Concept explainers

Videos

CAMPUS DELI INC.

OPTIMAL CAPITAL STRUCTURE Assume that you have just been hired as business manager of Campus Deli (CD), which is located adjacent to the campus. Sales were $1,100,000 last year, variable costs were 60% of sales, and fixed costs were $40,000. Therefore, EBIT totaled $400,000. Because the university's enrollment is capped, EBIT is expected to be constant over time. Because no expansion capital is required, CD distributes all earnings as dividends. Invested capital is $2 million, and 80,000 shares are outstanding. The management group owns about 50% of the stock, which is traded in the over-the-counter market.

CD currently has no debt—it is an all-equity firm—and its 80,000 shares outstanding sell at a price of $25 per share, which is also the book value. The firm's federal-plus-state tax rate is 40%. On the basis of statements made in your finance text, you believe that CD's shareholders would be better off if some debt financing were used. When you suggested this to your new boss, she encouraged you to pursue the idea but to provide support for the suggestion.

In today's market, the risk-free rate, rRF, is 6%, and the market risk premium, RPM, is 6%. CD's unlevered beta, bU, is 1.0. CD currently has no debt, so its

- a. 1. What is business risk? What factors influence a firm's business risk?

2. What is operating leverage, and how does it affect a firm's business risk?

3. What is the firm's

return on invested capital (ROIC)? - b. 1. What do the terms financial leverage and financial risk mean?

2. How does financial risk differ from business risk?

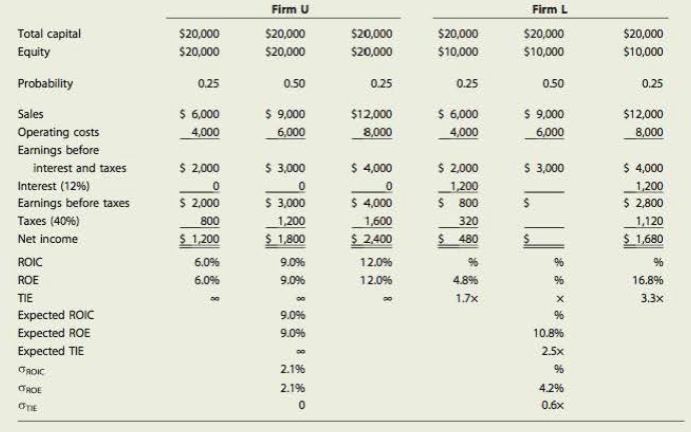

- c. To develop an example that can be presented to CD's management as an illustration, consider two hypothetical firms: Firm U with zero debt financing and Firm L with $10,000 of 12% debt. Both firms have $20,000 in invested capital and a 40% federal-plus-state tax rate, they have the following EBIT probability distribution for next year:

| Probability | EBIT |

| 0.25 | $2,000 |

| 0.50 | 3,000 |

| 0.25 | 4,000 |

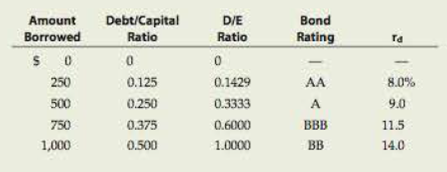

- d. After speaking with a local investment banker, you obtain the following estimates of the cost of debt at different debt levels (in thousands of dollars):

Now consider the optimal capital structure for CD.

1. To begin, define the terms optimal capital structure and target capital structure.

2. Why does CD's bond rating and cost of debt depend on the amount of money borrowed?

3. Assume that shapes could be repurchased at the current market price of $25 per share. Calculate CD's expected EPS and TIE at debt levels of $0, $250,000, $500,000, $750,000, and $1,000,000. How many shares would remain after recapitalization under each scenario?

4. Using the Hamada equation, what is the cost of equity if CD recapitalizes with $250,000 of debt? $500,000? $750,000? $1,000,000?

5. Considering only the levels of debt discussed, what is the capital structure that minimizes CD's WACC?

6. What would be the new stock price if CD recapitalizes with $250,000 of debt? $500,000? $750,000? $1,000,000? Recall that the payout ratio is 100%, so g = 0.

7. Is EPS maximized at the debt level that maximizes share price? Why or why not?

8. Considering only the levels of debt discussed, what is CD's optimal capital structure?

9. What is the WACC at the optimal capital structure?

- e. Suppose you discovered that CD had more business risk than you originally estimated. Describe how this would affect the analysis. How would the analysis be affected if the firm had less business risk than originally estimated?

Income Statements and Ratios TABLE IC 13.1

- f. What are some factors a manager should consider when establishing his or her firm's target capital structure?

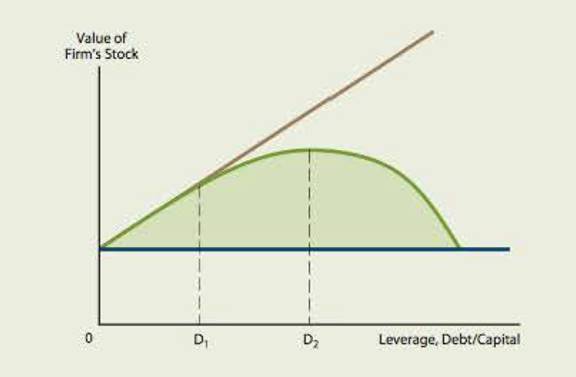

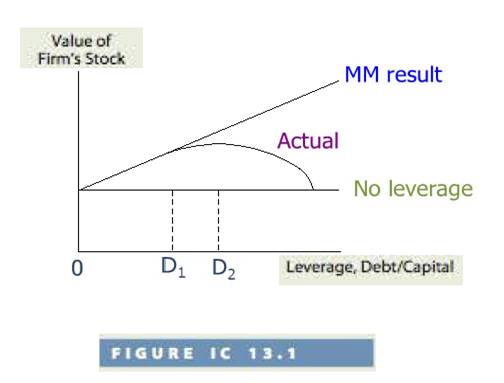

- g. Put labels on Figure IC 13.1 and then discuss the graph as you might use it to explain to your boss why CD might want to use some debt.

- h. How does the existence of asymmetric information and signaling affect capital structure?

FIGURE IC 13.1 Relationship between Capital Structure and Stock Price

a.1.

To determine: Business risk and factors which influence firm’s business risks.

Introduction:

Optimal Capital Structure:

The optimum mix of debt and equity in the capital structure of the company is known as the optimum capital budget. The optimum capital budget is also known as the optimum capital structure.

Business Risk:

Business risks are elements which have an adverse effect on the performance and profitability of the business.

Answer to Problem 15IC

- Business risks are elements which have an adverse effect on the performance and profitability of the business.

- Business risks are events and uncertainties that minimize the chances of expected profits and the business may face losses instead of earning profits.

Explanation of Solution

Given below are the factors which influence the firm’s business risks:

Business risks differ from business to business and from department to department.

Given below are the factors which influence the firm’s business risks:

- Fluctuation in the demand of the product

- Fluctuation in the selling price of the product.

- Fluctuation in the cost of its inputs.

- Competition in the market.

- Regulations by the government.

- Economic factors such as variations in market conditions.

Thus, management should work towards minimizing the business risks in order to achieve expected profits.

2.

To determine: Operating leverage and its effect on firm’s business risk.

Introduction:

Operating Leverage:

Operating leverage is the proportion of the fixed cost of the business in comparison to the total cost of the business.

Explanation of Solution

- Operating leverage is the proportion of the fixed cost of the business in comparison to the total cost of the business.

- Businesses with high fixed cost are more dependent on the volume of sales to cover high fixed costs.

- A high proportion of fixed costs indicate high operating leverage and as a result higher business risk in return.

- Operating leverage has a direct effect on the firm’s business risk.

- Since higher operating leverage indicates high fixed cost which cannot be cut down and require a high volume of sales to cover it.

- Change in profits due to the high volume of sales is higher than the change in the proportion of sales. Similarly, change in losses is more than the change in sales proportion.

- Thus in a situation of high sales volume, business benefits from high operating leverage and similarly in a situation of low sales volume, business will incur losses due to high fixed costs.

Thus, increase in operating leverage causes increases in business risk.

3.

To explain: Return on invested capital.

Introduction:

Return on Invested Capital:

Return on invested capital indicates the capability of the firm in generating revenue against the sum invested.

Answer to Problem 15IC

- Return on invested capital indicates the capability of the firm in generating revenue against the sum invested.

- It is the proportion of revenue generated by the sum total of funds raised by the firm.

- It indicates how productive and efficient a firm is in utilizing its funds to generate revenue.

Explanation of Solution

- Invested capital represents the sum total of all the funds invested in the firm by shareholders, lenders. Thus return on invested capital is the proportion of profit generated by the firm against the sum total of funds invested throughout the life of the firm.

- It evaluates the capability of the firm in converting its capital into revenue.

- Return on invested capital is a tool to measure the efficiency of the firm in utilizing its invested funds.

Thus, return on invested capital is a tool to measure the firm’s efficiency.

b.1.

To explain: Financial leverage and financial risks.

Introduction:

Financial Leverage:

Financial leverage indicates the extent of fixed income securities is utilized to purchase additional assets.

Financial Risks:

Financial risks are generally referred to risks that arise due to financial decisions.

Answer to Problem 15IC

- Financial leverage indicates the degree of debt utilized to purchase new equipment in order to achieve high sales volume and thus high revenue from sales.

- Financial leverage gives easy access to funds and raises the profitability and shareholder’s revenue.

- Financial risk is directly related to financial leverage as higher debt ratio demands a higher amount of repayments along with interest payments.

Explanation of Solution

- Financial leverage is a tool to measure the proportion of debt in funding or purchasing assets.

- Financial risk is the risks due to a high degree of debt in its financing decisions.

Thus, financial leverage is the extent of debt in purchasing additional assets whereas financial risks deal with the degree of risk related with financing decisions.

2.

To explain: Difference between financial risk and business risk.

Introduction:

Financial Risks:

Financial risks are generally referred to risks that arise due to financial decisions.

Business Risk:

Business risks are elements which have an adverse effect on the performance and profitability of the business.

Answer to Problem 15IC

- Financial risk represents the capability of the firm to control its debt and financial leverage.

- Business risk refers to firm’s degree of risk in generating sufficient revenue in order to cover its operational expenses.

- Business risks are events and uncertainties that minimize the chances of expected profits and the business may face losses instead of earning profits.

Explanation of Solution

- Financial risks are risks that arise only because of the extent of debt utilized in financing decisions.

- Therefore, there is a possibility that the firm will have a negative effect due to high debt ratio in.

- Business risks, on the other hand, depending on a number of factors such as sales volume, government regulations, and economic factors.

Thus, mentioned above are the differences between financial and business risks.

c.1.

To prepare: Partial income statement and the firm’s ratios.

Explanation of Solution

Given information:

Total assets for both firms are $20,000.

The tax rate for both firms is 40%.

The debt ratio for Firm U is 0%.

The debt ratio for firm L is 50%.

Cost of debt for firm L is 12%.

Given below is the partial income statement:

| Income Statement | ||||||

| FIRM U | FIRM L | |||||

| Probability | 0.25 | 0.50 | 0.25 | 0.25 | 0.50 | 0.25 |

| EBIT | 2,000 | 3,000 | 4,000 | 2,000 | 3,000 | 4,000 |

| Interest exp | 0 | 0 | 0 | 1,200 | 1,200 | 1,200 |

| EBT | 2,000 | 3,000 | 4,000 | 800 | 1,800 | 2,800 |

| Taxes (40%) | 800 | 1,200 | 1,600 | 320 | 720 | 1,120 |

| Net Income | 1,200 | 1,800 | 2,400 | 480 | 1,080 | 1,680 |

| BEP | 10% | 15% | 20% | 10% | 15% | 20% |

| ROE | 6% | 9% | 12% | 4.8% | 10.8% | 16.8% |

| TIE |

|

|

| 1.7 | 2.5 | 3.3 |

| E(BEP) | 15% | 15% | ||||

| E(ROE) | 9% | 10.8% | ||||

| E(TIE) | 2.5 | |||||

| SD(BEP) | 3.5% | 3.5% | ||||

| SD (ROE) | 2.1% | 4.2% | ||||

| SD(TIE) |

| 0.6 | ||||

Table (1)

2.

To identify: Impact of financial leverage on the expected rate of return and risk.

Explanation of Solution

The firm’s basic earning power remains to be uninfluenced by financial leverage.

Formula to calculate basic earning power (BEP) is,

Firm L is computed to have higher expected ROE:

Firm U:

ROE, when probability is 0.25, is 6%

ROE, when probability is 0.50, is 9%

ROE when the probability is 0.25. is 12%

Firm L:

ROE, when probability is 0.25, is 4.80%

ROE, when probability is 0.50, is 10.80%

ROE when the probability is 0.25. is 16.80%

Formula to calculate combined ROE of Firm U and Firm L when EBIT probability distribution is 0.25, 0.50 and 0.25.

Where,

Firm U:

Substitute 6% for

Firm L:

Substitute 4.8% for

Application of financial leverage has increased the anticipated yield to shareholders.

- Firm L has an extensive range of ROEs and higher standard deviation of ROE which indicated a higher degree of risk.

Therefore, firm L is double as risky as firm U.

The formula to calculate the financial risk of firm L is,

Substitute 4.24% for standalone risk and 2.12% for business risk

At the point when EBIT is $200,000, ROE of firm U exceeds ROE of firm L and leverage has a contrary influence on the profitability whereas, at a point of the anticipated level of EBIT, ROE of firm L is more than ROE of firm U.

Leverage tends to increase anticipated return on equity if the anticipated unleveraged return on assets is more than the after-tax cost of debt

The formula to calculate the cost of debt is,

Therefore, leverage tends to increase anticipated return on equity as the anticipated unleveraged return on assets which is 9%is more than the after-tax cost of debt which is 7.2%.

Therefore utilization of debt increases anticipated ROE.

TIE ratio is vast in case no debt is utilized whereas it is comparatively less if fifty percent debt is utilized. TIE ratio will be lower in case leverage is raised.

Mentioned above is the influence of financial leverage on the expected rate of return and risk.

d.1.

To discuss: The meaning of Optimal Capital Structure and Target Capital Structure.

Introduction:

Optimal Capital Structure:

The optimum mix of debt and equity in the capital structure of the company is known as the optimum capital budget. The optimum capital budget is also known as the optimum capital structure.

Target Capital Structure:

The optimal capital structured required by the firm in order to maintain firm’s stock price.

Answer to Problem 15IC

- Optimal capital structure signifies the ideal combination of debt and equity for the purpose of operations and growth of the firm.

- It reduces the cost of capital firm by minimizing the dependency on creditors.

- Target capital structure is the combination of debt and equity for maximizing the value of the firm.

- Target capital structure is the best capital structured required by the firm in order to maintain firm’s stock price.

Explanation of Solution

- The optimal capital structure represents the best combination of debt and equity for maximizing the value of the firm.

- Whereas target capital structure is the desired capital structure by the firm in order to maintain firm’s stock price.

The optimal capital structure is the best mix of debt and equity whereas target capital structure is the combination of debt and equity desired to be maintained by the firm.

2.

To determine: Dependence of bond rating and cost of debt on the amount of money borrowed.

Introduction:

Bond Rating:

The bond rating is the classification of a different class of bonds depending on factors such as creditworthiness of bonds, its ability to pay interest and principal timely.

Cost of Debt:

Cost of debt represents the percentage of amount company pays as interest on the borrowed funds.

Answer to Problem 15IC

- As the amount of borrowed money increases, the liability to repay the borrowed funds along with interest also increases.

- Increase in borrowed money can lead to increase in company’s risk to repay its investors which subsequently affects the bond's rating and so it’s cost of debt increases.

- As a result, change in credit rating will also affect the cost of debt, thus, low credit ratings will increase the cost of borrowing of funds.

Explanation of Solution

- Due to the increase in the volume of borrowed funds, the firm’s liability to repay its debt along with interest also increases the degree of business risk.

- Subsequently, it affects the creditworthiness of bonds by lowering the credit rating of bonds.

- Due to low credit ratings, cost of raising funds increases hence cost of debt increases due to low credit ratings.

Thus, amount of borrowed money affects the bond rating and cost of debt as well.

3.

To compute: C Company’s EPS and TIE.

Explanation of Solution

Given below is the calculation of EPS, when

Given,

EBIT of C Company is $400,000.

Outstanding shares of C Company are 80,000.

Tax rate is 40% or 0.40.

The formula to calculate EPS,

Where,

- EPS is Earnings per Share.

- EBIT is Earnings before Interest and Tax.

- D is debt ratio.

- T is tax rate.

Substitute $400,000 for EBIT, 0 for D, 0.4 for tax rate T and 80,000 for outstanding shares.

Given below is the calculation of EPS, when

Given,

EBIT of C Company is $400,000.

Tax rate is 40% or 0.40.

Formula to calculate outstanding shares:

Substitute 80,000 shares for shares outstanding in the beginning and

Formula to calculate EPS,

Where,

- EPS is Earnings per Share.

- EBIT is Earnings before Interest and Tax.

- D is debt.

-

- T is tax rate.

Substitute $400,000 for EBIT, 0.08 for rd, 250,000 for D, 0.4 for tax rate T and 70,000 for outstanding shares.

Formula to calculate TIE,

Where,

- TIE is Time Interest earned.

- EBIT is Earnings before Interest and Tax.

Substitute $400,000 for EBIT and $20,000 for interest.

Given below is the calculation of EPS, when

Given,

EBIT of C Company is $400,000.

Tax rate is 40% or 0.40.

Formula to calculate outstanding shares:

Substitute 80,000 shares for shares outstanding in the beginning and

Formula to calculate EPS,

Where,

- EPS is Earnings per Share.

- EBIT is Earnings before Interest and Tax.

- D is debt ratio.

- T is tax rate.

Substitute $400,000 for EBIT, 0.09 for rd, 500,000 for D, 0.4 for tax rate T and 60,000 for outstanding shares.

Formula to calculate TIE,

Where,

- TIE is Time Interest earned.

- EBIT is Earning before Interest and Tax.

Substitute $400,000 for EBIT and $45,000 for interest.

Given below is the calculation of EPS, when

Given,

EBIT of C Company is $400,000.

Tax rate is 40% or 0.40.

Formula to calculate outstanding shares:

Formula to calculate EPS,

Where,

- EPS is Earnings per Share.

- EBIT is Earnings before Interest and Tax.

- D is debt ratio.

- T is tax rate.

Substitute $400,000 for EBIT, 0.115 for rd, 750,000 for D, 0.4 for tax rate T and 50,000 for outstanding shares.

Formula to calculate TIE,

Where,

- TIE is Time Interest earned.

- EBIT is Earnings before Interest and Tax.

Substitute $400,000 for EBIT and $86,250 for interest.

Given below is the calculation of EPS, when

Given,

EBIT of C Company is $400,000.

Tax rate is 40% or 0.40.

Formula to calculate outstanding shares:

Formula to calculate EPS,

Where,

- EPS is Earnings per Share.

- EBIT is Earnings before Interest and Tax.

- D is debt ratio.

- T is tax rate.

Substitute $400,000 for EBIT, 0.14 for rd, 1,000,000 for D, 0.4 for tax rate T and 40,000 for outstanding shares.

Formula to calculate TIE,

Where,

- TIE is Time Interest earned.

- EBIT is Earnings before Interest and Tax.

Substitute $400,000 for EBIT and $140,000 for interest.

4.

To compute: Cost of equity.

Introduction:

Hamada Equation:

Hamada equation is a tool to measure the effect of an increase in debt on the cost of equity. It is used to distinguish the financial risk of a levered firm from its business risk.

Explanation of Solution

Given information:

The tax rate is 40%.

Total assets are $20,000,000.

Given below is the Hamada equation:

Where,

T is tax rate.

Given below is the CAPM equation,

Where,

Given below is the computation of cost of equity using Hamada equation:

| C Company | ||||

|

Amount borrowed($) |

Debt/assets ratio |

Debt/equity ratio |

Leveraged beta |

Cost of equity |

| 0 | 0 | 0 | 1.00 | 12.00% |

| 250,000 | 0.1250 | 0.1429 | 1.09 | 12.51% |

| 500,000 | 0.2500 | 0.3333 | 1.20 | 13.20% |

| 750,000 | 0.3750 | 0.6000 | 1.36 | 14.16% |

| 1,000,000 | 0.5000 | 1.0000 | 1.60 | 15.60% |

Above table computes the cost of equity using Hamada equation.

5.

To compute: Capital structure that minimizes C Company’s WACC.

Explanation of Solution

Given information:

Tax rate is 40% or 0.40.

Total assets are $20,000,000.

Given below is the Hamada equation:

Where,

T is tax rate.

Given below is the CAPM equation,

Where,

Where,

E is the market value of the firm’s equity (market cap).

D isthe market value of the firm’s debt.

V is the total value of capital (equity plus debt).

T is tax rate.

| C Company | ||||||||

|

Amount borrowed($) |

Debt/assets Ratio % |

Equity/assets Ratio % |

Debt/equity Ratio % | Leveraged beta |

Cost Of equity

|

|

| WACC |

| 0 | 0 | 100.00 | 0.00 | 1.00 | 12.00 | - | - | 12.00 |

| 250,000 | 12.50 | 87.50 | 14.29 | 1.09 | 12.51 | 8.00 | 4.8 | 11.55 |

| 500,000 | 25.00 | 75.00 | 33.33 | 1.20 | 13.20 | 9.00 | 5.4 | 11.25 |

| 750,000 | 37.50 | 62.50 | 60.00 | 1.36 | 14.16 | 11.50 | 6.9 | 11.44 |

| 1,000,000 | 50.00 | 50.00 | 100.00 | 1.60 | 15.60 | 14.00 | 8.4 | 12.00 |

Hence, C Company’s WACC is minimized at a capital structure, which is a combination of 25 % debt and 75% equity, or a WACC of 11.25%.

6.

To compute: New stock price.

Explanation of Solution

|

Amount borrowed |

Dividend per share | Cost of equity

| Stock price |

| 0 | 3.00 | 12.00 | 25.00 |

| 250,000 | 3.26 | 12.51 | 26.03 |

| 500,000 | 3.55 | 13.20 | 26.89 |

| 750,000 | 3.77 | 14.16 | 26.59 |

| 1,000,000 | 3.90 | 15.60 | 25.00 |

Hence, the capital structure with the highest yield, which is 26.89, will be accepted as the new stock price.

7.

To identify: EPS is not maximized at the debt level which increases the share prices.

Answer to Problem 15IC

- EPS increases even after achieving its optimal level of debt which is $500,000.

- Therefore it is not correct to take into consideration EPS for making capital structure decisions.

Explanation of Solution

- Also, EPS does not take into consideration the increase in risk to be suffered by the equity holders, whereas stock prices do reflect these factors.

- Thus, the stock prices will be highest at that point where debt level is below the level where EPS is maximizing.

Thus, EPS is not maximized at the debt level which maximizes share prices.

8.

To identify: C Company’s optimal capital structure.

Introduction:

Optimal Capital Structure:

The optimum mix of debt and equity in the capital structure of the company is known as the optimum capital budget. The optimum capital budget is also known as the optimum capital structure.

Answer to Problem 15IC

- Optimal capital structure signifies the ideal combination of debt and equity for the purpose of operations and growth of the firm.

- Highest stock price is $26.89 which is produced at a point where capital structure consists of $500,000 debt.

Explanation of Solution

- $500,000 debt will be observed as the ideal point to be identified as the optimal capital structure.

- Optimum capital structure with $500,000 debt gives the highest outcome of $26.89 stock price.

- Thus at $26.89, the value of C Company will be maximized.

Hence,$500,000 debt will be the point of the optimum capital structure.

9

To identify: WACC at the optimum capital structure.

Introduction:

Weighted Average Cost of Capital (WACC):

Weighted average cost of capital is a financial tool to measure the sum total of all the sources of capital to the firm.

Answer to Problem 15IC

- As per above table, we can conclude that WACC at the optimum capital structure is 11.25%.

- It has been observed that at this point, the stock price is at its highest and also the WACC is at its lowest, which indicates a low degree of risks.

Explanation of Solution

- Low WACC is deemed to be good as low WACC signifies the lower degree of risk.

- Lower WACC also creates a higher valuation for the firm by expanding the range of firm by generating value from low return projects.

Hence, at the point of the optimum capital structure of $500,000 debt, WACC is 11.25%.

e

To identify: Risk analysis of C Company

Answer to Problem 15IC

- In case it is discovered that C Company has higher business risk than the estimated risk, it will indicate a high degree of financial risk in the Company.

- As a result, it will lead to increase in the cost of debt and cost of equity.

- Similarly, in case of business risk is lower than the original risk estimated, then it represents a point of the optimal capital structure.

Explanation of Solution

- Increase in cost of debt will create a situation of higher financial risks which represent the inability of the company to pay its debts.

- Whereas a decrease in business risks represents a point of low debt and hence low financial risks and hence is an ideal situation of the optimum capital structure.

Hence, increase in business will increase the financial risk of company and decrease in business risk will lower the financial risks.

f.

To identify: Factors to be considered while establishing firm’s target capital structure.

Explanation of Solution

Given below are the factors to be considered while establishing firm’s target capital structure:

- The average debt ratio for the company in respective industries.

- Pro forma TIE ratios at different capital structures under different situation.

- The attitudeof lender or rating agency.

- Borrowing of money at a reasonable cost.

- Consequences of financing on control

- The composition of assets.

- The rate of tax expected.

- Target capital structure is the combination of debt and equity for maximizing the value of the firm.

- Target capital structure is the best capital structured required by the firm in order to maintain firm’s stock price.

Factors mentioned above need to be taken into consideration before establishing firm’s target capital structure.

g.

To prepare: Graph

Explanation of Solution

Given information:

Given below is the graph labeled as required:

- The use of debt for raising funds increases the financial risk of the firm thereby increases the amount of interest payment along with the principal.

- Therefore it increases the chances of bankruptcy which leads to increased cost of debt.

- Raising debt has its advantages also, as it assists in saving taxes by allowing the deduction of interest.

Therefore optimal capital structure is the point where firm’s tax savings are in tune with the marginal bankruptcy-related costs.

h.

To identify: Affect of asymmetric information and signaling on capital structure.

Answer to Problem 15IC

- Management’s selection of financing gives an indication to the investors.

- Firms with great investment options do not want to give their stake to the investors and hence use debt in order to raise funds.

- On the other hand, firms with low expectation will raise funds through issue of equity.

Explanation of Solution

- When a big Company raises funds through issue of equity or stock, this is deemed to be an indicator of troublesome news for the company and as a result the stock price falls.

- Hence firms avoid selling their new common stock thereby retain their reserve of borrowing capacity in order to utilize it at a time good opportunities.

Management should carefully select their financing course as it gives a fair idea to the investors.

Want to see more full solutions like this?

Chapter 13 Solutions

FUND. OF FINANCIAL MGMT CONCISE (LL)

- If data is unclear or blurr then comment i will write it. please don't use AI i will unhelpfularrow_forwardYou are considering an option to purchase or rent a single residential property. You can rent it for $5,000 per month and the owner would be responsible for maintenance, property insurance, and property taxes. Alternatively, you can purchase this property for $204,500 and finance it with an 80 percent mortgage loan at 4 percent interest that will fully amortize over a 30-year period. The loan can be prepaid at any time with no penalty. You have done research in the market area and found that (1) properties have historically appreciated at an annual rate of 2 percent per year, and rents on similar properties have also increased at 2 percent annually; (2) maintenance and insurance are currently $1,545.00 each per year and they have been increasing at a rate of 3 percent per year; (3) you are in a 24 percent marginal tax rate and plan to occupy the property as your principal residence for at least four years; (4) the capital gains exclusion would apply when you sell the property; (5)…arrow_forwardIf data is unclear or blurr then comment i will write it.arrow_forward

- I need answer typing clear urjent no chatgpt used pls i will give 5 Upvotes.arrow_forwardcorrect an If image is blurr or data is unclear then plz comment i will write values or upload a new image. i will give unhelpful if you will use incorrect data.arrow_forwardWhat are the five management assertions that serve as basis for financial statements audit programs?arrow_forward

- PROBLEM 2 On July 1, 2022, LTU Contracting, Inc. purchased a new Peiner SK575 Tower Crane for a total cost of $875,000. The crane has an estimated useful life of five (5) years. For financial reporting (book) purposes, the company utilizes straight line depreciation. For tax purposes, the equipment is depreciated over five years utilizing the 200% declining balance method. A. Prepare a table that computes the book and tax depreciation for each year of the useful life and determine the difference in book value between each method at the end of each year. B. On July 1st, 2025, the company is considering selling the crane for $500,000. Compute what the gain or loss would have been at that time for both book and tax purposes.arrow_forwardBrightwoodę Furniture provides the following financial data for a given enod: Sales Aount ($) Per Unit ($) 150,000 13 Less Variable E - L96,000 13 Contribwaon Margin c 1C Less Fixed Expenses $5,000 et Income 125,000 a. What is the company's CM ratio? b. If quarterly sales increase by $5,200 and there is no change in fixed expenses, by how much would you expect quarterly net operating income to increase?arrow_forwardPlease give correct answer dont use chatgpt . if image is blurr or any data is unclear then please comment i will write values , dont give answer without sure that data in image is showing properly.arrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning