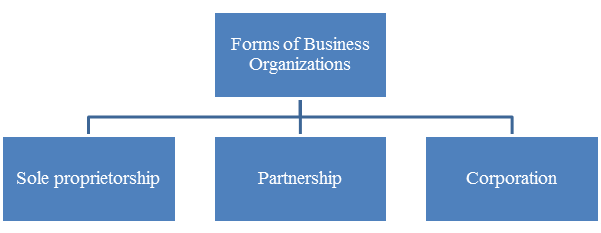

Describe the three major forms of business organizations.

Explanation of Solution

Forms of business organizations:

Sole proprietorship: It is one form of simple business that is owned and maintained by a single person. Obtaining business licence from the local government is required to setup the sole proprietorship. Government provides tax advantages for these firms.

Corporation: Corporation is a form of business organization which is created and organized as per the laws of the state. There is a separate legal entity in this form of business organization that means, it is owned by shareholders and managed by a board of directors. The transfer of ownership and raising funds are easy in this form of organization. No personal legal liability exists among the shareholders.

Want to see more full solutions like this?

Chapter 11 Solutions

Fundamental Financial Accounting Concepts, 9th Edition

- Delta's inventory records for February reflect the following details: On February 1, the beginning inventory consisted of 250 units priced at $3.20 each. On February 9, Delta made its first purchase of 350 units at a cost of $3.50 each. A second purchase was made on February 18, consisting of 500 units priced at $3.70 each. By the end of the month, on February 28, Delta sold 700 units at a price of $6.50 per unit. Using the FIFO (First-In, First-Out) cost flow method, what is the cost of goods sold (COGS) for February?arrow_forwardPlease explain the solution to this general accounting problem with accurate principles.arrow_forwardPlease explain how to solve this financial accounting question with valid financial principles.arrow_forward

- Veloid Ltd. has Assets of $312,480 and Liabilities of $95,165. The firm has 11,920 shares of stock outstanding. Then the board decides to pay a dividend of $10.50 per share. What is the value of Stockholders' Equity after the payment of the dividend?arrow_forwardShri Manufacturing has estimated total factory overhead costs of $625,000 and 25,000 direct labor hours for the current fiscal year. If direct labor hours for the year total 23,500 and actual factory overhead totals $610,000, what is the amount of overapplied or underapplied overhead for the year? Helparrow_forwardWhat is the correct answer with accounting questionarrow_forward

- Please solve this general accounting problem an given step by step explanationarrow_forwardBeacon Manufacturing has $85,000 in assets. They also have $32,000 in liabilities and $8,500 in expenses, and they paid out $6,200 in dividends this year. The extended accounting equation is assets = liabilities + (revenue - (expenses + dividends)). What would their revenue need to be for their accounts to be in balance?arrow_forwardThe Patidar Group manufactures and sells a single product, Product T. Budgeted sales for June are $450,000. Gross Margin is budgeted at 35% of sales dollars. If the net income for June is budgeted at $62,500, the budgeted selling and administrative expenses are?arrow_forward

- Can you explain the correct methodology to solve this financial accounting problem?arrow_forwardCan you help me solve this general accounting question using the correct accounting procedures?arrow_forwardI need help with this general accounting question using standard accounting techniques.arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education