Concept explainers

Issue of bond at premium:

When the coupon rate or contract rate of a bond is higher than the market interest rate, the bond is being issued at premium. If the bond is issued at premium, the selling price of the bond will be higher than the face value of the bond.

Under straight line amortization method, a specific amount of premium is amortized each period till its maturity period. The period ending amortization amount is computed by dividing the total premium by the number of periods in maturity of the bonds payable.

To determine:

1. Preparation of

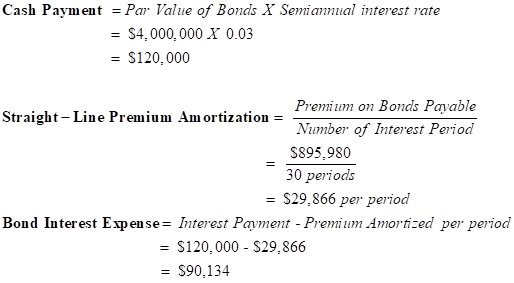

2. Computation of (a) the cash payment, (b) the straight-line premium amortization, and (c) the bond interest expense

3. Determine to total bond interest expense to be recognized over the life of the bonds.

4. Prepare the first two years of an amortization table using straight-line method.

5. Prepare the journal entries to record the first two interest payments.

Answer to Problem 3APSA

Solution:

1.

| Date | Accounts | Debit | Credit |

| 2015 | |||

| Jan. 1 | Cash | $4,895,980 | |

| Bonds Payable | $4,000,000 | ||

| Premium on Bonds Payable | $895,980 |

2.

| Semiannual Period | Amount |

| Cash Payment | $120,000 |

| Straight-line discount amortization | $29,866 |

| Bond Interest Expense | $149,866 |

3.

The total bond interest expense to be recognized over the bond’s life is $2,704,020.

4.

| Period Ending | Unamortized Premium | Carrying Value |

| 01/1/2015 | $895,980 | $4,895,980 |

| 06/30/2015 | $866,114 | $4,866,114 |

| 12/31/2015 | $836,248 | $4,836,248 |

| 06/30/2016 | $806,382 | $4,806,382 |

| 12/31/2016 | $776,516 | $4,776,516 |

5.

| Date | General Journal | Debit | Credit |

| 2015 | |||

| Jun. 30 | Interest Expense | $90,134 | |

| Premium on Bonds Payable | $29,866 | ||

| Cash | $120,000 | ||

| Dec. 31 | Interest Expense | $90,134 | |

| Premium on Bonds Payable | $29,866 | ||

| Cash | $120,000 |

Explanation of Solution

Explanation:

1. Computation of discount on bonds payable

2. Computation of cash payment, straight-line discount amortization, and the bond interest expense

3.

| Computation of total interest expense | |

| Amount to be repaid at maturity: | |

| Total Interest Payment | $3,600,000 |

| Par | $4,000,000 |

| Total amount to be repaid | $7,600,000 |

| Less : Selling Price of the Bonds | $4,895,980 |

| Total Bond Interest Expense | $2,704,020 |

4. The premium amortization amount of $29,866 deducted from both the unamortized premium column and carrying value of the bonds payable for every semiannual period.

5. Under straight line premium amortization, the same amount of interest expense, discount amortized and interest payment is recorded till the maturity of the bonds.

Conclusion:

The discount amortization for every semiannual period is $29,866 and carrying value of the bonds payable for the year ended December 31, 2016 is $4,776,516.

Want to see more full solutions like this?

Chapter 14 Solutions

Loose Leaf for Fundamentals of Accounting Principles and Connect Access Card

- Please solve this General accounting questions step by steparrow_forwardPlease provide the answer to this general accounting question using the right approach.arrow_forwardTaldon Manufacturing estimates 45,600 machine hours as its allocation base and anticipates total manufacturing overhead costs of $109,440. What is the predetermined overhead rate to be applied to jobs?arrow_forward

- Archer Logistics will ship all of the Canadian athletes' gear to Germany for the World Cup.arrow_forwardI am trying to find the accurate solution to this financial accounting problem with the correct explanation.arrow_forwardCan you explain the correct approach to solve this general accounting question?arrow_forward

- Dalton Co. sells its product for $15 per unit, with variable costs of $9 per unit. Its fixed costs for the year are $36,000, and it sold 15,000 units during the year. What is Dalton Co.'s operating leverage for the year? a) 1.5 b) 2.0 c) 1.25 d) 3.0arrow_forwardCorrect Answerarrow_forwardKindly help me with this General accounting questions not use chart gpt please fast given solutionarrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education