Recording Convertible Debt Zakin Co. recently issued $1,000,000 face value, 10%, 30-year subordinated debentures at 97. The debentures are redeemable at 103 upon demand by the issuer at any date upon 30 days notice 10 years after the issue. The debentures are convertible into $10 par value common stock of the Company at the conversion price of $12.50 per share for each $500 or multiple thereof of the principal amount of the debentures. Required 1. Explain how the conversion feature of convertible debt has a value to the: a. Issuer b. Purchaser 2. Management of Zakin Co. has suggested that in recording the issuance of the debentures, it should assign a portion of the proceeds to the conversion feature. a. What are the arguments for according separate accounting recognition to the conversion feature of the debentures? b. What are the arguments supporting accounting for the convertible debentures as a single element? 3. Assume that the company assigns no value to the conversion feature upon issue of the debentures. Assume further that five years after issue, debentures with a face value of $100,000 and book value of $97,500 are tendered for conversion on an interest payment date when the market price of the debentures is 104 and the common stock is selling at $14 per share and that the Company records the conversion as follows: Discuss the propriety of the preceding accounting treatment.

Recording Convertible Debt

Zakin Co. recently issued $1,000,000 face value, 10%, 30-year subordinated debentures at 97. The debentures are redeemable at 103 upon demand by the issuer at any date upon 30 days notice 10 years after the issue. The debentures are convertible into $10 par value common stock of the Company at the conversion price of $12.50 per share for each $500 or multiple thereof of the principal amount of the debentures.

Required

1. Explain how the conversion feature of convertible debt has a value to the:

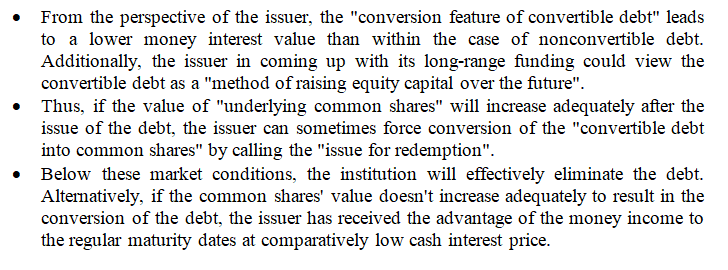

a. Issuer

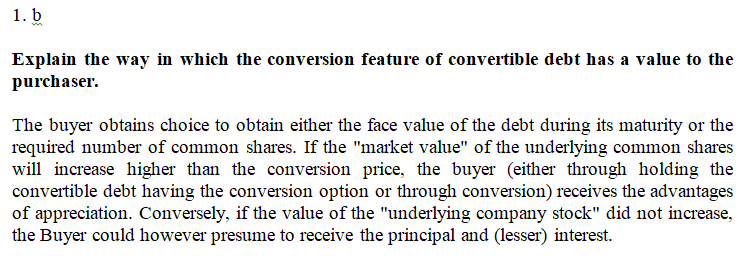

b. Purchaser

2. Management of Zakin Co. has suggested that in recording the issuance of the debentures, it should assign a portion of the proceeds to the conversion feature.

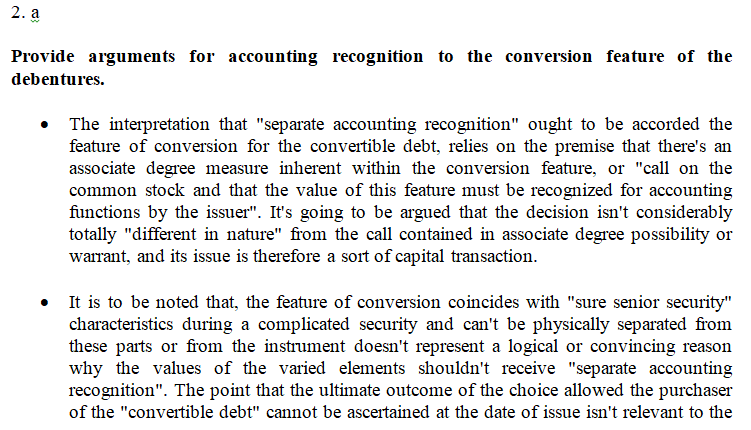

a. What are the arguments for according separate accounting recognition to the conversion feature of the debentures?

b. What are the arguments supporting accounting for the convertible debentures as a single element?

3. Assume that the company assigns no value to the conversion feature upon issue of the debentures. Assume further that five years after issue, debentures with a face value of $100,000 and book value of $97,500 are tendered for conversion on an interest payment date when the market price of the debentures is 104 and the common stock is selling at $14 per share and that the Company records the conversion as follows:

Discuss the propriety of the preceding accounting treatment.

- a

Explain the way in which the conversion feature of convertible debt has a value to the issuer.

Step by step

Solved in 5 steps with 10 images