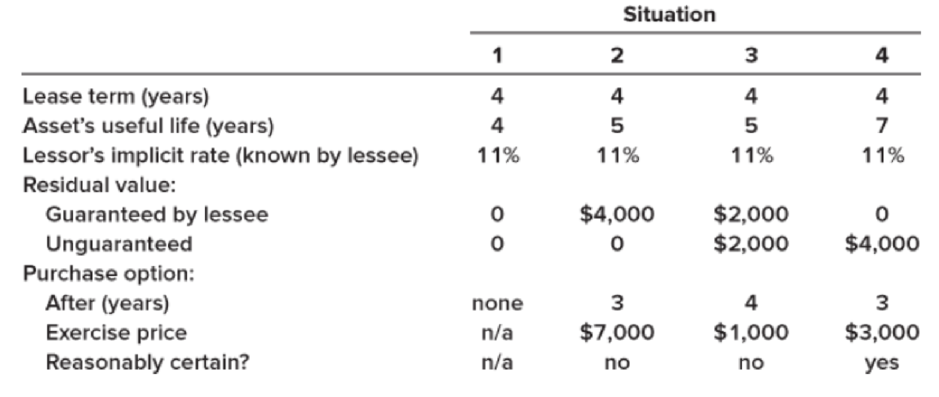

Lease concepts; sales-type leases; guaranteed and unguaranteed residual value • LO15–2, LO15–6 Each of the four independent situations below describes a sales-type lease in which annual lease payments of $10,000 are payable at the beginning of each year. Each is a finance lease for the lessee. Determine the following amounts at the beginning of the lease. A. The lessor’s: 1. Lease payments 2. Gross investment in the lease 3. Net investment in the lease B. The lessee’s: 4. Lease payments 5. Right-of-use asset 6. Lease liability

Lease concepts; sales-type leases; guaranteed and unguaranteed residual value • LO15–2, LO15–6 Each of the four independent situations below describes a sales-type lease in which annual lease payments of $10,000 are payable at the beginning of each year. Each is a finance lease for the lessee. Determine the following amounts at the beginning of the lease. A. The lessor’s: 1. Lease payments 2. Gross investment in the lease 3. Net investment in the lease B. The lessee’s: 4. Lease payments 5. Right-of-use asset 6. Lease liability

Lease concepts; sales-type leases; guaranteed and unguaranteed residual value

• LO15–2, LO15–6

Each of the four independent situations below describes a sales-type lease in which annual lease payments of $10,000 are payable at the beginning of each year. Each is a finance lease for the lessee. Determine the following amounts at the beginning of the lease.

A. The lessor’s:

1. Lease payments

2. Gross investment in the lease

3. Net investment in the lease

B. The lessee’s:

4. Lease payments

5. Right-of-use asset

6. Lease liability

(A)

Expert Solution

To determine

Lessee guaranteed residual value

The lessee guaranteed residual value of leased asset is an estimation of the commercial value of the asset at the end of lease term. The present value is considered when determining the lease classification criteria (Criteria 4). Lessee guaranteed residual value is added to lease receivable and also added to sales revenue.

To Determine: the amounts at the beginning of lease for the lessor at each independent situation.

Explanation of Solution

Situation

1

2

3

4

Lessor

Lease payments

(1) 40,000

(2) 40,000

(3) 40,000

(4)33,000

Gross investment

in the lease

(5)40,000

(6)44,000

(7)44,000

(8)33,000

Net investment

in the lease

(9)34,437

(10)37,072

(11)37,072

(12)29,319

Table (1)

Working note:

The lease payment is calculated as follows:

Lease payments (Situation 1) = [(Annual lease payments×Number of fixed payments) +Exercise price for options whose exercise is deemed reasonably certain]=[($10,000×4)+$0]=$40,000 (1)

Lease payments (Situation 2) = [(Annual lease payments×Number of fixed payments) +Exercise price for options whose exercise is deemed reasonably certain]=[($10,000×4)+$0]=$40,000 (2)

Lease payments (Situation 3) = [(Annual lease payments×Number of fixed payments) +Exercise price for options whose exercise is deemed reasonably certain]=[($10,000×4)+$0]=$40,000 (3)

Lease payments (Situation 4) = [(Annual lease payments×Number of fixed payments) +Exercise price for options whose exercise is deemed reasonably certain]=[($10,000×3)+$3,000]=$33,000 (4)

The gross investment in lease is calculated as follows:

The net investment in the lease is calculated as follows:

Net investment in lease(Situation 1) =[Annual lease payments×PVIFA(11%,4)]=[$10,000×3.44371]=$34,437 (9)

Net investment in lease(Situation 2) =[[Annual lease payments×PVIFA(11%,4)]+[Guaranteed lease payments×PVIF(11%,4)]]=[($10,000×3.44371)+($4,000×0.65873)]=$37,072 (10)

Net investment in lease(Situation 3) =[[Annual lease payments×PVIFA(11%,4)]+[Guaranteed lease payments×PVIF(11%,4)]+[Unguaranteed lease payments×PVIF(11%,4)]]=[($10,000×3.44371)+($2,000×0.65873)+($2,000×0.65873)]=$37,072 (11)

Net investment in lease(Situation 4) =[[Annual lease payments×PVIFA(11%,3)]+[Exercise price×PVIF(11%,3)]]=[($10,000×2.71252)+($2,000×0.73119)]=$29,319 (12)

(B)

Expert Solution

To determine

the amounts at the beginning of lease for the lessee at each independent situation.

Dunlop Systems applies manufacturing overhead to products based on standard machine-hours. The budgeted fixed manufacturing overhead cost for the most recent month was $28,800, and the actual fixed manufacturing overhead cost for the month was $29,320. The company based its original budget on 7,200 machine-hours. The standard hours allowed for the actual output of the month totaled 6,800 machine-hours. a. What was the overall fixed manufacturing overhead budget variance for the month? b. What was the fixed overhead rate? c. What was the volume variance?

I need help with this general accounting problem using proper accounting guidelines.

Chapter 15 Solutions

GEN COMBO INTERMEDIATE ACCOUNTING; CONNECT ACCESS CARD

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education