(a)

To Discuss:

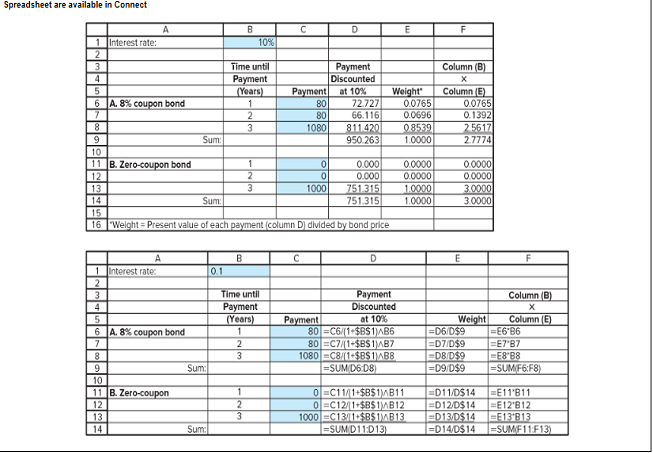

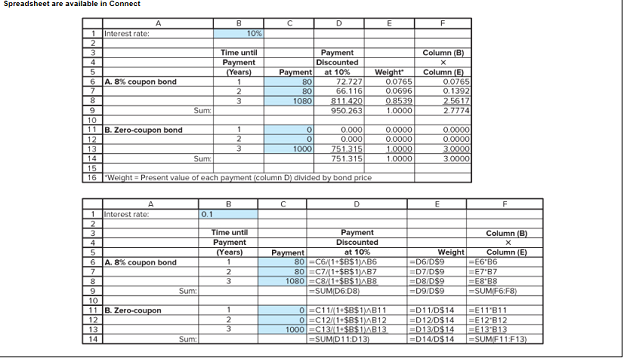

To use a spreadsheet to calculate the duration of the two bonds in Spreadsheet 11.1 if the market interest rate increases to 12%.The explanation of the reason of the fall in the duration of the coupon bond while the duration of the zero-coupon bond remaining unchanged is to be given.

Spreadsheet 11.1

Introduction:

A bond is a security that creates an obligation on the issuer to make specified payments to the holder for a given period of time. The face value of the bond is the amount the holder will receive on maturity along with the coupon rate which is also known as the interest rate of the bond.A zero-coupon bond is a bond where the face value is repaid at the time of maturity.

Yield to maturity means the discount rate which makes the present payments from the bond equal to the price, in simple terms it is the average

(b)

To Discuss:

To use the same spreadsheet to calculate the duration of the coupon bond if the coupon were 12% instead of 8%.The explanation of the reason of the duration of the coupon bond being lower is to be given.

Spreadsheet 11.1

Introduction:

A bond is a security that creates an obligation on the issuer to make specified payments to the holder for a given period of time. The face value of the bond is the amount the holder will receive on maturity along with the coupon rate which is also known as the interest rate of the bond. A zero-coupon bond is a bond where the face value is repaid at the time of maturity.

Yield to maturity means the discount rate which makes the present payments from the bond equal to the price, in simple terms it is the average rate of return a holder can expect from that bond. Duration is a measure of the sensitivity of the price -- the value of principal -- of a bond to a change in interest rates. The duration of a zero-coupon bond is equal to the time to maturity of the bond.

Want to see the full answer?

Check out a sample textbook solution

Chapter 11 Solutions

Essentials Of Investments

- Delta Corporation has the following capital structure: Cost Weighted (after-tax) Weights Cost Debt 8.1% 35% 2.84% Preferred stock (Kp) 9.6 5 .48 Common equity (Ke) (retained earnings) 10.1 60 6.06 Weighted average cost of capital (Ka) 9.38% a. If the firm has $18 million in retained earnings, at what size capital structure will the firm run out of retained earnings? b. The 8.1 percent cost of…arrow_forwardDillon Enterprises has the following capDillon Enterprises has the following capital structure. Debt ........................ 40% Common equity ....... 60 The after-tax cost of debt is 6 percent, and the cost of common equity (in the form of retained earnings) is 13 percent. What is the firm’s weighted average cost of capital? a. An outside consultant has suggested that because debt is cheaper than equity, the firm should switch to a capital structure that is 50 percent debt and 50 percent equity. Under this new and more debt-oriented arrangement, the after-tax cost of debt is 7 percent, and the cost of common equity (in the form of retained earnings) is 15 percent. Recalculate the firm’s weighted average cost of capital. b. Which plan is optimal in terms of minimizing the weighted average cost of capital?arrow_forwardCompute Ke and Kn under the following circumstances: a. D1= $5, P0=$70, g=8%, F=$7 b. D1=$0.22, P0=$28, g=7%, F=2.50 c. E1 (earnings at the end of period one) = $7, payout ratio equals 40 percent, P0= $30, g=6%, F=$2,20. Note: D1 is the earnings times the payout rate. d. D0 (dividend at the beginning of the first period) = $6, growth rate for dividends and earnings (g)=7%, P0=$60, F=$3. You will need to calculate D1 (the dividend after the first period).arrow_forward

- Terrier Company is in a 45 percent tax bracket and has a bond outstanding that yields 11 percent to maturity. a. What is Terrier's after-tax cost of debt? b. Assume that the yield on the bond goes down by 1 percentage point, and due to tax reform, the corporate tax falls to 30 percent. What is Terrier's new aftertax cost of debt? c. Has the after-tax cost of debt gone up or down from part a to part b? Explain why.arrow_forwardThe Squeaks Cat Rescue, which is tax-exempt, issued debt last year at 9 percent to help finance a new animal shelter in Rocklin. a. If the rescue borrowed money this year, what would the after-tax cost of debt be, based on its cost last year and the 25 percent increase? b. If the receipts of the rescue were found to be taxable by the IRS (at a rate of 25 percent because of involvement in political activities), what would the after-tax cost of debt be?arrow_forwardNo chatgptPlease don't answer i will give unhelpful all expert giving wrong answer he is giving answer with using incorrect values.arrow_forward

- Please don't answer i will give unhelpful all expert giving wrong answer he is giving answer with incorrect data.arrow_forward4. On August 20, Mr. and Mrs. Cleaver decided to buy a property from Mr. and Mrs. Ward for $105,000. On August 30, Mr. and Mrs. Cleaver obtained a loan commitment from OKAY National Bank for an $84,000 conventional loan at 5 percent for 30 years. The lender informs Mr. and Mrs. Cleaver that a $2,100 loan origination fee will be required to obtain the loan. The loan closing is to take place September 22. In addition, escrow accounts will be required for all prorated property taxes and hazard insurance; however, no mortgage insurance is necessary. The buyer will also pay a full year's premium for hazard insurance to Rock of Gibraltar Insurance Company. A breakdown of expected settlement costs, provided by OKAY National Bank when Mr. and Mrs. Cleaver inspect the uniform settlement statement as required under RESPA on September 21, is as follows: I. Transactions between buyer-borrower and third parties: a. Recording fees--mortgage b. Real estate transfer tax c. Recording fees/document…arrow_forwardHello tutor give correct answerarrow_forward

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education