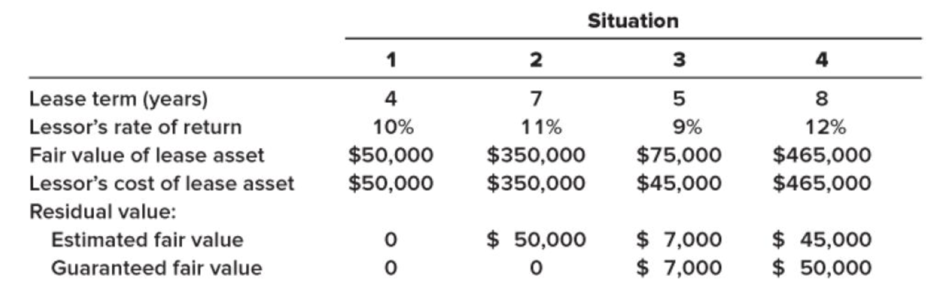

Calculation of annual lease payments; residual value • LO15–2, LO15–6 Each of the four independent situations below describes a finance lease in which annual lease payments are payable at the beginning of each year. The lessee is aware of the lessor’s implicit rate of return . Required: For each situation, determine: a. The amount of the annual lease payments as calculated by the lessor. b. The amount the lessee would record as a right-of-use asset and a lease liability.

Calculation of annual lease payments; residual value • LO15–2, LO15–6 Each of the four independent situations below describes a finance lease in which annual lease payments are payable at the beginning of each year. The lessee is aware of the lessor’s implicit rate of return . Required: For each situation, determine: a. The amount of the annual lease payments as calculated by the lessor. b. The amount the lessee would record as a right-of-use asset and a lease liability.

Solution Summary: The author explains that lease lease is a contractual agreement whereby the right to use an asset is provided by the owner to the user of the asset.

Calculation of annual lease payments; residual value

• LO15–2, LO15–6

Each of the four independent situations below describes a finance lease in which annual lease payments are payable at the beginning of each year. The lessee is aware of the lessor’s implicit rate of return.

Required:

For each situation, determine:

a. The amount of the annual lease payments as calculated by the lessor.

b. The amount the lessee would record as a right-of-use asset and a lease liability.

Definition Definition Percentage gain or loss from a specific investment over time. The rate of return is the difference between the closing and initial values of an investment divided by the initial value of the investment. The closing value includes any intermediate cash flows such as dividends or interest amounts.

(Situation 1) (a)

Expert Solution

To determine

Lease

Lease is a contractual agreement whereby the right to use an asset for a particular period of time is provided by the owner of the asset to the user of the asset. The owner, who possesses the asset, is termed as ‘Lessor’ and user, to whom the right is transferred to, is termed as ‘Lessee’.

To Determine: the annual lease payments as calculated by the lessor.

Explanation of Solution

Annual lease payments=Amount to be recovered (Fair Value)PVIFA(10%,4)=$50,0003.48685=$14,340

The lease payments at the beginning of each year is calculated by dividing fair value of the leased asset by present value of annuity for 4 years at the rate of 10%.

Conclusion

Therefore, annual lease payment as calculated by lessor is $14,340.

(Situation 1) (b)

Expert Solution

To determine

the amount that would be recorded as right-of-use asset and lease liability by the lessee.

Explanation of Solution

The lessor cost of lease asset is reported by the lessee as right-of-use asset$50,000.

Conclusion

Therefore, amount the lessee would record as right-of-use and lease liability is $50,000.

(Situation 2) (a)

Expert Solution

To determine

the annual lease payments as calculated by the lessor.

Explanation of Solution

Annual lease payments=Amount to be recovered (Fair Value)PVIFA(11%,7)=$325,917(2)5.23054=$62,310 (3)

Working notes:

Calculate the present value of residual value

Present value of residual value=Residual value(Estimated)×PVIF(11%,7)=$50,000×0.48166=$24,083 (1)

Calculate the amount to be recovered through periodic lease payments

Particulars

Amounts ($)

Amount to be recovered (Fair value)

350,000

Less: Present value of residual value (1)

24,083

Amount to be recovered through periodic lease payments

325,917

(2)

In case of lessor, even if the residual value is not guaranteed, the lessor is expected to receive. So, the lessor will assess the residual asset as contributing to amount needed to recover its investment causing the lessee’s lease payments to be lower.

Conclusion

Therefore, annual lease payment as calculated by lessor is $62,310.

(Situation 2) (b)

Expert Solution

To determine

the amount that would be recorded as right-of-use asset and lease liability by the lessee.

Explanation of Solution

Calculate the lessee would record as right-of-use asset and lease liability

Value to be recorded as right-of-use asset and lease liability}=Lease payments×PVIFA(11%,7)=$62,310(3)×5.23054=$325,917

Conclusion

Therefore, amount the lessee would record as right-of-use and lease liability is $325,917.

(Situation 3) (a)

Expert Solution

To determine

the annual lease payments as calculated by the lessor.

Explanation of Solution

Annual lease payments=Amount to be recovered (Fair Value)PVIFA(9%,5)=$70,450(5)4.23972=$16,617 (6)

Working notes:

Calculate the present value of residual value

Present value of residual value=Residual value(Estimated)×PVIF(9%,5)=$7,000×0.64993=$4,550 (4)

Calculate the amount to be recovered through periodic lease payments

Particulars

Amounts ($)

Amount to be recovered (Fair value)

75,000

Less: Present value of residual value (4)

4,550

Amount to be recovered through periodic lease payments

70,450

(5)

In case of lessor, even if the residual value is not guaranteed, the lessor is expected to receive. So, the lessor will assess the residual asset as contributing to amount needed to recover its investment causing the lessee’s lease payments to be lower.

Conclusion

Therefore, annual lease payment as calculated by lessor is $16,617.

(Situation 3) (b)

Expert Solution

To determine

the amount that would be recorded as right-of-use asset and lease liability by the lessee.

Explanation of Solution

Calculate the lessee would record as right-of-use asset and lease liability

Value to be recorded as right-of-use asset and lease liability}=Lease payments×PVIFA(9%,5)=$16,617(6)×4.23972=$70,450

Conclusion

Therefore, amount the lessee would record as right-of-use and lease liability is $70,450.

(Situation 4) (a)

Expert Solution

To determine

the annual lease payments as calculated by the lessor.

Explanation of Solution

Annual lease payments=Amount to be recovered (Fair Value)PVIFA(12%,8)=$444,806(9)5.56376=$79,947 (10)

Working notes:

Calculate the present value of excess guaranteed residual value

Present value of excess guaranteed residual value}=[Residual value(Guaranteed)−Residual value(Estimated)]×PVIF(12%,8)=[$50,000−$45,000]×0.40388=$2,019 (7)

Calculate the present value of residual value

Present value of residual value=Residual value(Estimated)×PVIF(12%,8)=$45,000×0.40388=$18,175 (8)

Calculate the amount to be recovered through periodic lease payments

Particulars

Amounts ($)

Amount to be recovered (Fair value)

465,000

Less: Present value of excess guaranteed residual value (7)

2,019

Less: Present value of residual value (8)

18,175

Amount to be recovered through periodic lease payments

444,806

(9)

If a lessee guaranteed residual value is expected, the present value of the payments is added to the present value of lease payments which the lessee records as right-of-use of asset and lease liability. In case of a finance lease, the lessor records it as lease receivable.

Conclusion

Therefore, annual lease payment as calculated by lessor is $79,947.

(Situation 4) (b)

Expert Solution

To determine

the amount that would be recorded as right-of-use asset and lease liability by the lessee.

Explanation of Solution

Calculate the lessee would record as right-of-use asset and lease liability

Value to be recorded as right-of-use asset and lease liability}=[Present value of periodic lease payments + Present value of excess guaranteed residual value]=[$444,806(9)+$2,019(7)]=$446,825

Conclusion

Therefore, amount the lessee would record as right-of-use and lease liability is $446,825.

Want to see more full solutions like this?

Subscribe now to access step-by-step solutions to millions of textbook problems written by subject matter experts!

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education