Concept explainers

Videos

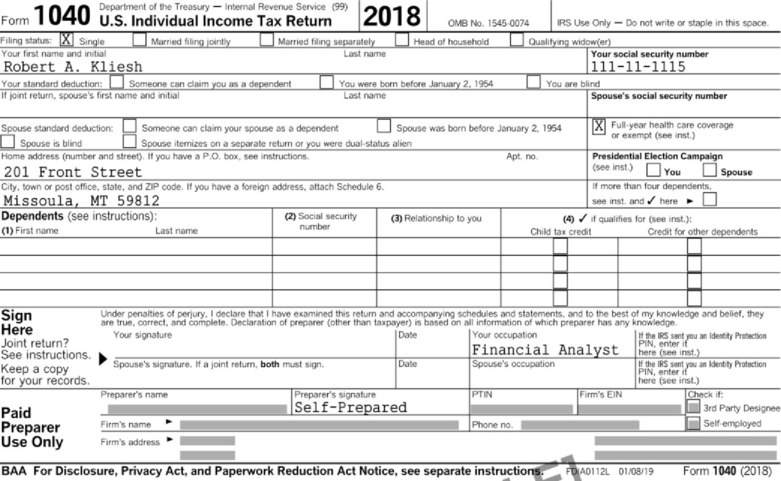

Robert A. Kliesh, age 41, is single and has no dependents. Robert’s Social Security number is 111-11-1115. His address is 201 Front Street, Missoula, MT 59812. He does not contribute to the Presidential Election Campaign fund through the Form 1040.

Robert works as a financial analyst and is very well regarded in his field. This year his salary totaled $650,000. His professional success has allowed him to purchase investments in real estate and corporate stocks and bonds. He also spends time volunteering with various organizations that help people develop financial literacy skills. Examination of Robert’s financial records provides the following information for 2018.

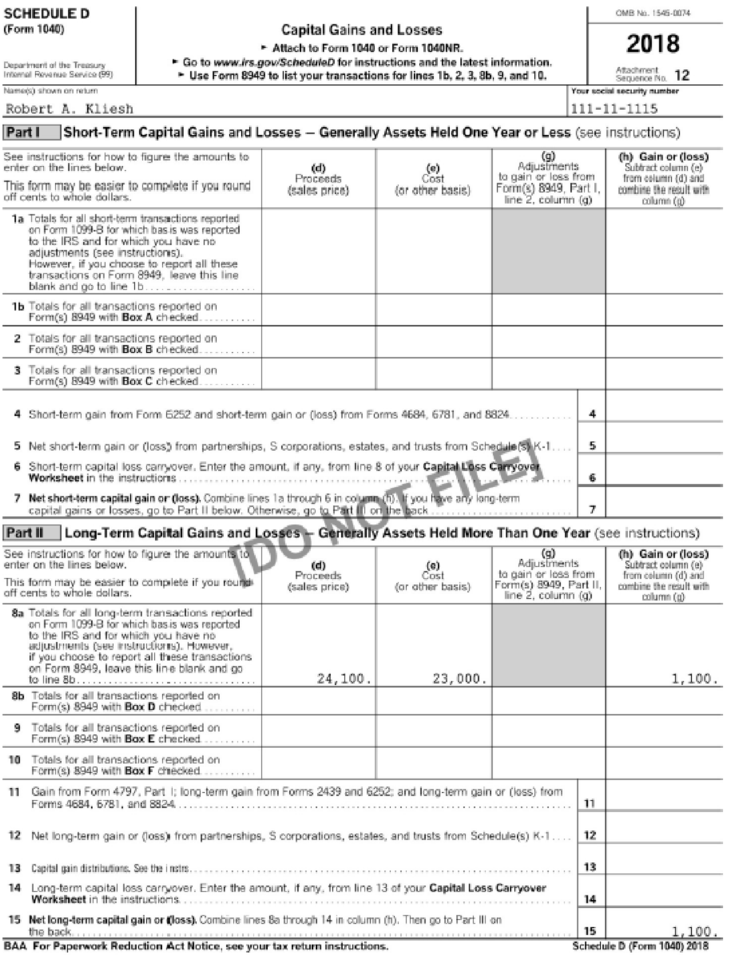

- a. On January 16, Robert sold 1,000 shares of stock for a loss of $12,000. The stock was acquired 14 months ago for $17,000 and sold for $5,000. On February 15, he sold 400 shares of stock for a gain of $13,100. That stock was acquired in 2010 for $6,000 and sold for $19,100.

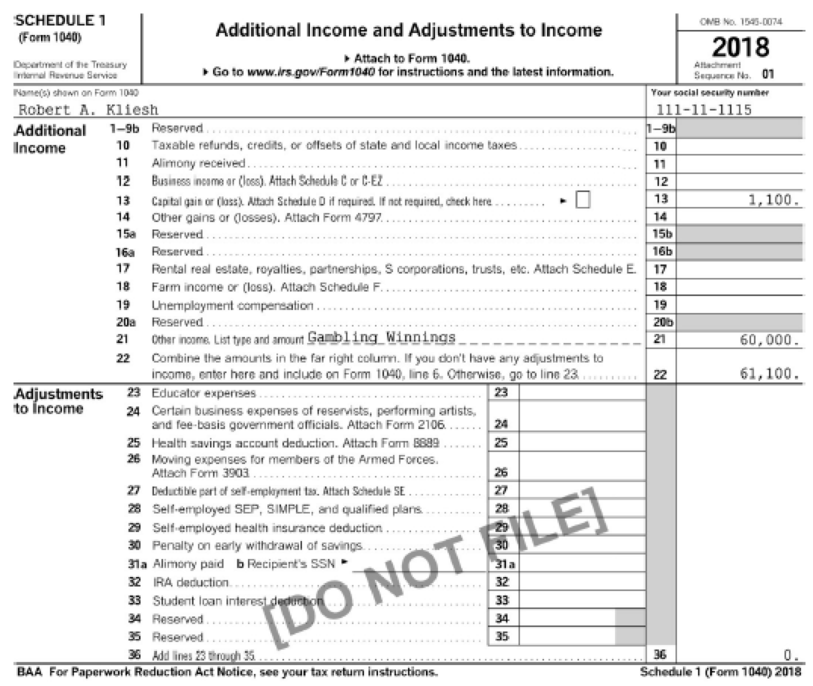

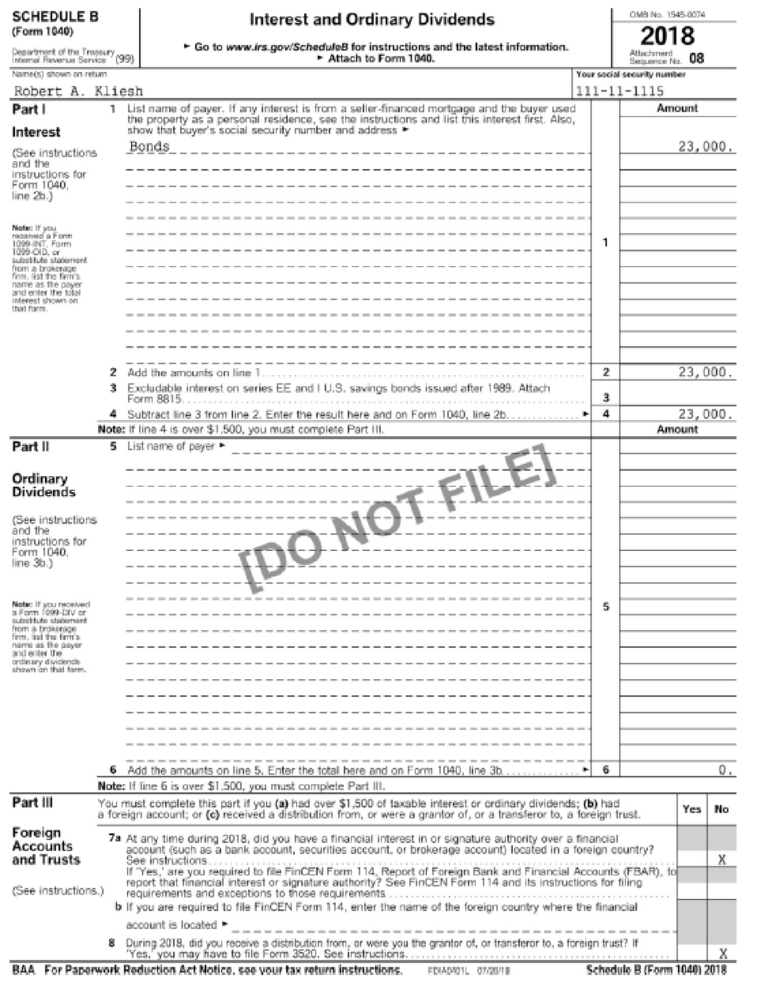

- b. He received $30,000 of interest on private activity bonds that he purchased in 2015. He also received $40,000 of interest on tax-exempt bonds that are not private activity bonds.

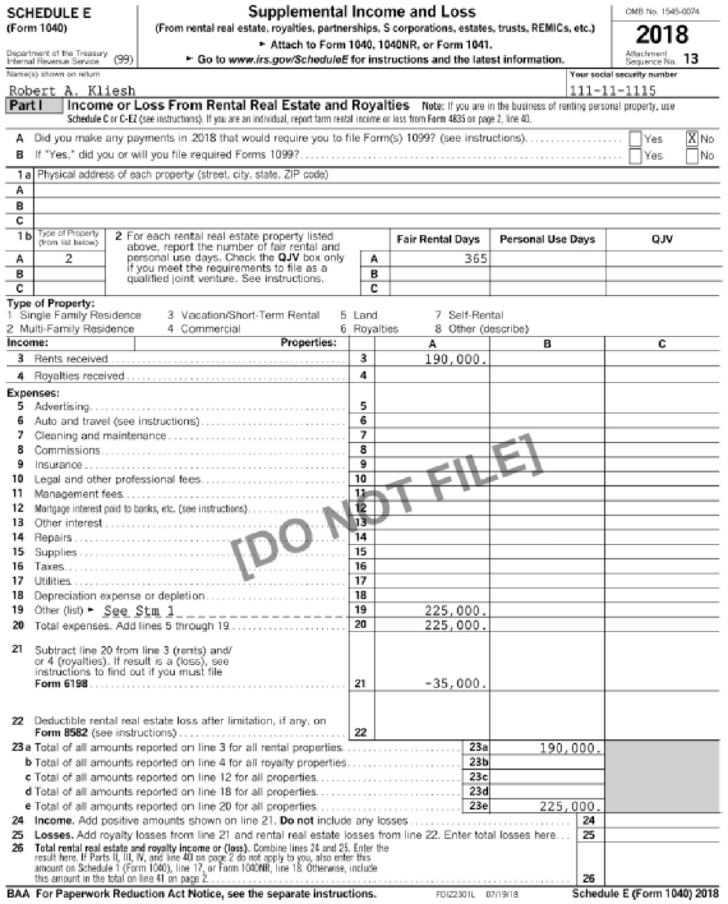

- c. Robert received gross rent income of $190,000 from an apartment complex he owns. He qualifies as an active participant in the activity. The property is at 50 Big Sky Resort Road, Big Sky, Montana, 59716.

- d. Expenses related to the apartment complex, acquired in 2009, were $225,000.

- e. Robert’s taxable interest income, all from corporate bonds, totaled $23,000. Because he invests only in growth stocks, he receives no dividend income.

- f. He won $60,000 in the Montana lottery.

- g. Robert was the beneficiary of an $800,000 life insurance policy on the life of his uncle Jake. He received the proceeds in October.

- h. In February, Robert exercised an incentive stock option that was granted by his employer in 2015. The strike price of the option was $10 per share. On the date of exercise, the fair market value of the stock was $25 per share. Robert purchased 400 shares with the option; as of the end of the year, he still owns the stock (current FMV $20 per share).

- i. Robert incurred the following potential itemized deductions.

- • $5,200 fair market value of stock contributed to the Red Cross ($3,000 stock basis). He had owned the stock for two years. Robert also made cash contributions of $8,000 to qualified organizations during the year.

- • $4,200 interest on consumer purchases.

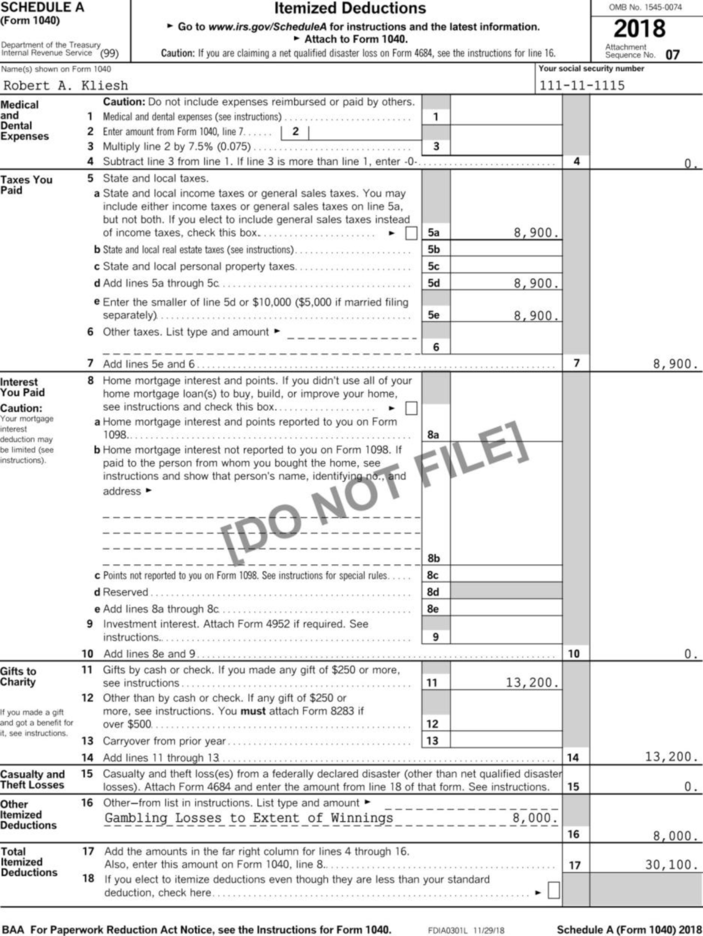

- • $8,900 state and local income tax.

- • $15,000 of medical expenses that he paid on behalf of his administrative assistant, who unexpectedly took ill.

- • $8,000 paid for lottery tickets associated with playing the state lottery.

- • $750 contribution to the campaign of the Democratic candidate for governor of Montana.

- • Because Robert lived in Montana, he paid no state-income tax.

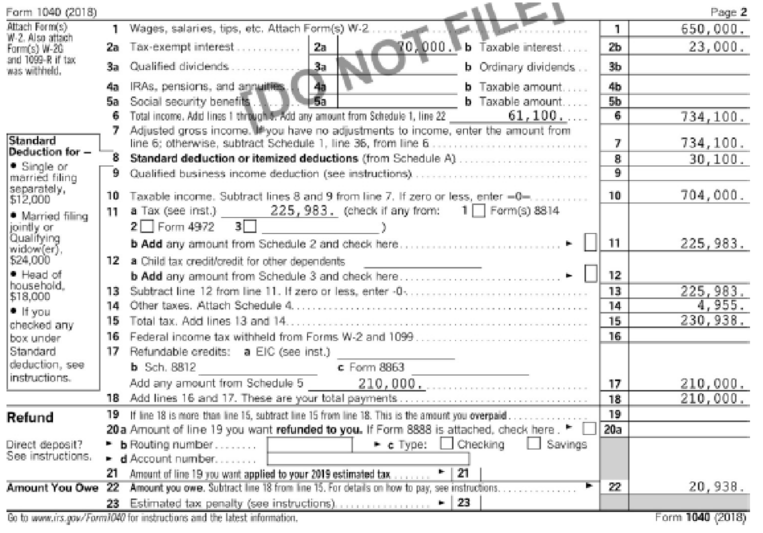

Robert made estimated Federal tax payments of $210,000, and he was covered by health insurance for the entire tax year.

Use Forms 1040 and 6251 and Schedules A, B, D, and E to compute the tax liability (including AMT) for Robert A. Kliesh for 2018. Omit Forms 8283, 8582, and 8949. Suggested software: ProConnect Tax Online.

Determine R’s taxable income and regular tax liability and Alternative Minimum Taxable Income (AMTI). Also, find whether he has an AMT liability.

Explanation of Solution

Determine R’s taxable income and regular tax liability.

| Calculation of taxable income and regular tax liability | ||

| Description | Amount | |

| Salary | $650,000 | |

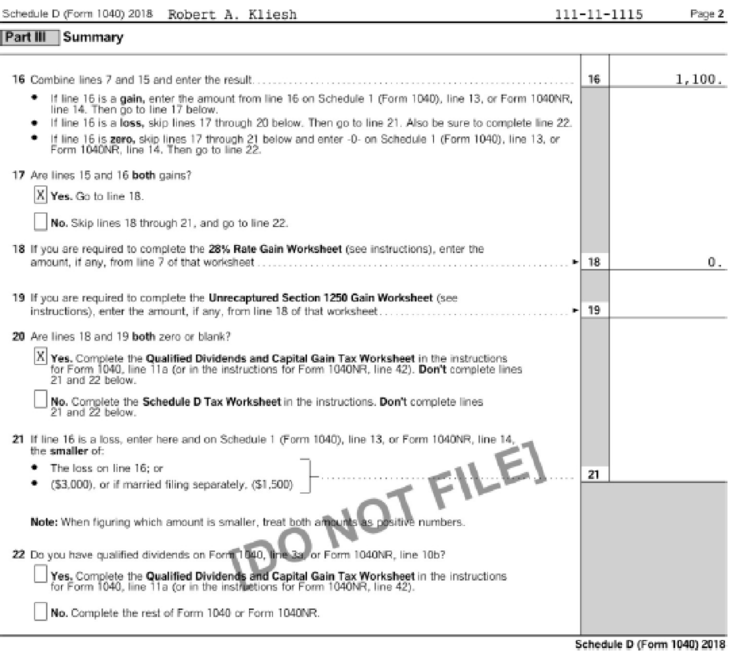

| Long-term capital gain | $1,100 | Refer working note 1 |

| Interest income | $23,000 | Refer working note 2 |

| Lottery winnings | $60,000 | |

| Life insurance proceeds | $0 | Refer working note 3 |

| Adjusted Gross income before rental loss | $734,100 | |

| Real estate rental loss | $0 | Refer working note 4 |

| Adjusted Gross income | $734,100 | |

| Less: Itemized deductions: | $(30,100) | Refer working note 5 |

| Taxable income | $704,000 | |

| Regular income tax liability | $225,983 | Refer working note 6 |

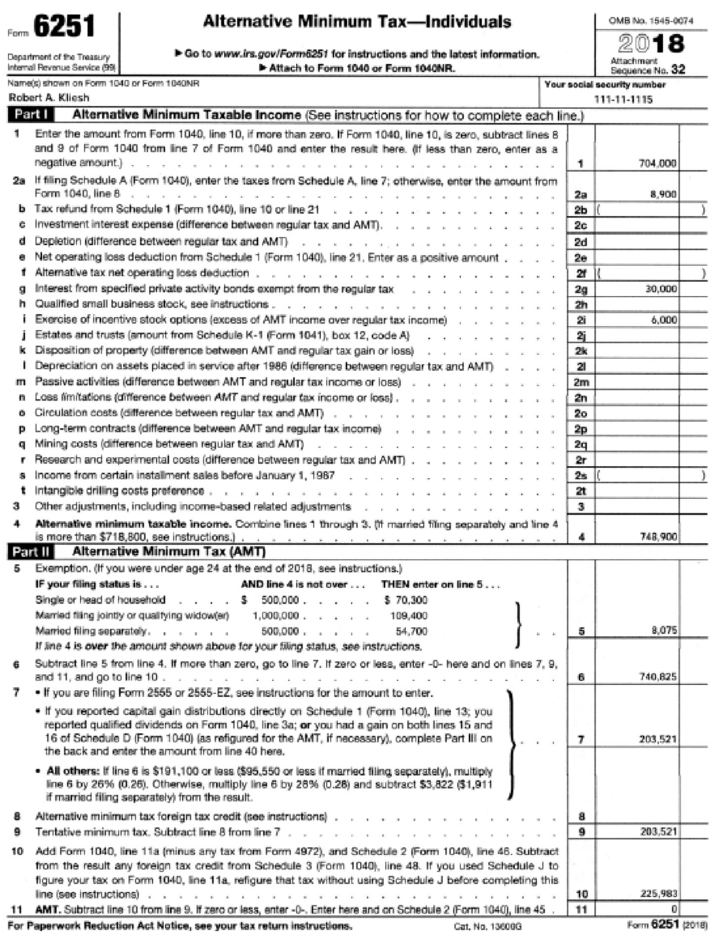

Compute R’s AMT (alternative minimum tax).

| Calculation of AMT | ||

| Particulars | Amount | |

| Taxable income | $704,000 | |

| Add: Adjustments and preferences | ||

| Incentive stock option adjustment | $6,000 | Refer working note 7 |

| State and local income taxes | $8,900 | |

| Interest on private activity bonds | $30,000 | |

| Alternative minimum taxable income (AMTI) | $748,900 | |

| Less: Exemption | $(8,075) | Refer working note 8 |

| AMT base | $740,825 | |

| TMT | $203,521 | Refer working note 9 |

| Less: Regular Income tax liability | $225,983 | Refer working note 6 |

| AMT | $0 | |

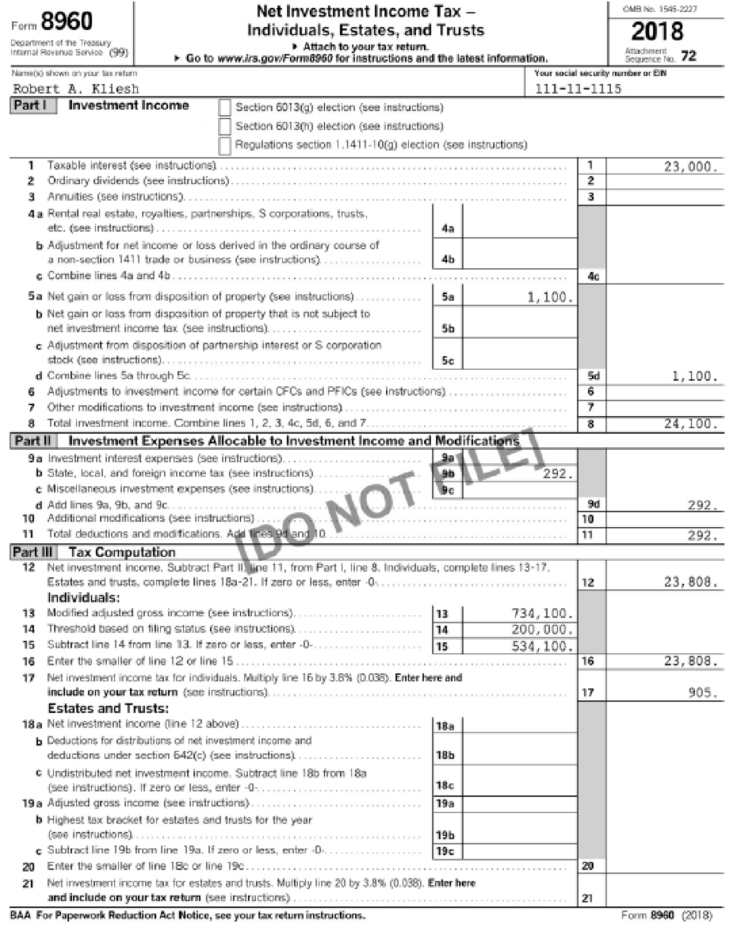

Calculate R’s tax owned or (refund due).

| Calculation of total tax liability | |

| Particulars | Amount |

| Regular income tax liability | $225,983 |

| Alternative minimum tax | $0 |

| Medical and investment taxes | $4,955 |

| Total tax liability | $230,938 |

| Less: Estimated tax payments | (210,000) |

| Tax owned | $20,938 |

Working Note (1):

Long-term capital gain of $13,100 is offset by long-term capital loss of $12,000. Hence, net long-term capital gain is $1,100

Working Note (2):

$30,000 of interest on private activity bonds and $40,000 of other tax-exempt interest is excluded from gross income. $23,000 of interest income on growth stock is included in gross income.

Working Note (3):

The life insurance proceeds of $800,000 are excluded from gross income.

Working Note (4):

Calculate the amount of loss on rental property.

R is an active participant. Hence, he may deduct a loss of $35,000

Working Note (5):

Calculate itemized deductions.

| Calculation of itemized deduction | |

| State and local income taxes | $8,900 |

| Gambling losses | $8,000 |

| Charitable contributions | $13,200 |

| Itemized deductions | $30,100 |

Note: Consumer interest of $4,200 is not deductible. As the assistant is not the dependent of R, Medical expense of $15,000 is not deductible.

Working Note (6):

Calculate regular income tax liability.

Working Note (7):

Calculate the amount of incentive stock option adjustment.

Working Note (8):

Determine the AMT exemption (files as single taxpayer).

Working Note (9):

Calculate the amount of tentative minimum tax.

Complete the appropriate form for R.

Want to see more full solutions like this?

Chapter 12 Solutions

Individual Income Taxes

- Varma Corporation distributes property to its sole shareholder, Maya. The property has a fair market value of $675,000 and an adjusted basis of $425,000. With respect to the distribution, Varma has a gain of ____.arrow_forwardCan you explain this general accounting question using accurate calculation methods?arrow_forwardAccounting questionarrow_forward

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT