1.

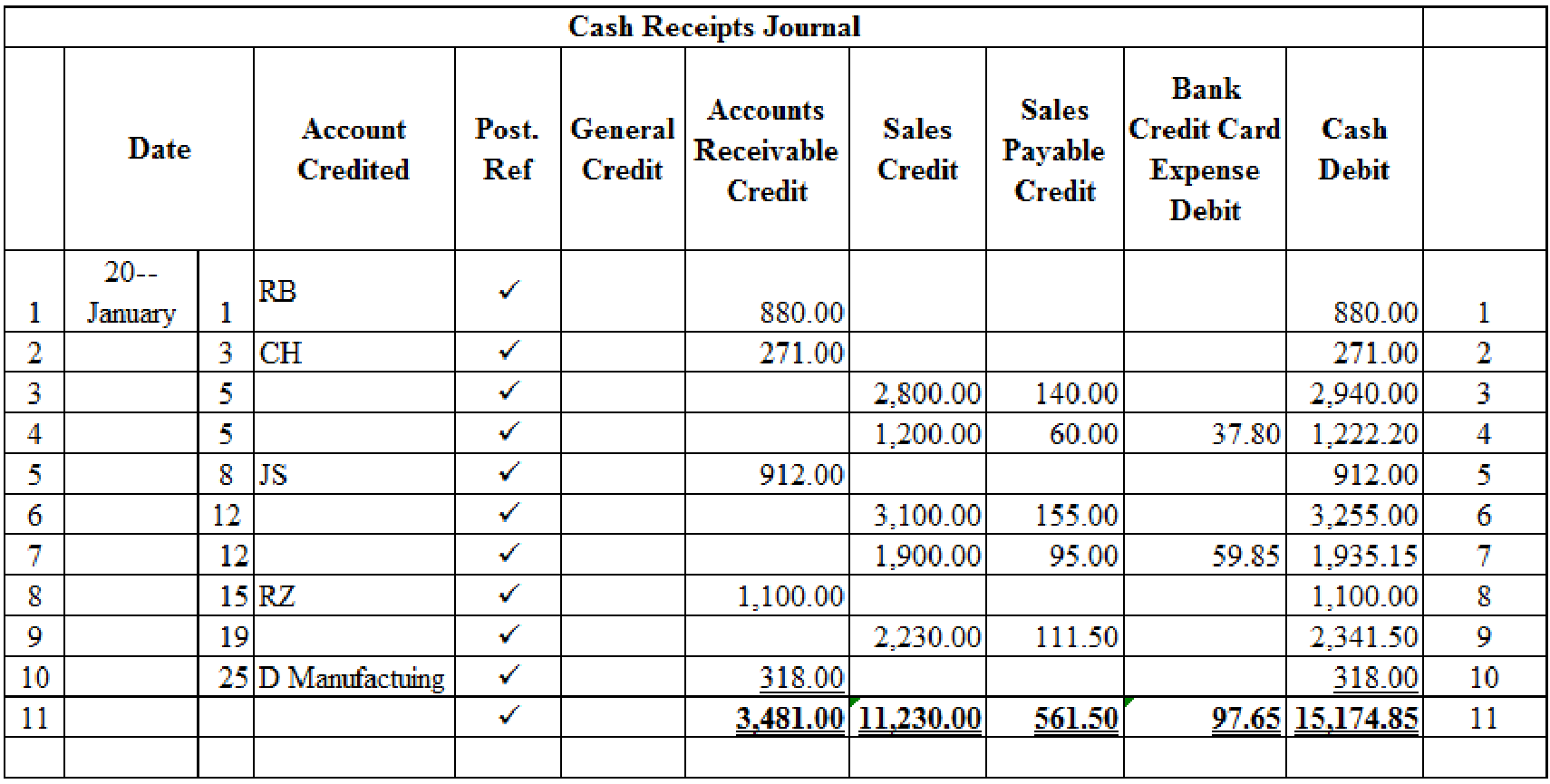

Prepare the given transactions in the cash receipts journal and verify the total column and rule the column and use the general journal to record the sales returns and allowances.

1.

Explanation of Solution

Cash Receipts Journal: It is a special book where only cash receipts transactions that are received from customers, merchandise sales and service made in cash and collection of accounts receivable are recorded.

The following are the some examples of transactions that would be recorded in the Other Accounts credit column of the cash receipts journal:

- • Cash received as interest on notes payable

- • Interest revenue received from debtors

- • Cash receipts from bank loans

- • Cash receipts for capital investments

Prepare the given transactions in the cash receipts journal and verify the total column and rule the column and use the general journal to record the sales returns and allowances:

Table (1)

Verification of total debit and credit column:

Working note 1:

Calculate the amount of cash on dated 5th January:

Working note 2:

Calculate the amount of bank credit card expense on dated 5th January:

Working note 3:

Calculate the amount of cash on dated 5th January:

Working note 4:

Calculate the amount of cash on dated 12th January:

Working note 5:

Calculate the amount of bank credit card expense on dated 12th January:

Working note 6:

Calculate the amount of cash on dated 12th January:

Working note 7:

Calculate the amount of cash on dated 19th January:

Use the general journal to record the sales returns and allowances:

General Journal: It is a book where all the monetary transactions are recorded in the form of journal entries on the date of their occurrence in a chronological order.

Transaction on January 11:

| General Journal | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| 20-- | ||||||

| January | 11 | Sales Returns and Allowances | 401.1 | 40.00 | ||

| Sales Tax Payable | 231 | 2.00 | ||||

| Accounts Receivable, MA | 122/✓ | 42.00 | ||||

| (Record merchandise returned) | ||||||

Table (2)

Description:

- ■ Sales Returns and Allowances is a contra-revenue account, and contra-revenue accounts decrease the equity value, and a decrease in equity is debited.

- ■ Sales Tax Payable is a liability account. Since the payable decreased due to returns, the liability decreased, and a decrease in liability is debited.

- ■ Accounts Receivable, MA is an asset account. Since inventory is returned, amount to be received has decreased, asset account is decreased, and a decrease in asset is credited.

Working note 1:

Compute the sales tax payable amount.

Working note 2:

Compute the accounts receivable amount.

Transaction on January 18:

| General Journal | ||||||

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| 20-- | ||||||

| January | 21 | Sales Returns and Allowances | 401.1 | 31.00 | ||

| Sales Tax Payable | 231 | 1.55 | ||||

| Accounts Receivable, RZ | 122/✓ | 32.55 | ||||

| (Record merchandise returned) | ||||||

Table (3)

Description:

- ■ Sales Returns and Allowances is a contra-revenue account, and contra-revenue accounts decrease the equity value, and a decrease in equity is debited.

- ■ Sales Tax Payable is a liability account. Since the payable decreased due to returns, the liability decreased, and a decrease in liability is debited.

- ■ Accounts Receivable, RZ is an asset account. Since inventory is returned, amount to be received has decreased, asset account is decreased, and a decrease in asset is credited.

Working note 1:

Compute the sales tax payable amount.

Working note 2:

Compute the accounts receivable amount.

2.

Post the prepared journal to the general ledger, and to the accounts receivable ledger.

2.

Explanation of Solution

Posting transactions: The process of transferring the journalized transactions into the accounts of the ledger is known as posting the transactions.

Post the prepared journals to the general ledger:

| ACCOUNT Cash ACCOUNT NO. 101 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20-- | |||||||

| January | 1 | Balance | ✓ | 2,890.75 | |||

| 31 | CR10 | 15,174.85 | 18,065.60 | ||||

Table (4)

| ACCOUNT Accounts Receivable ACCOUNT NO. 122 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20-- | |||||||

| January | 1 | Balance | ✓ | 6,300.00 | |||

| 11 | J8 | 42.00 | 6,258.00 | ||||

| 21 | J8 | 32.55 | 6,225.45 | ||||

| 31 | CR10 | 3,481.00 | 2,744.45 | ||||

Table (5)

| ACCOUNT Sales Tax Payable ACCOUNT NO. 231 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20-- | |||||||

| January | 11 | J8 | 2.00 | 2.00 | |||

| 21 | J8 | 1.55 | 3.55 | ||||

| 31 | CR10 | 561.50 | 557.95 | ||||

Table (6)

| ACCOUNT Sales ACCOUNT NO. 401 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20-- | |||||||

| January | 31 | CR10 | 11,230.00 | 11,230.00 | |||

Table (7)

| ACCOUNT Sales Returns and Allowances ACCOUNT NO. 401.1 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20-- | |||||||

| January | 11 | J8 | 40.00 | 40.00 | |||

| 21 | J8 | 31.00 | 71.00 | ||||

Table (8)

| ACCOUNT Bank Credit Card Expense ACCOUNT NO. 513 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20-- | |||||||

| January | 31 | CR10 | 97.65 | 97.65 | |||

Table (9)

Post the journals to the accounts receivable ledger.

| NAME RB | ||||||

| ADDRESS 229 SE 65th Avenue, P, Or 97215-1451 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| January | 1 | Balance | ✓ | 1,400.00 | ||

| 1 | CR10 | 880.00 | 520.00 | |||

| 11 | J8 | 42.00 | 478.00 | |||

Table (10)

| NAME D Manufacturing | ||||||

| ADDRESS 447 6th Avenue, F Staff, AZ 86004-6842 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| January | 1 | Balance | ✓ | 318.00 | ||

| 25 | CR10 | 318.00 | 0 | |||

Table (11)

| NAME CH | ||||||

| Address 1462 N. S Blvd., Los Cruces, Nm 88012-7791 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | 815 | |||||

| January | 1 | Balance | ✓ | 271 | 544 | |

| 3 | CR10 | |||||

Table (12)

| NAME JS | ||||||

| ADDRESS 5997 Blackgold Lane, G, TX 76051-2366 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| January | 1 | Balance | ✓ | 1,481.00 | ||

| 20 | CR10 | 912.00 | 569.00 | |||

Table (13)

| NAME RZ | ||||||

| ADDRESS 6881 S Drive, San D, CA 92127-8671 | ||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance ($) | |

| 20-- | ||||||

| January | 1 | Balance | ✓ | 2,286.00 | ||

| 15 | CR10 | 1,100.00 | 1,186.00 | |||

| 18 | J8 | 32.55 | 1,153.45 | |||

Table (14)

Want to see more full solutions like this?

Chapter 12 Solutions

COLLEGE ACCOUNTING CH. 1-9 (LOW COST)

- For the current fiscal year, Purchases were $380,000, Purchase Returns and Allowances were $12,000, Purchase Discounts were $5,500, and Freight-In was $52,000. If the beginning merchandise inventory was $75,000 and the ending merchandise inventory was $102,000, what is the Cost of Goods Sold (COGS)? Right Answerarrow_forwardWhat is the amount of cost of goods sold?arrow_forwardPlease provide the answer to this general accounting question with proper steps.arrow_forward

- A corporation purchases land and a warehouse on the land. The land is appraised at $150,000, and the warehouse at $250,000. If the cost of the property is $380,000 in total, then the portion of the cost allocable to the land is _____.arrow_forwardPlease explain the solution to this general accounting problem with accurate principles.arrow_forwardCan you explain the correct methodology to solve this financial accounting problem?arrow_forward

- Do fast answer of this general accounting questionarrow_forwardPlease provide the accurate answer to this general accounting problem using valid techniques.arrow_forwardFor the current fiscal year, Purchases were $380,000, Purchase Returns and Allowances were $12,000, Purchase Discounts were $5,500, and Freight-In was $52,000. If the beginning merchandise inventory was $75,000 and the ending merchandise inventory was $102,000, what is the Cost of Goods Sold (COGS)? Helparrow_forward

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub