Calculate income tax amounts under various circumstances • LO16–1, LO16–2 Four independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences: The enacted tax rate is 40%. Required: For each situation, determine the: a. Income tax payable currently b. Deferred tax asset —balance c. Deferred tax asset—change (dr) cr d. Deferred tax liability —balance e. Deferred tax liability—change (dr) cr f. Income tax expense

Calculate income tax amounts under various circumstances • LO16–1, LO16–2 Four independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences: The enacted tax rate is 40%. Required: For each situation, determine the: a. Income tax payable currently b. Deferred tax asset —balance c. Deferred tax asset—change (dr) cr d. Deferred tax liability —balance e. Deferred tax liability—change (dr) cr f. Income tax expense

Solution Summary: The author explains how deferred tax is computed on the basis of tax liability on income as per income statement and the income per tax return.

Calculate income tax amounts under various circumstances

• LO16–1, LO16–2

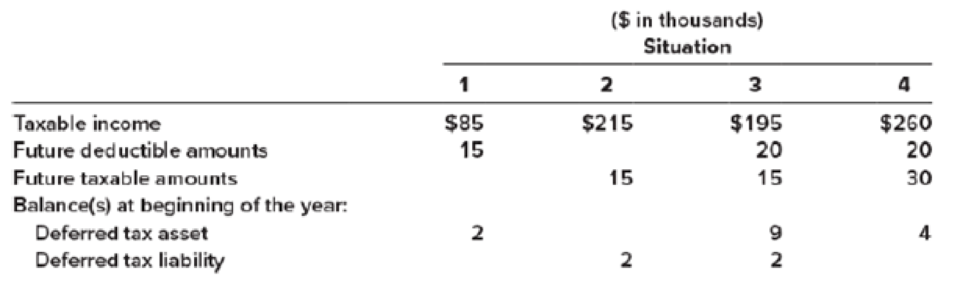

Four independent situations are described below. Each involves future deductible amounts and/or future taxable amounts produced by temporary differences:

The enacted tax rate is 40%.

Required:

For each situation, determine the:

a. Income tax payable currently

b. Deferred tax asset—balance

c. Deferred tax asset—change (dr) cr

d. Deferred tax liability—balance

e. Deferred tax liability—change (dr) cr

f. Income tax expense

Definition Definition Items on the balance sheet that are created when the tax paid is less than the tax considered on the income statement. A deferred tax liability is recorded on the liability side of the balance sheet and is thus a tax burden. It increases the taxes owed in the future.

JH, Inc., is a calendar year, accrual basis corporation with Joe as its sole shareholder (basis in his stock is $90,000). On January 1 of the current year, JH Corporation has accumulated E & P of $200,000. Before considering the effect of the distribution described below, the corporation’s current E & P is $50,000. On November 1, JH distributes an office building to Joe. The office building has an adjusted basis of $80,000 (fair market value of $100,000) and is subject to a mortgage of $110,000. Assume that the building has been depreciated using the ADS method for both income tax and E & P purposes. What are the tax consequences of the distribution to JH and to Joe? (In your answer, be sure to describe the effects on taxable income for both JH and Joe, the impact of the distribution on JH’s E & P, and Joe’s basis in the building.)

Joe is the sole shareholder of JH Corporation. Joe sold his stock to Ethan on October 31 for $150,000. Joe’s basis in JH stock was $50,000 at the start of the year. JH distributed land to Joe immediately before the sale. JH’s basis in the land was $20,000 (fair market value of $25,000). On December 31, Ethan received a $75,000 cash distribution from JH. During the year, JH has $20,000 of current E & P and its accumulated E & P balance on January 1 is $10,000. Which of the following statements is true?

a. Joe recognizes a $110,000 gain on the sale of his stock. b. Joe recognizes a $100,000 gain on the sale of his stock. c. Ethan receives $5,000 of dividend income.d. Joe receives $20,000 of dividend income. e. None of the above.

Please provide the accurate answer to this general accounting problem using appropriate methods.

Gitman: Principl Manageri Finance_15 (15th Edition) (What's New in Finance)

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning