mathematical equation of Black-Scholes option pricing model is given below:

Where,

V refers to the value of option

P refers to the current price of stock

N(d1) refers to the probability where a deviation is less than d1.

X refers to the exercise price of option

N(d2) refers to the probability that the Stock price is greater than strike price

rRF refers to the risk-free rate

t refers to the number of periods

Note: The value of “e” is 2.718281828.

- The second mathematical equation which constitute Black-Scholes option pricing model is given below:

Where,

P refers to the current price of stock

X refers to the exercise price of option

rRF refers to the risk-free rate

t refers to the number of periods

σ2 refers to the variance of

rate of return on the stockIn refers to the natural logarithm

- The third mathematical equation which constitute Black-Scholes option pricing model is given below:

Where,

t refers to the number of periods

σ refers to the variance of the stock

f.3.

To determine: The value of call option as per the Black-Scholes option pricing model.

f.3.

Explanation of Solution

Given information:

The price of the stock is $27, exercise price is $25, and risk-free rate is 6 percent. The variance stock return is 0.11 and the period of expiration is 6 months.

The formula to compute the value of call option is as follows:

Where,

V refers to the value of option

P refers to the current price of stock

N(d1) refers to the probability where a deviation is less than d1.

X refers to the exercise price of option

N(d2) refers to the probability that the Stock price is greater than strike price

rRF refers to the risk-free rate

t refers to the number of periods

Note: The value of “e” is 2.718281828.

Compute the d1:

Hence, the value of d1 is 0.5735. Now, represent an area in a standard

Compute the value of d2:

Hence, the value of d2 is 0.339. Now, represent an area in a standard normal distribution curve using Appendix C. therefore, the N(d2) is 0.6327

Compute the value of call option:

Hence, the call option value as per this model is $4.00.

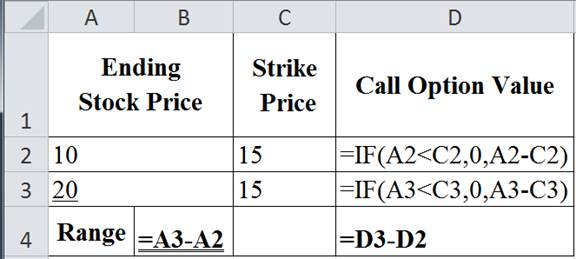

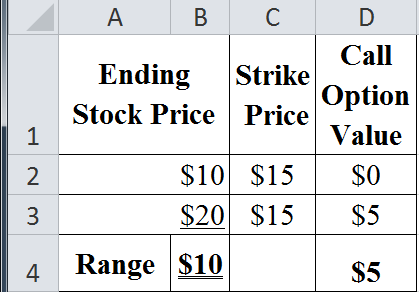

g.

To determine: The value of call option of the firm using binominal model.

g.

Explanation of Solution

Given information:

The price of the stock is $15 per share, exercise price is $15, and risk-free rate is 6 percent. The period of expiration is 6 months and selling price of the stock of the firm is $10 or $20.

The formula to compute the present value of the riskless portfolio is as follows:

The formula to compute the cost of the stock in the portfolio is as follows:

The formula to compute the market value of option is as follows:

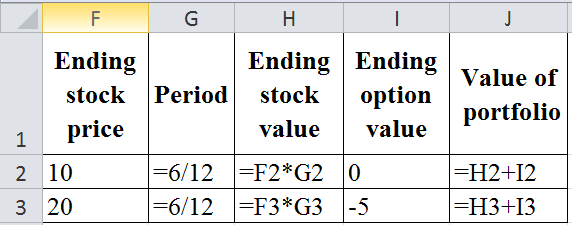

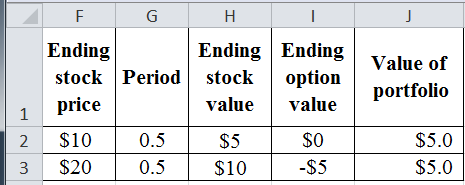

Compute the range:

The table below shows the Excel formula to calculate the range:

The table below shows the calculated values of range:

Hence, the range is $10 and the call option value is $5.

Compute the value of the portfolio at the end of six-month period:

The table below shows the Excel formula to calculate the value of the portfolio at the end of six-month period:

The table below shows the calculated values of the portfolio at the end of six-month period:

Compute the present value of the riskless portfolio:

Hence, the present value of the riskless portfolio is $4.86.

Compute the cost of the stock in the portfolio:

Hence, the cost of the stock in the portfolio is $7.5.

Compute the market value of the option:

Hence, the market value of option is $2.64.

h.1.

To discuss: The effect of current stock price has on the value of a call option.

Introduction:

Option is a contract to purchase a financial asset from one party and sell it to another party on an agreed price for a future date. There are two types of options, which are as follows:

- An option that buys an asset called call option

- An option that sells an asset called put option

h.1.

Explanation of Solution

The effect of current stock price has on the value of a call option is as follows:

The value of call option rises when there is a rise in the current stock price or vice-versa. Therefore, this is the effect of current stock price has on the value of a call option.

h.2.

To discuss: The effect of exercise price has on the value of a call option.

Introduction:

Exercise price is a price wherein a call or put options can be exercised in a derivative. It is also termed as Strike price.

h.2.

Explanation of Solution

The effect of exercise price has on the value of a call option is as follows:

The value of call option increases when there is a fall in the exercise price or vice-versa. It has an inverse relationship with the value of a call option. Therefore, this is the effect of exercise price has on the value of a call option.

h.3.

To discuss: The effect of length of the option period has on the value of a call option.

h.3.

Explanation of Solution

The effect of length of the option period has on the value of a call option is as follows:

The value of option increases when there is a longer expiration period. It is because the value of option mostly depends on three factors which are as follows:

- Probability of an increase in the price of stocks

- Longer option period

- Higher stock price

h.4.

To discuss: The effect of risk-free rate has on the value of a call option.

h.4.

Explanation of Solution

The effect of risk-free rate has on the value of a call option is as follows:

The value of option tends to rise when the risk-free rate increase. It is because an increase in the risk-free rate can decrease the present value of the exercise price of the option. As a result, it can also raise the current value of the option.

h.5.

To discuss: The effect of variability of the stock price has on the value of a call option.

h.5.

Explanation of Solution

The effect of variability of the stock price has on the value of a call option is as follows:

The price of stock can exceed the exercise price of the option at the time when there is a greater variance in the underlying price of stock. Therefore, the value of call option will be more valuable.

i.

To discuss: The difference between futures and forward contracts.

Introduction:

A type of financial security whose value is derived from the value of a particular underlying asset is termed as Derivative. This form of financial security consists of two or more parties who enter into an agreement to purchase or sell an asset at a specific price on a particular period. They are four types of derivative securities that are as follows:

- Forward contract

- Future contract

- Swap

- Option

i.

Explanation of Solution

The difference between futures and forward contracts are as follows:

- Forward contract is a derivative instrument, which agrees to buy or sell a financial instrument or a commodity in the future date at a present agreed price. It helps to eliminate the potential risk for the investors. However, futures contract is also a derivative instrument as well as a legal agreement. This contract is generally made on the trading floor of an organized exchange to buy or sell a financial instrument or a particular commodity at a predetermined price and time in future.

- Future contracts are popular instruments in derivatives. It is a widely used technique to hedge the financial risks of companies and investors. The buyer of the futures contract eliminates his or her price risk by entering into a legal agreement that promises a predetermined price to an instrument or a commodity at a predetermined time in the future. The forward contract is identical to a futures contract by its function.

However, the forward contract is unstandardized. As a result, parties in the forward contract have no common platform to buy and sell the contract, and hence, both parties have to find parties themselves to enter into a forward contract. It exacerbates the default risks of both parties. In the case of the futures contract, it is highly standardized and has a common exchange to buy and sell the futures contracts.

j.

To discuss: The working of swaps.

j.

Explanation of Solution

The working of swaps is as follows:

An exchange of obligation (cash payment) between two parties is termed as swap. Parties in swap contract mostly prefers the terms of other party’s debt contract. It is because the terms are more related to the cash flows of the firm. This derivative can reduce every party’s financial risk.

k.

To discuss: The ways how futures and swaps are used by the firm to hedge risk.

k.

Explanation of Solution

The ways how futures and swaps are used by the firm to hedge risk is as follows:

Hedging process is used by the firm when a price changes can negatively affect the profitability of the firm. A long hedge involves with the purchase of a futures contract in order to lookout against an increase in price. However, a short hedge mostly involves with the selling of a futures contract to protect against a price drop. As a result, the purchase of a commodity futures contract would permit to make a future purchase at the current market price. Therefore, it is a safer zone for the firm because the market price on the items might rise substantially in the future.

Swaps are used to match every cash flows of the firm. It is involved with either currencies or interest payments. For instance, Company B has $100 million bonds outstanding for 20-years that issued for fixed-interest rate and Company K has outstanding bonds of $100 million for 20- years, which is issued at floating-interest rate. At the time when the Company K has constant cash flows and decided to lock in its costs of debt, then it will prefer a fixed-rate obligation. However, the Company B has cash flows that fluctuate with the economy, so it will prefer a floating-rate obligation. It is because the interest rate will fluctuate with the economic changes. As a result, the Company B will mostly prefer variable-rate debt. Therefore, the companies can match their cash flows by swapping debt instruments and reduce financial risk.

l.

To discuss: The meaning of corporate risk management and reason for its importance to all the firms.

l.

Explanation of Solution

The meaning of corporate risk management and reason for its importance to all the firms are as follows:

The management of unpredictable events which would leads to an adverse result for the firm is termed as corporate risk management. It helps to reduce the consequence of risk to the extent where there will be no significant adverse effect on the financial position of the firm. Therefore, it function is very important to all the firms.

Want to see more full solutions like this?

Chapter 18 Solutions

Mindtap Finance, 1 Term (6 Months) Printed Access Card For Brigham/houston's Fundamentals Of Financial Management, 15th

- Ends Apr 27 Explain why we start with Sales forecasts when we do our financial forecasting. What are the limitations of the Percent of Sales Forecasting method?arrow_forwardDescribe in detail what exactly is the Cash Conversion Cycle, how is it computed and what is the purpose of this calculation (how is it used).arrow_forwardExplain what Interest Rate Parity is, how it is calculated, and why it is important to a company operating internationally.arrow_forward

- Compare and contrast the three core means of adding shareholder wealth; Cash Dividends, Stock Dividends and Stock Splits, and Stock Repurchases. Include the various advantages and disadvantages of each one.arrow_forwardHow to calculate the future value?arrow_forwardhow to caculate the future value?arrow_forward

- what are some of the question can i asek my prinsiple of finance teache?arrow_forwardA critical discussion of the hockey stick model of start-up financing should be presented, supported by recent in-text citations. Provide a detailed explanation of the model. Describe each of the three stages of the hockey stick model of start-up financing, including a detailed characterisation of each stage. The characterisation of each stage should detail the growth, risk, and funding expectations. Present a critical evaluation and an insightful conclu sion.arrow_forwardQuestion Workspace Check My Work New-Project Analysis The president of your company, MorChuck Enterprises, has asked you to evaluate the proposed acquisition of a new chromatograph for the firm's R&D department. The equipment's basic price is $64,000, and it would cost another $18,000 to modify it for special use by your firm. The chromatograph, which falls into the MACRS 3-year class, would be sold after 3 years for $28,400. The MACRS rates for the first three years are 0.3333, 0.4445 and 0.1481. (Ignore the half-year convention for the straight-line method.) Use of the equipment would require an increase in net working capital (spare parts inventory) of $3,000. The machine would have no effect on revenues, but it is expected to save the firm $24,760 per year in before-tax operating costs, mainly labor. The firm's marginal federal-plus-state tax rate is 25%. Cash outflows and negative NPV value, if any, should be indicated by a minus sign. Do not round intermediate…arrow_forward

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781285867977Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning